Account Aggregator leverages ‘informed’ consent to enable multiple use cases in digital lending

Chitwan Kaur

Content Specialist

|

Jul 12, 2023

User data is the lifeblood for lenders. Be it physical operations or digital lending - the volume and velocity of data sought, collected and analysed is only increasing exponentially. This added exposure not only makes it tougher to cull insights but also increases data privacy risks.

There are solutions to this data privacy risk that function at legislative, institutional, and even specific company levels. However, one innovation that cuts across all these tiers and levels the playing field is the Account Aggregator framework.

As discussed earlier, AA is a modern data-sharing framework that puts user consent front and center of the workflows and enables encrypted flow of data between financial information providers to financial information users.

The core innovation in AA, however, is the introduction of informed consent - a detailed, privacy-first and user-controlled framework for deciding what, how much and for how long is there data shared with a specific entity. How does this work? Let’s dive into the details.

Informed consent

What is user consent? The permission given by a user to a platform, website or application to proceed with the collection of their data.

Platforms often register users’ consent (or denial) to the collection of this data through a verbose privacy policy screen. However, as a Deloitte report showed, 91% of users willingly sign away their consent without reading the terms and conditions !

Can financial service providers create a user experience that simplifies the process of informing customers about the use of the information sought before securing their consent? It’s challenging to build such a component within the user journey because it requires complicated explanations, protection of confidentiality, and compliance with regulatory requirements and protocol.

The Account Aggregator framework was created after due consideration to the ‘uninformed’ nature of such consent.

Fetching consent under Account Aggregator, in contrast to conventional methods, is based on ‘informed’ consent. Customers explicitly grant their consent with complete knowledge of the data being sought and its use. In addition to this, it makes the process transparent by declaring –

The names of the Financial Information Users (FIUs) and Financial Information Providers (FIPs)

The purpose of seeking this data like lending, wealth management, or personal finance management

The time period over which the data will be used by the FIU

The frequency at which the data will be pulled (one-time or recurring)

Which data fields from a financial document will be shared

The duration of user consent validity

The digital signature from the particular Account Aggregator requesting the information

By securing explicit, informed consent, platforms can unlock a range of use cases addressing the needs of end users.

Periodic consent

The informed nature of consent – and the seamlessness of its integration within the journey – makes it possible for FIUs to tap into a user’s financial information recurrently, with due consent. This capability also fuels several use cases in financial services, especially digital lending.

Loan monitoring

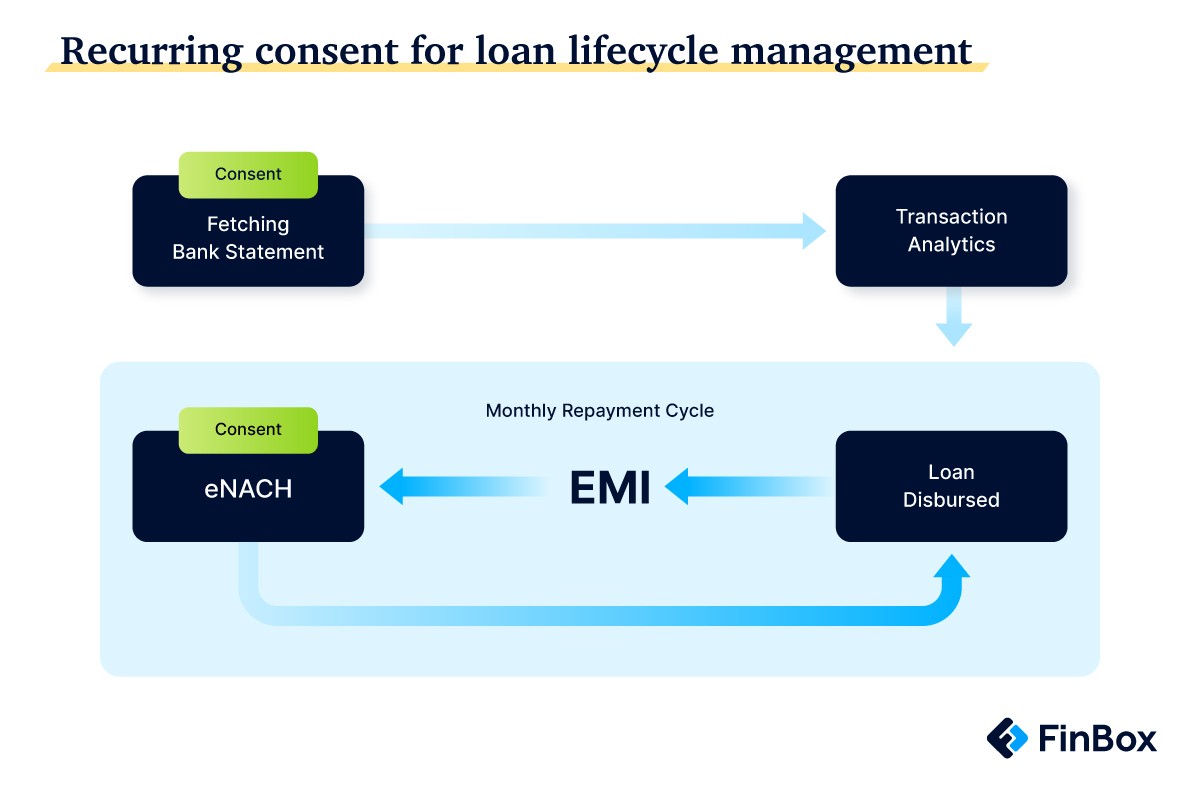

Instinctively, most digital lenders are using the Account Aggregator framework to pull bank statements for underwriting. However, periodic consent allows lenders (FIUs) to request the FIPs for financial information at various points during the loan lifecycle.

The Account Aggregator framework enables lenders to set the frequency at which consented extractions of data occur. These can be scheduled for multiple times a day, daily, weekly or monthly. FinBox BankConnect allows lenders to automate the eNACH trigger if the funds in the account are sufficient for the amount payable.

This can help nip delinquencies in the bud by identifying them early through repetitive access to borrowers’ bank statements. Armed with this information, lenders can gauge when a user has the means to pay their installments, and schedule the eNACH requests accordingly. This solves the “ability” question when it comes to loan repayment, improving chances of debt recovery since the user has the liquidity to pay their EMIs.

Accounting

Accounting platforms need recurring access to the financial information of businesses to conduct analysis. Repeatedly asking for such information places a greater cognitive burden on the user, ultimately making for a poor user experience.

Through Account Aggregator’s recurring pull feature, such platforms can secure user consent once and continue to tap into the current accounts of business users over a predetermined period of time.

Personal finance management

The Account Aggregator framework allows personal finance management platforms to tap into multiple financial accounts like bank accounts, insurance, investments, etc. This enables them to seamlessly source financial information from a variety of essential sources, thus giving users insights to better manage their personal finance.

Conclusion

The Account Aggregator framework is a unique example of ecosystems that balance data security, user experience, and business viability for platforms by unlocking the capacity to scale. At FinBox, our efforts to leverage the framework for MSME lending were laureled at SamvAAd 2023 – just a small step in our journey to innovate on top of the underlying ecosystem that is being touted as the UPI moment for digital lending!

Get in touch for a demo .

bank statement analyser, FinBox BankConnect, Account Aggregator, underwriting