Flaws in risk assessment and how they foster lending biases

Anna Catherine

Content Specialist

|

Dec 16, 2021

With Omicron looming over, RBI in its efforts to stimulate the economy has left the repo rate unchanged at 4%. This accommodative stance is flushing banks with liquidity. Yet, loans to companies and individuals have been growing only at a subdued 5.5-6%. Why? Memories of insurmountable NPAs have kept India’s banking sector risk-averse. And bankers don’t even want to try swinging it anymore even if that means failing to achieve targets — once bitten, twice shy. Unfortunately, this is stripping the economy of credit support when it’s needed the most.

But how long can banks sit on too much cash? Given that RBI is unenthusiastic about soaking up the excess liquidity, it’s only a matter of time until banks resort to indiscriminate lending.

How do you jolt these risk-averse lenders out of inertia? Above all, how do you prevent them from resorting to lending excesses?

The answer is risk assessment! Current risk assessment models are rife with fallacies. They impair lenders’ judgement when it comes to distinguishing good and bad borrowers.

Contextualised assessment methodologies made easy by technology can potentially save the day by helping lenders assess risk better and enable credit where it’s due. But before delving into solutions, it's important to understand the lacunae in current risk assessment methodologies and how they manifest as unconscious biases.

What is credit risk?

Simply put, credit risk measures the likelihood of borrowers failing to meet their loan obligations by assessing their ability and willingness to make good on a debt.

It has historically been measured through a formal bureau credit score, a number between 300 and 900, provided by four agencies in India — TransUnion CIBIL, Experian, Equifax, and CRIF HighMark.

However, the formal bureau coverage stands at a low of 63.1% as of 2019 and keeps 50.7 million MSMEs out of the formal credit system because of the banks’ insistence on bureau scores while making lending decisions.

Types of credit risks

1. Default Risk

Default risk refers to the possibility that a borrower will not be able to repay their loan in full or on time. It’s considered the most common type of credit risk, and can result from economic conditions, industry trends, or individual borrower behaviour.

2. Credit Spread Risk

This involves the possibility of the difference in yield between two types of debt securities will increase, which results in a loss for investors. Credit spread risk is often associated with fixed-income securities and can be caused by changes in interest rates or other market conditions.

3. Country Risk

The possibility of a borrower not being able to repay their loan due to economic, political, or social conditions in their home country is covered under this category. Country risk mostly connects with international lending and can be difficult to assess due to the complexity of international markets.

4. Concentration Risk

Concentration risk involves the probability of a lender having too much exposure to a particular industry, sector, or borrower. This type of credit risk can result from poor diversification or overreliance on a single borrower, and it can increase the likelihood of default if the borrower experiences financial difficulties.

5. Interest Rate Risk

Interest rate risk is the possibility that changes in interest rates will affect the value of a borrower's assets and liabilities, making it more difficult for them to repay their loans. In most cases, variable-rate loans fall under this umbrella, as they can be difficult to manage due to the unpredictability of interest rate fluctuations.

How to calculate credit risk?

Finding the Expected Loss (EL) is the most popular and simplest way to quantify credit risk.

In order to calculate Expected Loss, you need to consider three variables:

the probability of default (PD),

the loss given default (LGD), and

the exposure at default (EAD).

The expected loss (EL) is then calculated as the product of these three variables: EL = PD x LGD x EAD.

Consider this example:

Let's say that a bank is considering lending Rs. 1,00,000 to a borrower with a PD of 5%, an LGD of 50%, and an EAD of Rs. 75,000. Using the expected loss method, we can calculate the credit risk as follows:

EL = PD x LGD x EAD

EL = 0.05 x 0.5 x Rs. 75,000

EL = Rs. 1,875

This means that the bank can expect to lose Rs. 1,875 on average if they lend Rs. 1,00,000 to this borrower . This expected loss calculation can help the bank determine whether the potential return on the loan justifies the credit risk involved.

It's important to note that the expected loss method is just one way to calculate credit risk, and it has its limitations. For example, it assumes that the PD, LGD, and EAD are independent of each other, which may not always be the case. Additionally, it does not account for potential correlations between borrowers or external factors that could impact credit risk. As such, banks and other lenders may use additional methods and models to assess credit risk and make informed lending decisions.

Do credit risk assessments hide more than they reveal?

The centrality of formal scores and their insistence by the banks is how a lot of new and potentially good borrowers never make it to a bank’s loan book. Most lenders employ a standardised rather than a contextualised approach to credit risk assessments.

Firstly, banks in India follow a two-track approach by analysing credit risk and market risk (macroeconomic factors) separately. While credit risk is addressed in Loan Policies and Procedures, market risk is articulated in Asset-Liability Management policies. Such a distinct treatment hinders comprehensive assessment of risk.

For example, a mango exporting business with strong balance sheets, solid earnings, and positive cash flows will qualify as a promising borrower when viewed from the standpoint of credit risk. But mango exports could take a massive hit due to a variety of market factors that are beyond the control of the company. This could deplete the business’ reserves, debilitating its repayment capacity. Hence, an integrated approach becomes crucial to risk assessment.

Secondly, legacy lending institutions rely heavily on credit scores which are arrived at by credit bureaus using proprietary algorithms. There is a colossal problem of data latency that plagues credit scoring in India. In addition, they reflect input bias owing to source data being ‘noisy’ — they tend to reflect historical biases and are often unrepresentative.

For instance, women have to face greater credit-constraints than men although the repayment history of women borrowers is far more satisfactory. Similarly, new-to-credit consumers have a hard time building up credit history, while those who are trying to make amends find it an uphill battle.

In attempts to fix this, credit bureaus are digitalising rapidly to generate real-time, data-led scoring. Although this could improve accuracy in assessing risk of borrowers already part of the financial system, it would still limit access to capital for those without credit history, i.e., 190 million Indians.

Thirdly, the inability to distinguish between good and bad borrowers further exacerbates lending biases. Lenders think an averaged-out loan interest rate, a safe bet in the absence of accurate risk models. The result? High-quality borrowers will end up paying a higher interest rate than they should because low-quality borrowers pay a lower interest rate than they should.

The sum and substance — lenders often end up giving the wrong people loans and a major chunk of the population never gets the chance to build up the data needed to secure a loan in the future.

How does FinTech fill in the blanks?

In attempts to turn over a new leaf, lenders are increasingly leveraging contextualised assessments offered by alternate data . This model offers real-time visibility into a borrower’s financial health and spending behavior. How? New-age digital lenders work with customer profiles culled from alternative data sources such as contact lists, text messages, web-browsing history, and smartphone apps — painting a full picture of borrowers’ financial behavior. Also, these AI- and ML-supported predictive risk assessment models help factor in multiple parameters and discount biases.

FinBox DeviceConnect, an in-device risk engine enhances such contextualised risk assessments. It has made it easy for lenders to strike the perfect balance between assessing both ability and propensity of potential borrowers to repay loans.

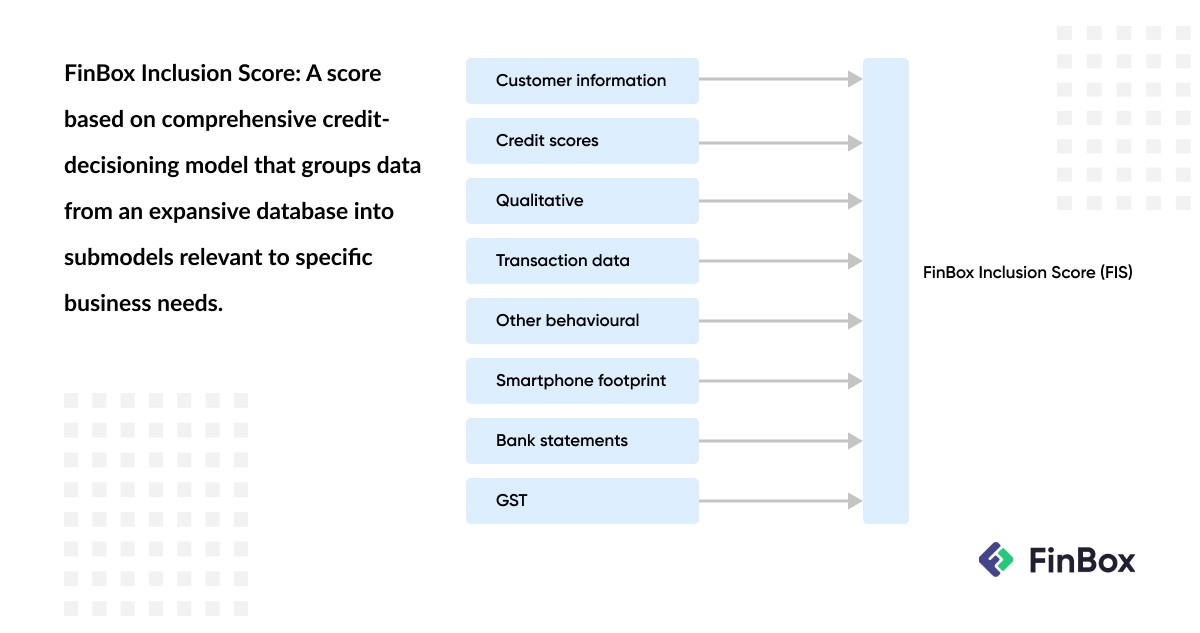

Our AI- and ML-driven underwriting suite leverages alternative data to generate a FinBox Inclusion Score (FIS), tested on the largest new-to-credit (NTC) customer base in India.

Various types of data are fed into submodels; business decisions and industry-specific parameters determine how this data are grouped and evaluated to arrive at targeted analyses.

We subject loan applications to qualitative analysis as much as quantitative analyses, including external factors on which the borrower doesn’t have control such as markets, industry trends, business environment, and more. Extensive analysis of GST data reveals qualitative inputs pertaining to the borrower's core business, historic development of the company, credibility, and more.

This holistic approach has helped lenders improve approval rates by 25%. Also, its ability to raise red flags using insights from real-time data has helped reduce delinquency by 30%. To top it all, FinBox DeviceConnect covers 92% of digitally acquired customers as opposed to credit bureau coverage of 63.1%.

This makes possible risk-based lending — a tiered pricing structure that assigns loan rates based on an individual's credit risk. Such smart, accurate risk assessment models may just be the panacea to the default menace plaguing the Indian banking and financial sector.

["risk assessment"]["digital lending"]["credit risk management"]["alternative data"]["Banking as a Service"]["FinTech"]["New-to-Credit"]["Inclusion Score"]["Alternate Data"]["DeviceConnect"]["MSME"]