How do credit cards really work? Unpacking the magic stack that makes tap and pay happen

Aparna Chandrashekar

Content Specialist

|

Jul 11, 2022

Credit cards have the potential to be one of the most powerful financial tools available to consumers. And for banks, it can be one of the most lucrative business opportunities.

With the RBI now allowing for credit cards to be linked to UPI, there’s delirium around not just UPI becoming the most mighty payment system in the world, but also deeper penetration of credit cards.

To think about it, credit cards are magical - they’re arguably easier to use than UPI - with the NFC tap-to-pay functionality, and are still the preferred option for millions - consumers needn’t worry about having a 3G/4G network, and it takes 2-3 seconds as opposed to other payment methods including UPI, which can take up to a minute.

For banks, credit cards are tools for revenue generation, getting insights into consumer behaviour, increasing loyalty and building a brand that people will remember.

Building a credit card is easier said than done, it’s complicated, to say the least. There are many logistics to consider and a number of moving pieces that need to be aligned to make it work.

In fact, an average credit card transaction involves at least half a dozen players.

Who’re the players involved and how does each player make money?

We’re breaking it down for you in this blog -

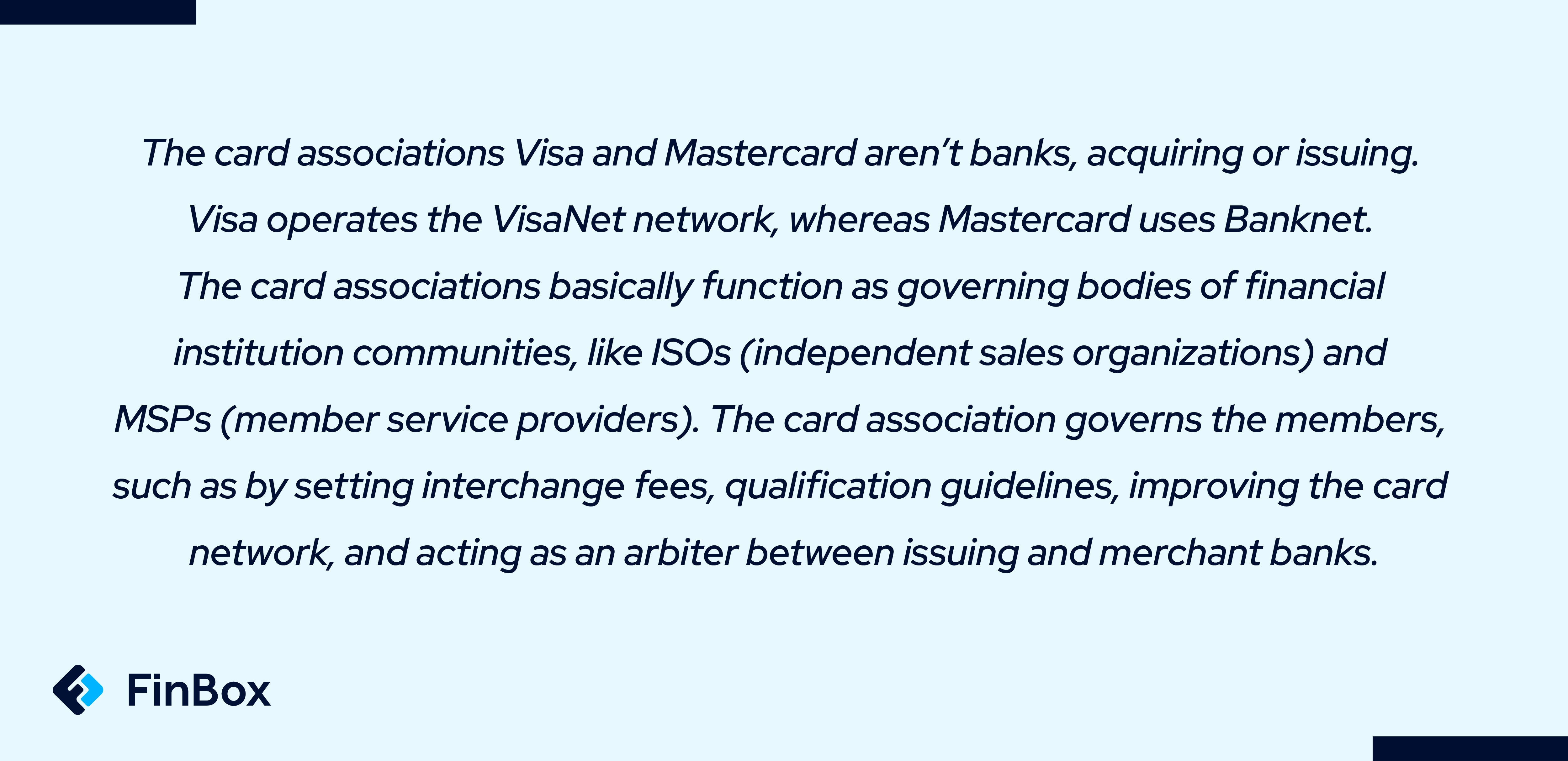

A bank card network conducts billions of transactions between customers, merchants, processors and banks in mere seconds. The merchant’s terminal software (payment gateway) passes the transaction information to the processor, and the processor asks for authorisation from the issuing bank. Sitting at the centre of the payments industry are card networks like Visa, MasterCard, American Express and Discover. Think of them as the toll booths of the industry - they supply the electronic network that allows all the players in the ecosystem to communicate with one another. For this, they charge a fee.

How do Credit Cards work?

Credit cards allow individuals to borrow money for various purchases. Here's a brief overview of how credit cards work in a sequential manner:

A credit card is issued with a specific credit limit: When a lender issues a credit card, they set a credit limit for the borrower, which is the maximum amount of credit that can be borrowed. The credit limit is typically based on the borrower's credit score, income, and other factors.

The users make purchases: Credit card users can make purchases at merchants who accept credit cards. The lender pays the merchant on behalf of the borrower, and the borrower is then responsible for repaying the lender.

Banks set up interest rates: Borrowers are charged interest on the amount they borrow, which is typically based on the lender's assessment of the borrower's creditworthiness. Interest rates can vary depending on the lender, the borrower's credit score, and the current market rates.

Users pay back with minimum payments: Each month, borrowers are required to make a minimum payment, which usually covers the interest charges and a portion of the principal. Borrowers can choose to pay more than the minimum to pay off the balance faster and reduce interest charges.

Banks or lenders charge fees: Credit card lenders may charge various fees, such as annual fees, late fees, or balance transfer fees. It's important for lenders to disclose these fees clearly to borrowers.

The user’s credit score is impacted: Borrowers' use of credit cards is reported to credit bureaus, which can affect their credit score. Timely payments can help borrowers build a good credit history and improve their credit scores.

Credit card vs Debit Card

Debit cards and credit cards are both popular financial tools that enable users to make purchases, but they operate differently and offer different benefits. Here are some key differences:

Funding source : Debit cards are linked to the user's bank account and allow for direct access to the user's own funds, while credit cards allow users to borrow money from a lender up to a predetermined credit limit.

Spending limit : With a debit card, users can only spend the money they have available in their account, whereas credit card users can make purchases beyond their available funds, subject to interest charges.

Fees : Debit cards typically have lower fees than credit cards. While some debit cards may have transaction fees or monthly fees, credit cards may have annual fees, balance transfer fees, cash advance fees, or other fees that can add up.

Rewards : Credit cards often offer rewards programs, such as cashback, points, or miles, while debit cards may not have any rewards programs.

Interest charges : Credit card users who carry a balance beyond the grace period are charged interest on the borrowed amount, while debit card users do not accrue interest charges since they are using their own funds.

Credit history : Using a credit card responsibly can help build a positive credit history, while debit card usage does not have an impact on credit scores.

These are the average transaction costs from the top four credit card networks:

American Express: 1.58% to 3.3%

Discover: 1.53% to 2.53%

Mastercard: 1.29% to 2.64%

Visa: 1.29% to 2.54%

These are charged as a percentage of the total transaction volume rather than on a per-transaction basis. Card networks also determine where credit cards are accepted. Card networks are also responsible for any credit card perks/ rewards.

Card networks are on top of the credit card pyramid. They also set and dole out the rest of the fees paid by the merchant to other players. And while the percentage they charge for processing may seem nominal, billions of transactions processed each year (with minimal overhead) add up to a very profitable industry.

What’s more, these card networks have entrenched partnerships and critical technologies that create high barriers to entry for new players.

Card issuers are financial institutions that issue the card network cards to their customers. For instance, ICICI might issue a Visa card. These institutions also issue payment to the merchant’s bank (also called the acquiring bank) on behalf of their customers.

The bank that issues your credit card receives an interchange fee on every transaction. In the case of the ICICI Visa credit card, ICICI would receive the interchange fee. The average credit card interchange fee for a credit card is around 1.81% .

The interchange fee is set by the card network, and the amount is variable depending on a combination of factors like card type, transaction type, merchant type, level of risk for the given transaction and so on.

Processors are technological systems that work with banks and card networks to help merchants accept and process credit, debit , and prepaid payments. They verify transaction details, ensure funds are available, and perform certain anti-fraud measures .

The rates are set by card networks and vary depending on the processing method - if a merchant is using a card reader, they will be charged less compared to a card-not-present processing method like on e-commerce sites.

Processors make most of their money from:

Accepting and processing payments

Settlement of funds

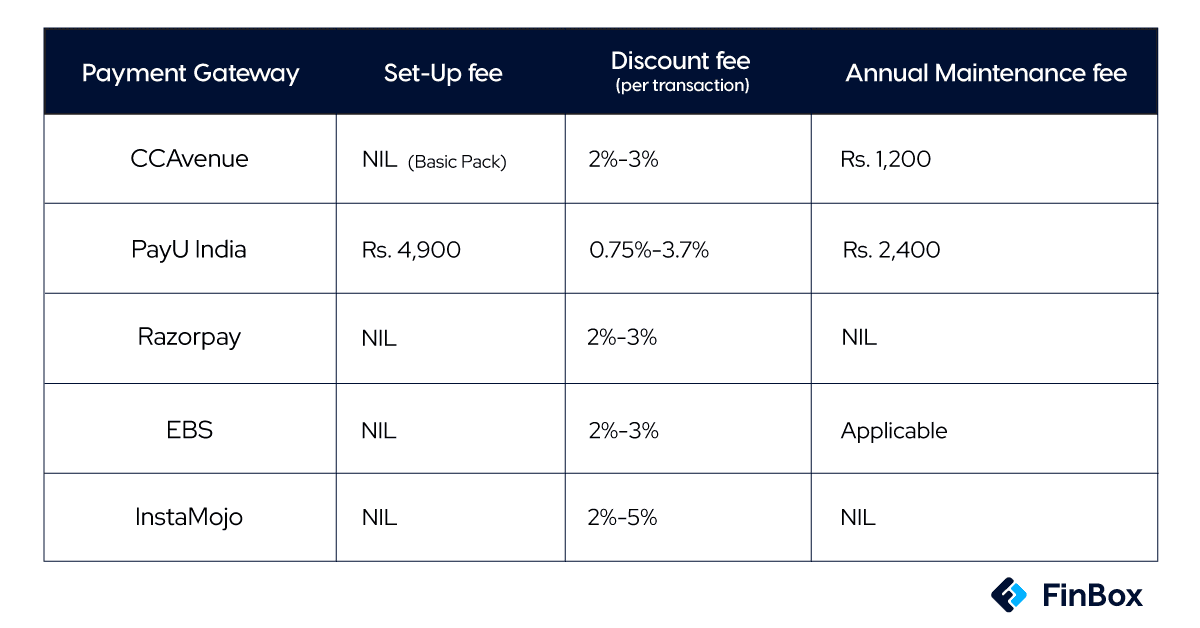

Some of the popular online payment processors in India are RazorPay, CCAvenue, PayUIndia, EBS and Instamojo. Here’s a table comparing the prices they charge

Source:

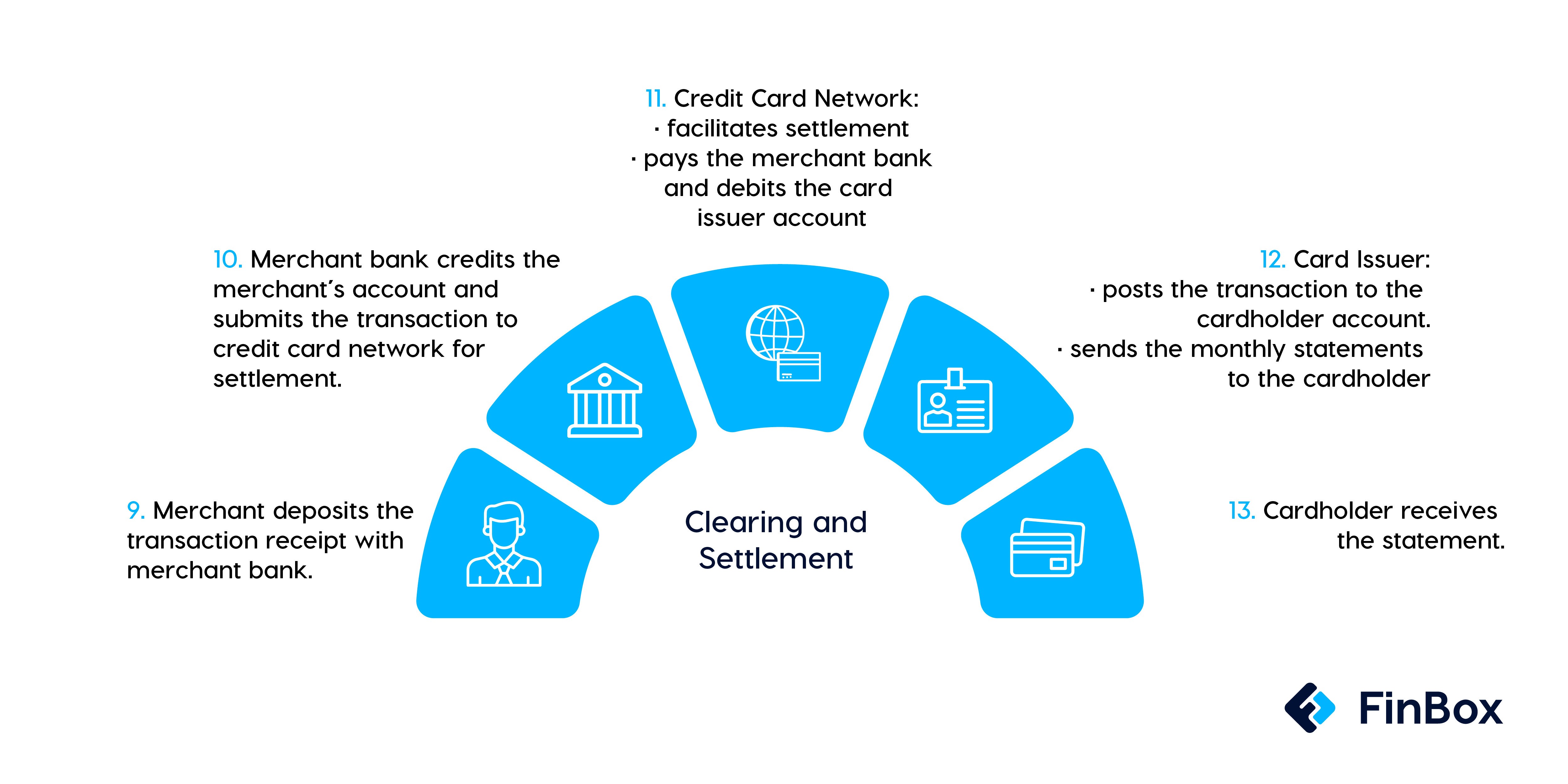

Clearing happens when the issuing bank exchanges transaction information with the merchant’s bank.

The payment processor will connect your card acceptance system to Visa and MasterCard, and each of these card networks have their own system for authorisation, clearing and settlement. MasterCard uses the Global Clearing Management System (GCMS) and Visa uses VisaNet .

They accept transaction data, edit it, assess the appropriate fees, and route the data on to the appropriate card issuer. The clearing messages contain data, but they do not actually exchange or transfer funds, that is done during the settlement process.

The “cleared” transaction is then settled to conclude the process.

This system usually relies on a cardholder signature as an authentication method. When a merchant’s card processing system receives an authorization message, it creates a record through ‘electronic draft capture’ (EDC).

All EDCs in a given period are then lumped together in a “batch”. These batches are processed once a day, however while high-volume merchants may process them multiple times a day, some low-volume merchants may do so less often.

MasterCard and Visa set specific time frames to submit transaction data and transactions should be submitted to the acquirer within that period. The acquiring bank, for its part, has its own time restrictions to comply with for sending that information into network clearing.

Both the card networks receive millions of electronic drafts for clearing each processing data, as you can well imagine, comprising enormous amounts of data. Card networks have built a solid system to handle the traffic.

By crunching all these data, the two card brands are also able to calculate the total amount owed by each issuer and the amount owed to each acquirer.

Then there is an exchange of funds between a card issuer and an acquiring bank to complete a transaction and the reimbursement of a merchant for the amount of each card transaction that has been submitted to the network.

The settlement is done either on an aggregate basis or net basis. This means all credits and debits of a given bank are summed up and the net amount is transferred in a lump sum to the bank’s account with the respective network (i.e. Visa or MasterCard), in the case of an acquirer, or from the bank’s account, in the case of an issuer.

Why should you use Credit cards?

Using credit cards can offer several benefits, including:

Convenience : Credit cards allow for quick and easy payments, making it convenient to make purchases both in-store and online.

Fraud protection : Credit cards often offer fraud protection, which can help protect against unauthorized transactions.

Rewards : Many credit cards offer rewards programs, such as cashback, points, or miles, which can provide benefits to cardholders who use their card frequently.

Building credit : Using credit cards responsibly and paying off balances in full each month can help build a positive credit history, which can be important for future loans or credit applications.

Emergencies : Having a credit card can provide a safety net in case of emergencies or unexpected expenses.

However, it's important to use credit cards responsibly and avoid carrying a balance beyond what can be paid off in full each month to avoid high interest charges and debt accumulation.

What is APR?

Annual Percentage Rate (APR) is a measure of the cost of borrowing money on an annual basis, expressed as a percentage. APR includes the interest rate charged by the lender, as well as any fees or charges associated with the loan.

For instance, if you borrow ₹1,00,000 at a 10% APR for one year, you would pay ₹10,000 in interest charges over the course of the year. However, if there are also additional fees associated with the loan, such as an origination fee of ₹2000, the APR would be higher than 10%, as it takes into account the total cost of borrowing.

APR is often used to compare the cost of different loan products, such as credit cards or mortgages, as it provides a standardized way of measuring the overall cost of borrowing.

Credit cards in India are poised for huge long-term growth irrespective of the regulatory teething issues regarding licensing and capital sourcing. This is because there is a credit appetite that’s going unfulfilled and credit cards are unparalleled when it comes to the flexibility and ease of paying via credit across mediums - online, offline, at gas stations or even at one’s neighbourhood supermarket.

The form factor of a credit card might change and evolve with time (think NFCs, virtual cards, BNPL etc) but the convenience of credit-on-tap is here to stay. A lot of future credit card growth is likely to come from new-to-credit borrowers who enter the formal credit ecosystem for the first time.

Even in this segment, however, the perceived value of a credit product is likely to be much higher than a traditional loan or personal credit line. Hence, the time is ripe for lenders, technology companies and enterprises to foray into the new-age financial services era by introducing truly innovative credit cards that take advantage of cutting-edge underwriting , seamless onboarding and a positive unit-economics structure that ensures that products aren’t just built for vanity - but for business and long-term value creation for the end borrower.

To learn more about the new era of credit without credit scores, consider reading our whitepaper here.

["Credit Cards"]["Financial Service"]["FinTech"]["Revenue Generation"]["Payment Gateway"]["Card Processors"]["Partnerships"]["Underwriting"]["FinTech"]["Fraud Detection"]