Introducing BureauConnect: FinBox’s multi-bureau connector and bureau analytics tool

Aparna Chandrashekar

Content Specialist

|

Oct 5, 2023

Credit bureaus are lenders' first source of truth. However, the true worth of the credit bureau data heavily relies on the breadth and depth of the information and its ability to create value for underwriters.

As a reliable source of data on a potential borrower, banks and NBFCs expect more from credit bureaus than just an aggregation of data points.

However, variations in scoring methods, reporting practices, and algorithms make it ineffective to rely solely on a single bureau’s credit score. Besides, most bureau reports omit predictors like DPD calculations, bureau income, and more.

There’s also a lack of uniformity in predictors, nomenclature, and features among the four bureaus, that might leave potential borrowers unsatisfied.

In this blog, we will discuss why adopting a multi-bureau strategy can aid better lending decisions and how FinBox BureauConnect can get you there.

Harnessing data from multiple credit bureau sources can nearly double the predictive capability compared to relying solely on one source.

Historically, each credit bureau has specialised in specific sectors such as priority sector lending, MSME lending, or insurance, resulting in relative strengths and weaknesses within their respective databases. Consequently, each bureau possesses information that others might lack, implying that while one bureau might be aware of an individual's default on a loan or credit card, others may remain oblivious to this fact - in some cases, at least.

Furthermore, each credit bureau employs its proprietary matching, deduplication, data retention, and processing algorithms. This divergence results in notable variations in the returned data. When comparing bureau A to bureau B and even bureau C, additional credit accounts, historical data, search records, and linked addresses are discovered. Approximately 20% of cases exhibit such disparities , forming influential sets of data swaps at the margins.

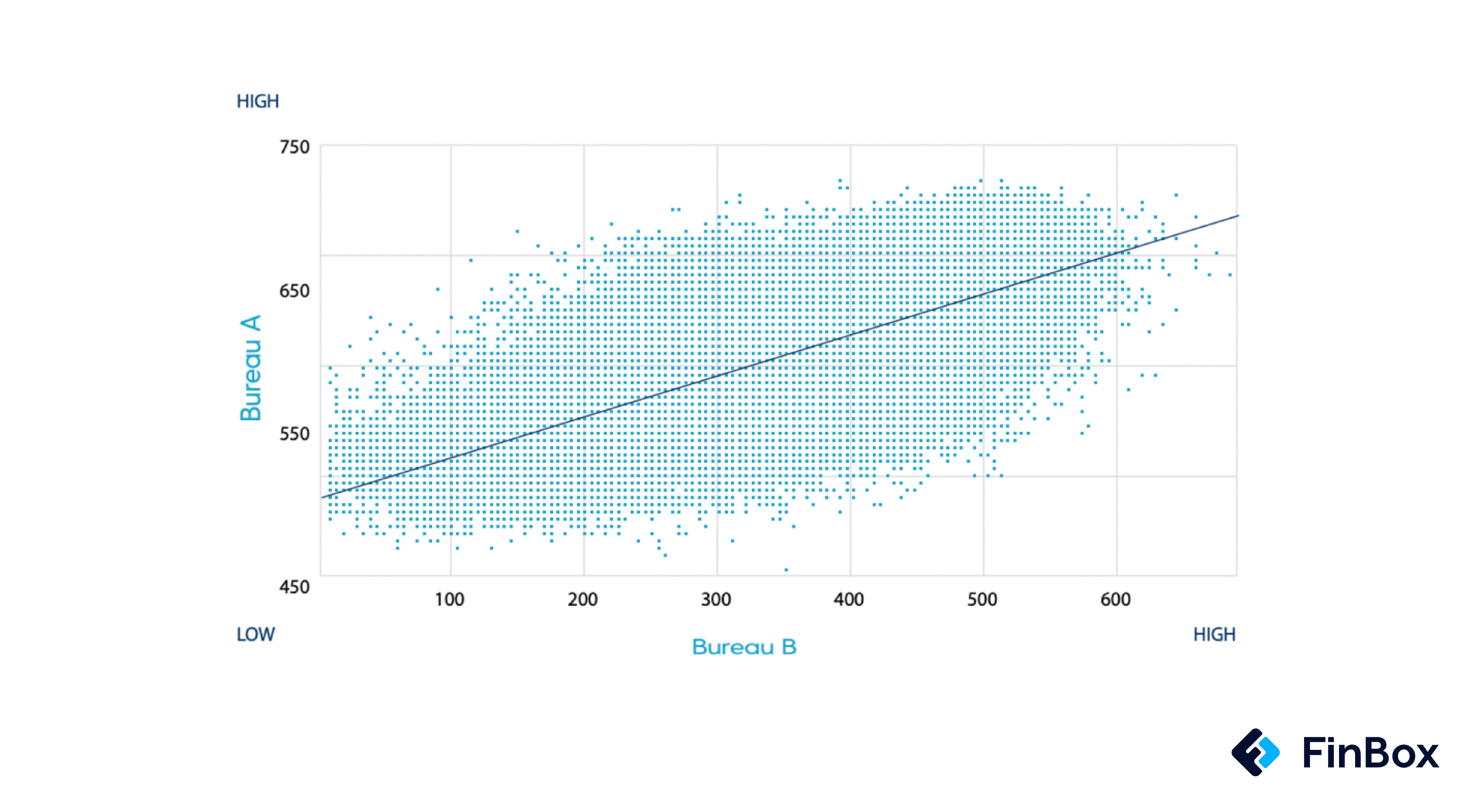

An alternative method to statistically demonstrate this contrast is by comparing two standardised credit bureau scores. In the following graphical representation, we have juxtaposed two generic scores from these bureaus. In a scenario where both bureaus completely agree on an individual's credit score and associated risk, the data points would form a perfect diagonal line on the chart.

Figure: Comparison of Credit Scores from Bureau A and Bureau B

It’s evident from the chart that numerous instances exist where Bureau A could assess an individual as high risk while Bureau B categorises the same individual as low risk, and vice versa. This observation underscores the necessity for adopting a dual or multi-bureau approach to effectively reconcile such disparities.

How FinBox BureauConnect can help

Our Machine learning models provide a detailed view of the entire loan history of the borrower. This includes the following:

Summary of Borrowings – What is the overview status of all borrowings in terms of the number of credit accounts, total outstanding credit balance, credit enquiries, etc.?

Repayment History – Has the borrower been consistent with loan payments and made all payments on time? This can help you gauge the probability that the borrower will meet their payment obligations on time.

‘Enquiry to Success’ ratio – Comparison of the number of loan enquiries made by the borrower and the number of times those were approved.

An essential component within credit reports provided by credit bureaus is the 'Days Past Due' (DPD) indicator. BureauConnect meticulously examines this section, compiling a comprehensive list of all missed instalment payments by borrowers. Additionally, it offers insights into the timeliness of credit card bill payments and whether borrowers have met their EMI obligations punctually.

Additionally, BureauConnect creates over a 1000 predictors over and above bureau predictors that provide deep insights into the borrower and de-duplicates these to give genuine independent matches of that individual. Whether you’re a bank, NBFC or neobank, you can customise predictors as per your lending requirements and business rule engine policies.

All this and more in one, unified format; all presented in a visually accessible dashboard.

The "credit bureau hit rate" is the percentage of successful credit report retrievals by lenders from credit bureaus. Accessing credit information from credit bureaus incurs fees, varying with report type, inquiry frequency, and negotiated terms. Lenders often include these costs in their operations and may pass them on to borrowers.

In certain situations, enterprises may send parameters such as name, mobile number, and email ID to the bureau as part of a request. However, it's important to note that the information requested of the user in the given request fields may not always match precisely with what is stored in the bureau database. This mismatch can lead to the failure of report generation.

At FinBox, we've uncovered the power of a multi-bureau strategy, elevating data coverage by up to 60-70%. This dynamic approach, employing either a sequential ladder or simultaneous parallel call strategy, drives the hit rate to an impressive 75% , far surpassing the 60% hit rate of a single bureau call method

The ladder and parallel call strategies are instrumental components of this multi-bureau approach. The ladder strategy entails a step-by-step inquiry into various credit bureaus, cascading down the list, ensuring that if one bureau lacks sufficient data, the system seamlessly moves to the next, optimising the chances of obtaining relevant information. Conversely, the parallel call strategy initiates simultaneous inquiries with multiple bureaus, drastically expediting data retrieval and delivering an even higher hit rate.

BureauConnect employs Machine Learning models to create a unique credit assessment tool known as the FinBox Bureau Score (FBS). This specialised credit score is formulated by analysing data from various credit bureaus and leveraging predictive indicators. Importantly, it's designed to maintain consistency and uniformity when dealing with data from different bureaus.

Moreover, BureauConnect continually refines these FBS scores to align with the specific lending portfolio of the institution using them. This fine-tuning process ensures that the FBS provides 2x the risk segregation capability of conventional bureau scores, making it a highly effective tool for assessing an individual's creditworthiness. This enhanced ability to differentiate between high and low-risk borrowers empowers lenders to extract greater value from the data obtained from credit bureaus, ultimately leading to more informed lending decisions and improved risk management.

At FinBox, we take compliance very seriously. We ensure none of the bureau data we receive is shared with anybody. The only data we share are predictors that our machine learning models build over bureau data. Despite our specified user licence, we ensure utmost confidentiality and explicit consent with the end borrower in every lending journey. Which is no surprise then, that FinBox BureauConnect is compliant as per RBI guidelines of Credit Information Companies (Amendment) Regulations, 2021 and under CICRA, 2005 regulations.

To attain a comprehensive and coherent understanding of your customers' financial stress and its potential impact on various aspects such as claims and fraud risk, likelihood of policy cancellations, cross-selling opportunities, and loss ratios, it is imperative to adopt a multi-bureau approach.

Working with multi-bureau data presents a unique level of complexity that necessitates specialised expertise, skills, and tools. Only a select few individuals and organisations possess the requisite experience to effectively adopt and effect a multi-bureau strategy.

While it is true that there may be additional costs associated with this approach, the business cases we have developed thus far strongly indicate that the potential benefits far outweigh these expenses. These benefits include:

Reduced time and friction in underwriting

Identify and reduce fraud

Increase approval rates

Improved data capture

The single bureau call approach limits the scope of data acquisition to just one credit bureau, leaving room for potential gaps and outdated information. While it can still provide valuable insights, it falls short of the comprehensiveness and accuracy achieved by the multi-bureau strategy, thereby reducing the lender's ability to effectively assess and mitigate risks.

Adopting a multi-bureau strategy, with its ladder and parallel call options, not only expands data coverage but also significantly enhances the hit rate. This approach is invaluable in the financial industry, where precision and speed in credit assessment are paramount, ultimately leading to more informed and profitable decision-making.

Get in touch for further information!