Introducing Sentinel │ All things BRE, Part III

Anna Catherine

Content Specialist

|

May 14, 2023

We are excited to bring you Part III of our three-part series ‘ All things BRE ’. In Part I , we discussed what a Business Rules Engine (BRE) is, and in Part II , why lenders must upgrade their BREs. In this part, we will explore how Sentinel, a BRE with rule authoring and risk intelligence capabilities, helps lenders go from ‘zero to one’ and then ‘one to N' in digital credit, at speed.

In light of digitisation, a dominant assumption in the lending industry is that loan officers’ discretion gets curtailed by automated lending workflows. This could be true to a considerable extent when business rules are hard-coded into application software. In Part I , we saw how hard-coding makes it difficult for risk teams to modify or update business rules, making lending systems ineffective, complex, and inflexible.

This is less than ideal in the credit world as macroeconomic, regulatory, and business environments change a little too often and we have seen just how much in Part II of this series.

Even if risk teams were to find ways to adapt, the challenge is that development teams typically take 3-4 weeks to reprogramme digital lending workflows accordingly — which is lost time for lenders.

For agility to be a realistic feature of modern lending businesses — the business rules that power credit decisioning should become flexible. For digital lenders that do use a business rules engine, the question is whether to shift to a feature-rich BRE , one that offers more value.

An automation solution that empowers digital lenders with agility, scalability, and flexibility is the need of the hour.

Presenting Sentinel: A smarter, faster Business Rules Engine

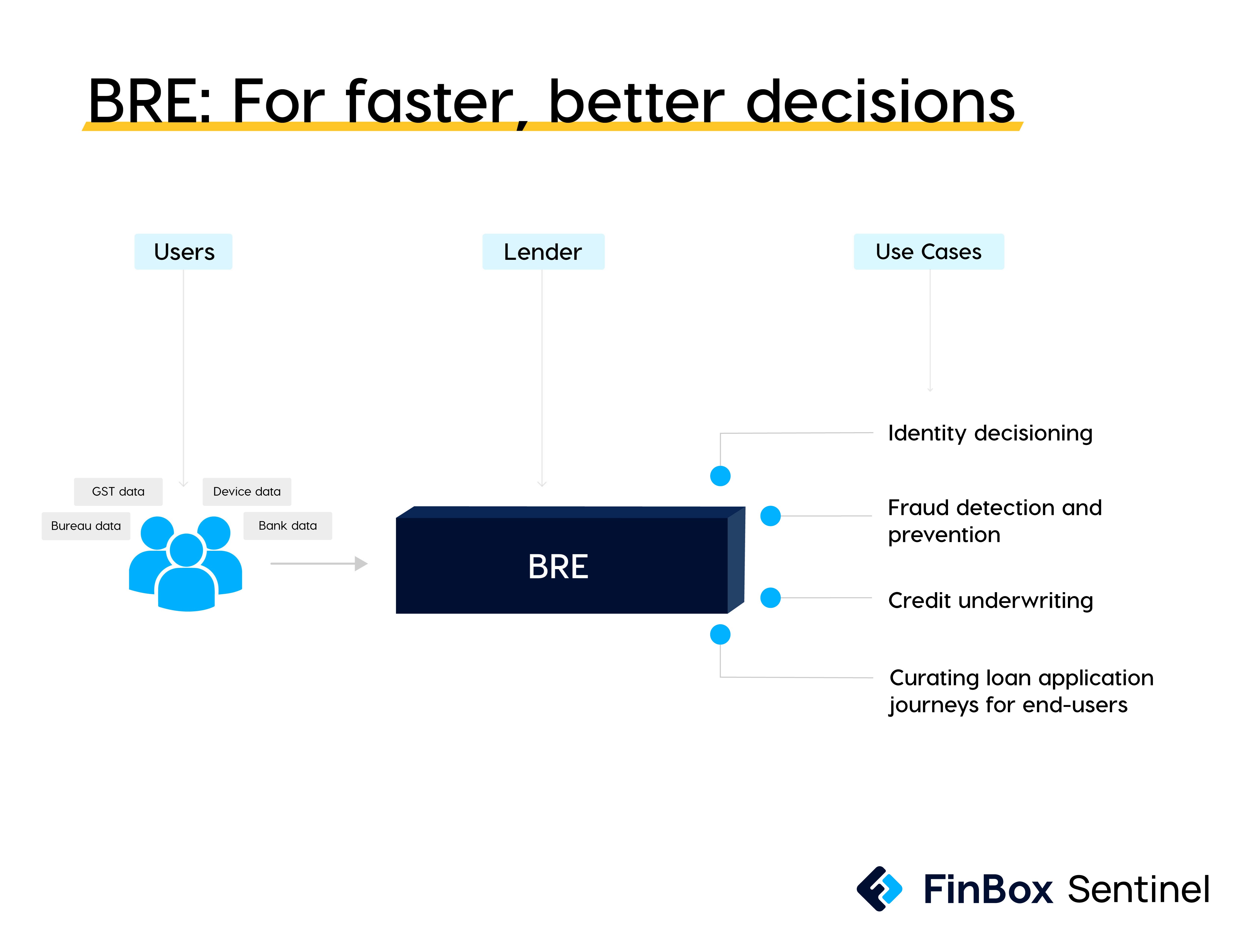

Sentinel is a next-gen decision management system powered by big data analytics. It has two core elements — business rules engine (for decision & workflow automation) and risk intelligence.

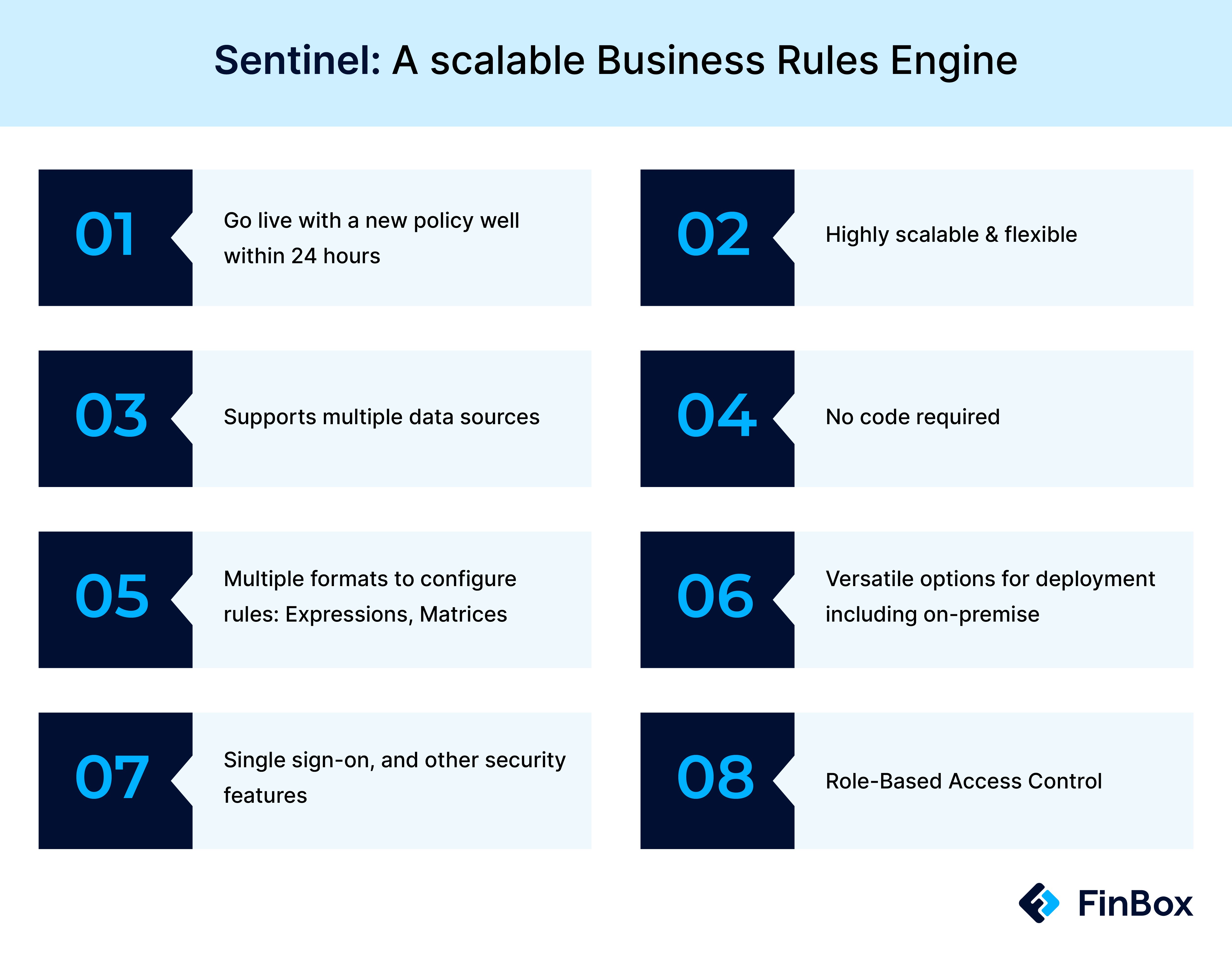

Sentinel allows business analysts or subject matter experts to create, modify, and manage business rules without having to write code. The Sentinel studio provides a graphical user interface (GUI) that enables users to add as many data sources , and define logic for identity verification, credit underwriting, and fraud either in the form of expressions or matrices. With ready templates and import features available on the studio, it’s safe to say that lending policy creation and editing has never been easier. Users can test rules or workflows, particularly complex ones, right when they are creating them. In fact, one can even control end-user journeys on any platform using Sentinel’s workflow automation capability.

Sentinel’s big data capabilities enable superior decision-making. Sentinel has an in-built simulator that replicates real-world environments much like flight simulators. While the latter trains pilots to fly through thunderstorms and hurricanes, Sentinel’s simulator trains risk teams to navigate policy changes, business goal realignments, and other upheavals in the course of lending operations. How? Users have three options for simulating these scenarios which are elaborated in subsequent sections.

Basically, Sentinel helps lenders cross over from automation to intelligent automation. What the industry has been building thus far are ‘digital lending arms’ that are trained to do repetitive tasks at scale — it’s a lot like muscle memory. But what if these digital lending arms could have a mind of their own?

Sentinel is to the lending system what the brain is to the nervous system

Simply put, Sentinel is a self-service technology for lending policy creation and business intelligence. It sets in motion a library of business rules powered by decision tables that can run into millions of rows and columns. It processes billions of data points to make various credit decisions such as:

Are applicants who they claim to be?

Has an applicant committed fraud or fudged their data to be eligible for the loan?

Does the applicant belong to low-risk, medium-risk, or high-risk category?

What interest should be charged?

What should be the tenure of the loan?

Isn’t this much like the human brain — the way we determine our spending limit, verify the authenticity of products we buy, or decide how much to speed on a highway based on our individual perception of risk? Besides enabling such decisioning, Sentinel also has memories and generates ideas, much like human cognition. Here’s how.

Sentinel’s simulator enables risk teams to test different lending strategies. Let’s say you want to test a lending policy’s performance with the aim of approving a certain risk segment among previously rejected customers. Sentinel provisions for three methods for such simulation testing . One is the ‘historical method’ where you can retrieve all historically approved, rejected, and reserved users of select policies within a specific date range and run your new policy on these users.

The second method is as easy as selecting Customer IDs of all the users you want to assess with respect to a specific lending policy. Sentinel will fetch the predictors for the selected users and run the rules engine to generate a result — that comprises information on which applications qualified and the corresponding loan offers generated.

The third method allows you to upload a .csv file containing customer data to run a simulation. Now, in case you don’t have historical data for simulation testing, you can do simulation testing in a live environment, what we call Canary Testing — a unique feature of Sentinel.

You can also release a test policy to a subset of users in a phased manner using Champion/Challenger Mode to mitigate the risk of adverse impacts on operations, business outcomes or customer experience. You can also set benchmarks at the rule level and policy level to serve as reference points for comparing and measuring different lending activities and performances. All these are clearly systematic means for inductive reasoning, which is nothing but ideation.

Sentinel records every rule, function, or matrix ever published along with metadata such as author, data of publishing, etc, thereby, allowing users to trace any version of rule or policy and rollback changes . In fact, rolling back to a previous policy version is a one-click job on Sentinel. This makes the whole lending process traceable, replicable, and auditable.

Sentinel stores all structured and unstructured data that was ever routed through the BRE, both input and output data, in an anonymised and encrypted format . Besides storing this information, it also analyses it to deduce macro-level trends such as demographic, behavioural, and other multi-faceted data patterns. That’s not all. Another exciting feature of Sentinel is the Risk Connector. It processes data pertaining to loan recovery and delinquency to give feedback to risk teams on what worked and what didn’t.

Simply put, it perceives the credit market and tells you how to react to it.

Sentinel is pure processing power to turn data into action… superfast

To make the best decisions we need as much information as possible. Similarly, lenders would want access to as much data as possible to make the best lending decisions. Sentinel connects lenders to a host of data sources on the FinBox Data Platform (FDP — ranging from bureau to other powerful alternate data sources.

One has to simply select data sources of their choice or can go with FinBox UIS score — a single credit score generated by unifying insights from multiple separate sources on FDP. If the lender wishes to utilise its own credit scoring system or incorporate custom data into the decision-making process, this can also be done through Sentinel's Custom Input method. The idea is simple — more the data, better the decisioning.

Sentinel is designed to put core-decision makers in full control of everything that’s going on inside the lending workflow and at the same time empowers them to react to everything outside the workflow. To better understand how Sentinel’s prowess helps you realise your full lending potential, get in touch with us .

Sentinel, Business rules engine, BRE, policy creation, no-code, identity decisioning, underwriting, fraud prevention, credit decisioning