How to build a purchase order financing solution and its efficacy in boosting B2B commerce

Shamolie Oberoi

Content Marketing Specialist

|

Oct 11, 2022

Healthy credit access is the fertilizer in which a business blooms. Even Jeff Bezos got a USD 245,000 loan from his parents for an early internet business venture. But unfortunately, most business owners don’t have the luxury of wealthy parents to fall back on.

That’s where formal and personalized credit products come into play. From cash flow-based lending to merchant cash advances, there are different lending solutions that address business’ working capital needs and allow them to fulfill orders without disrupting cash flow and business as usual. In this piece, we’re talking about one such solution - purchase order financing (POF) - and its benefits to both businesses and e-commerce platforms that tend to aggregate these businesses.

What is purchase order financing?

POF is a commercial financing option that allows suppliers to be paid upfront for verified purchase orders. While traditional supply chain finance methods fund an invoice (and therefore only the payment terms), funding a purchase order reduces financing costs and friction across the whole chain.

Here’s a snapshot of how POF works

A business receives a purchase order from a customer - it should specify the type and and volume of goods to be purchased

If financing is needed, the businesses consults its supplier to estimate costs involved for the ordered goods

The business then applies for financing after estimating and confirming the involved costs. The lender will typically approve financing for up to 90% of the total cost

The lender pays the supplier based on the POF application. The supplier then has the funds to begin work on the order

The goods are delivered to the customer. The business then invoices the customer for the fulfilled order

The customer makes the payment towards the POF lender

The lender deducts their fees(essentially the interest on the amount lent) and forwards the business the remaining sum of the proceeds

Who uses purchase order financing?

Purchase order financing is typically used by small and medium-sized businesses that need short-term funding to fulfill large customer orders. This type of financing is particularly useful for businesses that don't have enough cash on hand to purchase the materials and produce the products needed to fulfill the order.

Here are some businesses that might use purchase order financing:

Manufacturers

Wholesalers

Distributors

Importers and exporters

How is Line of Credit used for purchase order financing?

A line of credit can be used for purchase order financing to help businesses cover the costs of fulfilling large customer orders. Here’s an easy example to break it down:

Let's say a small electronics manufacturer receives a large purchase order from a major retailer for ₹1,00,00,000 worth of electronic devices. However, the manufacturer only has ₹20,00,000 in cash available to purchase the necessary materials and components to fulfill the order.

To bridge the funding gap, the manufacturer applies for a line of credit with a lender that specializes in purchase order financing. The lender reviews the purchase order and the creditworthiness of the retailer and approves a ₹1,20,00,000 line of credit for the manufacturer.

The manufacturer draws ₹80,00,000 from the line of credit to purchase the necessary materials and components to fulfill the order. They then use the remaining ₹40,00,000 from the line of credit to cover other costs associated with production, such as labor and overhead.

Once the order is completed and delivered to the retailer, the retailer pays the manufacturer ₹1,00,00,000 for the order. The manufacturer then repays the lender the ₹1,20,00,000 drawn from the line of credit, plus any fees and interest charged by the lender for the financing.

Pros and cons of purchase order financing

Purchase order financing can be a useful tool for businesses that need short-term funding to fulfill large orders. However, like any financing option, it has both pros and cons. Here are some of the key advantages and disadvantages of purchase order financing:

Pros:

Provides short-term funding

Improves cash flow

Easy to qualify

No collateral required

Cons:

Higher cost

Limited funding

Limited customer base

Limited industry applicability

Alternatives to purchase order financing

While purchase order financing can be a useful option for businesses that need short-term funding to fulfill large orders, there are also other financing options available. Here are some alternatives to purchase order financing:

Traditional bank loans : Traditional bank loans can provide businesses with long-term financing to cover a range of expenses, including the costs associated with fulfilling large orders. However, these loans typically require collateral and a strong credit history, and the application process can be lengthy.

Invoice factoring : Using invoice factoring, businesses can sell their outstanding invoices to a third-party company for immediate funding. This can help businesses improve their cash flow and cover expenses associated with fulfilling orders. However, factoring companies typically charge high fees and may require businesses to have a certain level of monthly revenue.

Merchant cash advances : This provision allows businesses to begin the trade with a lump sum of cash in exchange for a percentage of their future credit card sales. While businesses can have quick funding with merchant cash advances, the high fees and interest rates associated with merchant cash advances can make them a costly option.

Supplier financing : Supplier financing involves negotiating payment terms with suppliers so that they can delay payment until after they have received payment from their customers. This can provide businesses with more time to fulfill orders and improve their cash flow.

Why this is the right time to build a digital credit offering

India is among a handful countries that boasts a robust public infrastructure, which has made it possible to build solutions like UPI and Account Aggregator that are transforming both payments and credit respectively. Now, the Indian government is doubling down on its push for digital finance products, specifically targeted towards MSMEs.

This, alongside the boost in digitization led by the pandemic, has created an enabling environment for platforms looking to offer B2B digital credit solutions such as POF. However, as seen from the process above, a solution like POF involves several complex processes and multiple moving parts. Building this in-house requires massive financial and human resources, to say the least.

The cost and time-effective approach would be to partner with a FinTech that specializes in digital credit infrastructure. They can provide easy-to-integrate APIs and SDKs that can drastically reduce your new offering’s time to market.

What are the benefits of POF for businesses?

Since suppliers are paid directly by the lenders, businesses don’t have to worry about acting as middlemen in the processes

The inflow of credit allows businesses to take orders they may not have been able to fulfill otherwise due to emergencies or a cash crunch

While finding the right financier may take time initially, the process be becomes faster and more simplified once a relationship has been built

It’s relatively easier to qualify for purchase order financing even without a comprehensive credit history and immovable collateral

Why should B2B E-commerce platforms offer a POF solution?

Let’s take a current example of festive-season sales. Purchases skyrocket during this period (for example, at the time of writing, 60-70 lakh mobile phones have been sold within the first four days of major e-commerce players kickstarting their festive sales).

Merchants thus need to up their inventory in order to match increasing demand, and the e-commerce platform places early orders inventory. In order to facilitate this, the platform itself can offer purchase order financing to enable merchants to procure the volume of products needed. It’s a win-win situation for both parties involved.

Other benefits to the platform include:

Increased conversion rates and thus, higher revenue

Higher average order values

Streamlined user experience

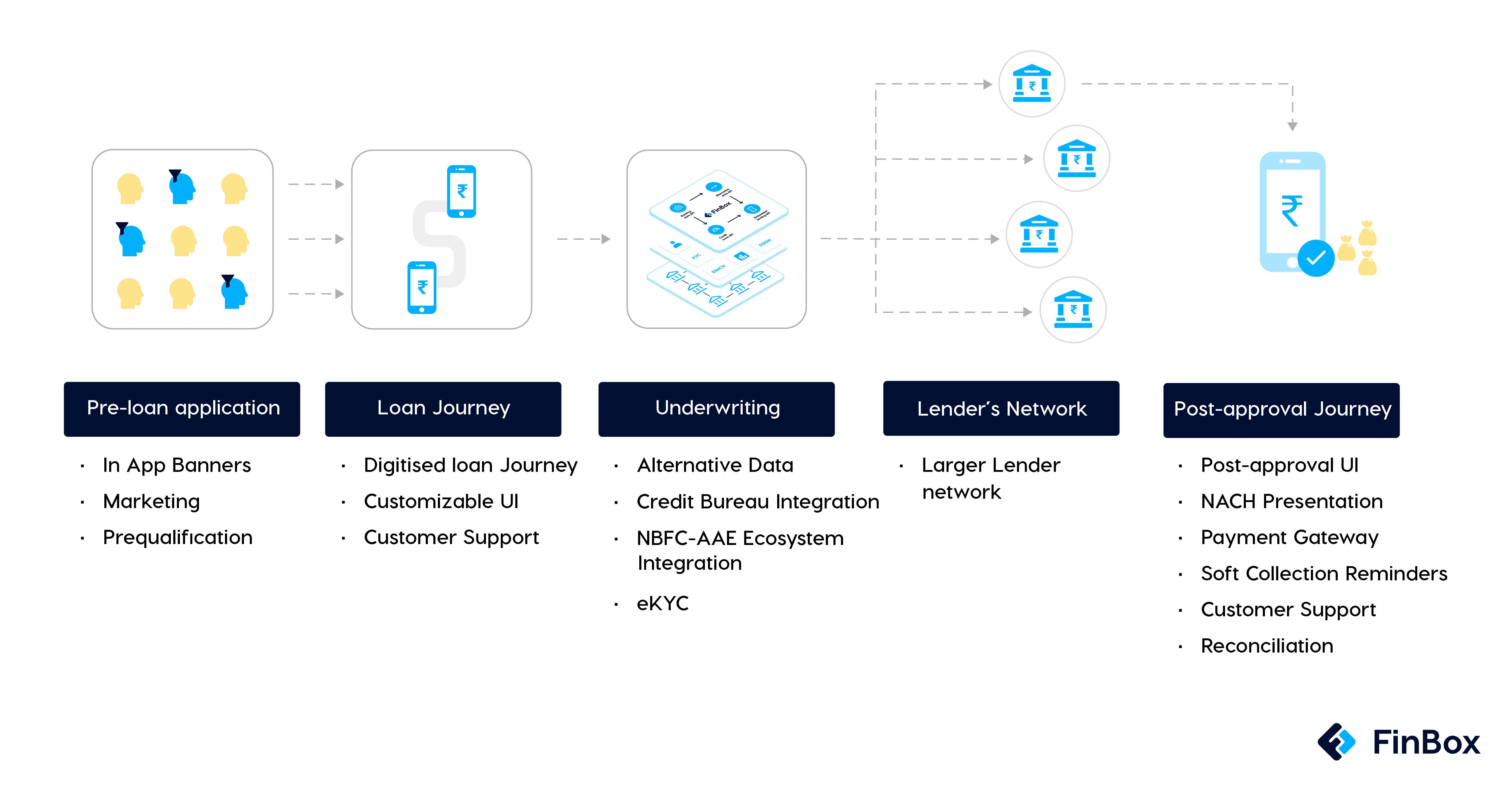

Building one’s own POF lending solution involves creating several layers as part of a lending stack:

A lender network that will provide the required capital

A KYC suite that should enable user authentication through Aadhaar, PAN authentication, bank account validation etc

An underwriting suite built on both traditional and alternative data points for accurate risk assessment

An automated collections solution to recover loans with relevant nudges and communication

If you would like a faster and easier way to begin offering POF to merchants, get in touch with us at FinBox - our end-to-end lending infrastructure will have your POF solution up and running in no time! Contact us here.

["FinTEch"]["Financial Inclusion"]["Banking as a Service"]["Digital Lending Infrastructure"]["Alternate Date"]["Underwriting"]["Risk Assessment"]["Fraud Prevention"]["Collection"]["Credit Score"]["Account Aggregator"]