The digital-first guide: How NBFCs can launch and scale their digital offerings

Aparna Chandrashekar

Content Specialist

|

Feb 9, 2023

Digital credit is no longer a good-to-have, it is table stakes. Any lending NBFC worth its salt today must be looking at digital lending as the holy grail of building a resilient business. This is so because digital lending is on its way to dwarf other sources of origination and with digitalized lending operations come better conversions, stronger unit economics as well as much higher customer retention and the ability to cross and up-sell various other products within the right context.

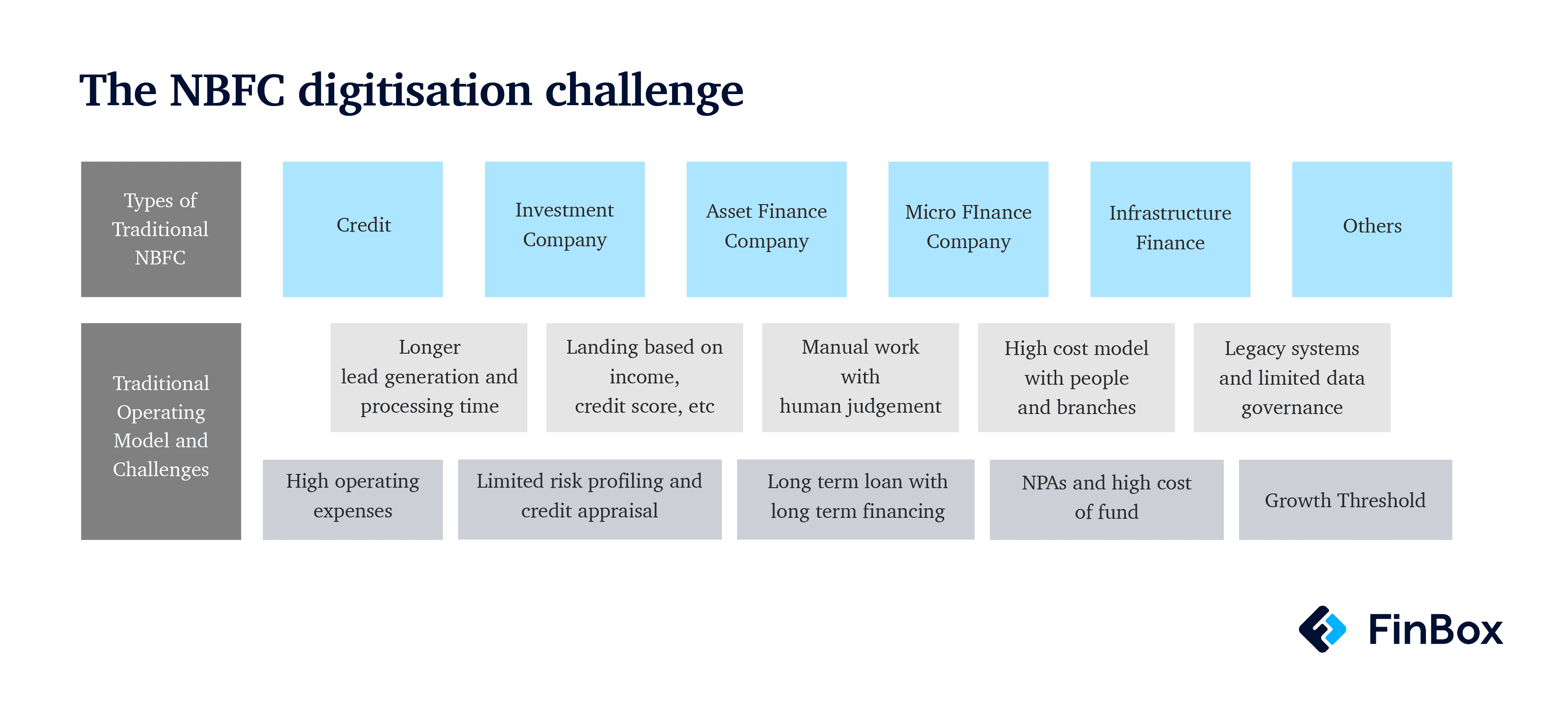

However, digital transformation is a big phrase that often means a daunting amount of work, resources, as well as time to come to fruition. And more often than not, digitisation is viewed as getting your hands on the latest technology. And that’s the easy part but the part where most NBFCs that want to be ‘digital first’ struggle with are -

Setting up dependable integrations with partners

Building and scaling new products

Managing third-party loan sourcing agencies with ease and reliability

Streamlining siloed data to create value

Launching a dynamic B2B credit programme

Strengthening co-lending models

At the core, digitisation is really about turning this overabundance of data into a gift that keeps giving and that’s where technology comes into play. However, take it from us - building technology that's reliable and scalable is easier said than done. Nearly 100s of employees and half a decade later, we can safely say that FinBox has built the technology that can future-proof NBFCs for a hyper-digital world.

But this isn’t to say NBFCs can’t do that; the way we look at it, we want NBFC lenders to continue doing what they do best - distribute credit where it’s needed the most in the most efficient way possible without having to worry about building the necessary technology or digital credit expertise and systems in-house.

In this blog, we’ve designed a six-pronged approach that will help NBFCs face stiff competition from micro-lenders and fintech start-ups that have ventured into the INR 118 trillion Indian formal credit market.

The six-pronged tech-driven, low-cost operating model for NBFCs in digital credit

The easy part of the partnership piece is finding partners. Lender partnerships are important for platforms and vice-versa, so every player in the ecosystem is eager to forge partnerships with each other. However, the tough part is hard integrations across the journey - from prequalification, funding, loan journey, underwriting, the disbursal and collections. Every step of the loan requires innumerable, individual integrations, which could take anywhere between 6 months to a year to complete.

Besides, integrating every partner with different types of loans - be it BNPL, credit lines, invoice financing or sachetized loans - is tedious. Factoring the time taken to design a native-looking journey across partners can make it more intimidating. The FinBox approach to partnerships is one Software Development Kit (SDK) with six lines of code that instantly supports multiple journeys across multiple platforms and integrations across the stack - Penny drop, payment gateway, E-Nach + GST, KYC, and credit bureaus. A one-stop shop to lower acquisition costs for high-quality borrower pools and grow the loan book!

Traditional loan management systems (LMS) and the ecosystems around them weren’t built to support new credit products like BNPL - they can’t support the high volumes, shorter repayment cycles, the credit risk that comes with lending to NTC borrowers, the integrations required with partner platforms’ payment gateway for a smooth checkout, and the new regulatory requirements.

Lenders may face similar challenges with products like EDI, sachet loans or co-lending. Pricing, amortisation schedules, and collection efficiencies can be challenged with every new product. The solution? A modular stack that is flexible, configurable and dynamic. This stack should typically be entirely API-based, come with pre-built integrations with partners and host an externalised business rule engine that can be modified according to the product.

Loan distribution for NBFCs and banks is largely dependent on third-party agencies and DSAs - they account for 30% of lenders’ retail books on average. But the challenges with DSAs for most lenders are mis-selling, diffused focus, attrition, lack of transparency and high turnaround time (TAT).

It’s imperative then to invest in a modern, technology-driven DSA management system that streamlines all the data and ensures lenders have a real-time view of every loan application and one that also ensures DSA incentives are managed thoroughly. FinBox’s DSA management module easily integrates into existing apps for DSAs or other partners. Our no-code module seamlessly blends with your branding and offers custom journeys. On the off chance that you don’t have an app yet, our microsite ensures you still have independent journeys for your DSAs. This module provides complete control, deep analytics and super effective DSA operations with the capability to scale loan books without worrying about the red tape.

Going digital entails customer segmentation, which remains a pressing challenge for NBFCs. Leveraging analytical tools for customer segmentation, and designing segment-specific sales strategies can lead to better conversion rates, present cross-selling opportunities around every bend, and improve collections efficiencies. These analytical tools usually come from carefully developed tech-driven products that can provide a 360-degree view of a customer. At FinBox, products like DeviceConnect, BankConnect , MarketX and CollectX have underwriting, customer-segmentation and collection capabilities that ensure 3x more conversions, and 50% higher collection efficiency.

Trade credit has existed for quite some time in the B2B market - but creating a modernised BNPL offering looks very different. BNPL for retail consumers works because it is merchant-funded and largely impulse driven. High-margin, discretionary items were offered with no interest, catalysing customer motivation. However, B2B purchases are need-based and hardly ever driven by impulse or competitive pricing. BNPL for consumers also has low ticket sizes, compared to B2B BNPL. While consumer BNPL is driven by a streamlined, single workflow, B2B BNPL is subject to more variability and complexity. Plus businesses have more stakeholders throughout the process - sourcing teams, budget owners, end users and accounting departments. The complexity increases, for instance, if approvals for purchase are required at the point of order and not the point of payment. Businesses applying for a BNPL loan should be able to

Apply in minutes

Get on-demand funding

Be eligible for faster credit decisions

Co-lending allows NBFCs to seek funds at a low cost from banks. The 80:20 model ensures that NBFCs don't originate poor-quality loans as their 20% stake would be severely impacted in case of any losses. But the co-lending mechanism is a win-win for all parties involved - banks, NBFCs and borrowers. The challenges arise when it comes to aligning credit policies, complex accounting, whether or not banks can trust loans originated by NBFCs, and the different regulatory standards around KYC and collateral norms for banks and NBFCs. The FinBox co-lending stack ensures

A Business rule engine that runs parallelly between banks and NBFCs

A single dashboard to manage disbursals and repayments

An LMS bridge to support multiple LMSes

A dashboard for automatic analytics, reporting and ticketing.

Conclusion

At its core, digitisation is slower among NBFCs due to legacy infrastructure, technologies used, frameworks, approval processes and tight-knit integration across business and technological value chains. Not to say NBFCs are not innovating - the challenge is to identify which ideas to actively pursue at the intersection of capital and technology. The value infrastructure players like FinBox bring is the capability to break down complex systems into smaller, more agile modules, so NBFCs can improve efficiency, reduce risk, and increase scalability. The innate customer insight that NBFCs come with coupled with the agility and technology of fintech infrastructure players acts as a great equaliser.

Get in touch with us today for a demo!

["NBFC"]["Digital Credit Infrastructure"]["Customer Retention"]["B2B Credit"]["Co-Lending"]["FinTech"]["Credit"]["BNPL"]["LMS"]["DeviceConnect"] ["BankConnect"] ["MarketX"] ["CollectX"]["Credit Policies"]