Why lenders need an agile, no-code Business Rules Engine │ All things BRE, Part II

Anna Catherine

Content Specialist

|

Sep 27, 2022

In part I of our three-part series ‘All things BRE’, we discussed what a Business Rules Engine (BRE) is and touched upon how standard BREs make lending processes inflexible.

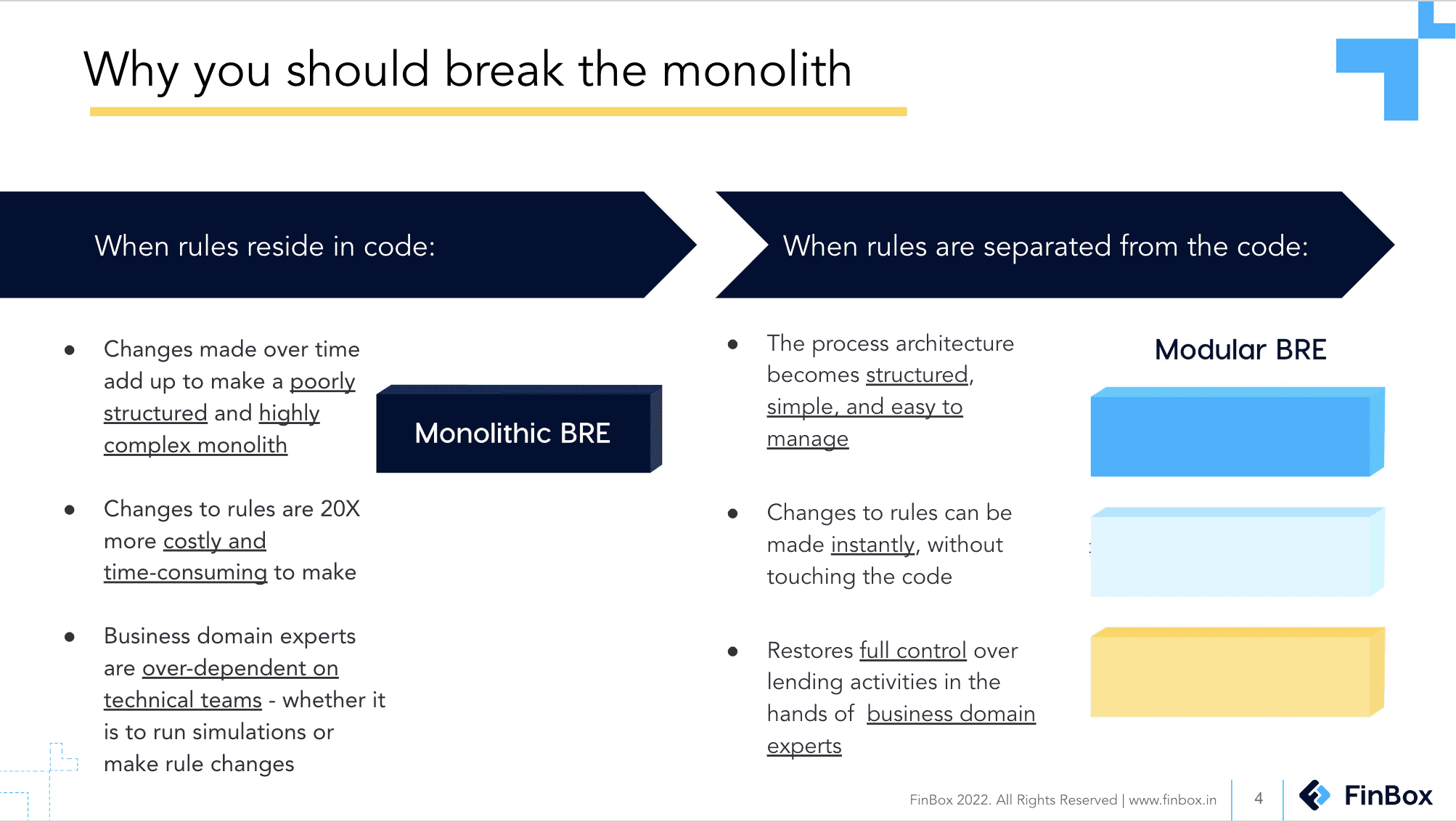

Every time business and risk teams at lending organisations want to change business rules, they have to rely on IT teams and wait 3-4 weeks to go live with a new/modified lending policy. This is bound to happen when credit decisioning logic is embedded in code. Inflexibility of credit decisioning processes that run on standard BREs is a major pain-point felt across the industry. This is solvable by adopting a modular approach.

In this blog, we shall delve deeper into why lenders must upgrade their BREs and why it is crucial for them to be able to automate decisioning, without having to code .

Why lenders need no-code automation capabilities

Amid the storm of crises and disruptions, leading financial institutions are recognising risk’s strategic and resilience-building role. Chief Risk Officers (CROs) and Risk Heads are consistently tasked with the responsibility of ensuring business continuity as the global economy faces ongoing disruptions caused by various factors such as pandemics, financial crises, inflationary pressures, and technological and social movements. In fact, contending with persistent and dynamic disruption has become a fact of life for CROs of financial services companies.

To better understand the magnitude of the challenge CROs face, let’s consider the following scenarios.

How a business rules engine helps adapt to evolving regulations

Interest rate risk is fundamental to the business of banking. And recently RBI has been on a rate hike spree — a 140 basis points increase in just four months — jolting banks out of their four-year long comfort zone of an unchanged 4% repo rate .

Such a rising rate environment combined with flattening yield curve as has been the case since June 2022 — is basically ‘interest rate risk’ entering the danger zone.

In such a scenario, a lender should be able to adjust digital lending workflows quickly to account for this risk or it may affect net earnings adversely. But to adjust lending workflows — whether it is to create or edit a policy — lenders must deploy considerable IT resources for a good 3-4 weeks.

This doesn’t exactly scream ‘agility’ and the inefficiency of the process cripples lenders’ ability to respond to changes in the regulatory environment at speed.

The key to achieving agility lies in building self-service capabilities — the new mandate of a BRE .

How a business rules engine helps tackle unceasing uncertainty

CROs must deal with not just what’s happening but also what may be about to. For example, RBI’s current stance on First Loss Default Guarantee (FLDG) points to the imminent death of FLDG agreements. This is likely to turn current lender-fintech partnerships on its head, requiring lenders to amend and redeploy their lending policies.

But how do you amend a policy when you don’t know what amendments will work? Shots in the dark can end up becoming costly mistakes. This is why risk managers sit with IT teams and run simulations to arrive at optimal cutoffs for maximal approval and lowest risk. This is a trial and error method and hence long-winded. It does not help matters, when risk teams need tech support to run every simulation.

Well, only if credit risk teams had the kind of simulators aviation students do. In a simulated flight, you have the freedom to make mistakes that might be impossible to survive in the ‘real world’. Similarly, a smart BRE should be able to offer risk teams the benefits of a simulator to practise, identify, assess, and mitigate risk .

How a business rules engine helps lenders cope with macroeconomic hiccups

The one risk issue that garnered maximum CRO attention in the last 12 months was credit risk, according to EY . This is not surprising, considering the economic upheaval caused by the pandemic. The most touted solution for this is data-led credit risk modelling, and rightly so. But what use is knowing the likelihood of default unless lending policies can respond to it at speed? This is where modern BREs that enable ‘ policy creation without coding ’ shine. They dramatically shorten the time it takes users to make changes — from weeks to a matter of minutes.

A business rules engine for testing new growth strategies

Financial inclusion is no longer just a welfare goal but a major growth opportunity — thanks to alternative data and cost-effective tech-enabled distribution. Put simply, embracing risk is the new growth strategy. Whether you want to lend to new risk cohorts, or leverage risk-based pricing — the ability to optimise your lending policy becomes crucial. With an agile BRE, risk teams can do this instantaneously without touching the code. Besides cutting dependency on development teams, a functionality-rich BRE can add one more incredible advantage — eliminate human error.

Mind you, eliminate, not just reduce. How? It’s called validation . Typically, you run the risk of basing decisions on incomplete rule sets that may not accurately or fully represent the situation at hand. Such lacunae in policy formulation can be solved at the validation step. There are BREs out there that double up as compilers to ensure error-free execution.

Bottom line

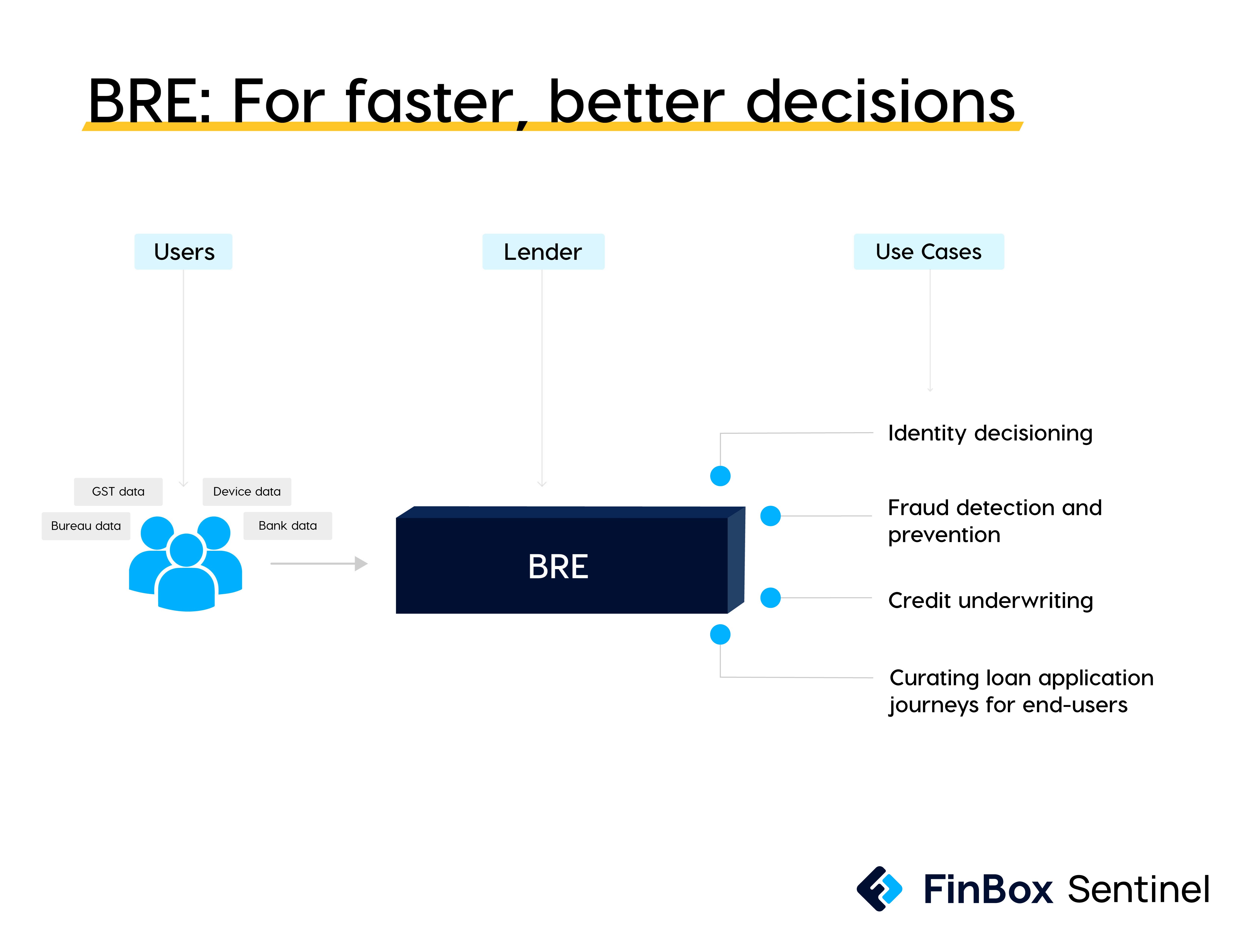

BREs can empower financial institutions to streamline important decision-making processes involved in lending — whether it is for onboarding, underwriting, or even controlling end-user journey.

Risk leaders are realising that they can do more and do better with smarter credit decisioning systems enriched with alternate data. Additionally, BRE has the power to restore full control over lending activity with core teams of financial institutions. More importantly, it’s the door to agility.

This blog is the second part of our three-part series ‘All things BRE’. In Part I, we discussed what a BRE is, and in this blog (Part II) why you need an agile BRE. Watch out for Part III to know all about how FinBox is approaching this challenge.

["interest rate"] ["lending"]["onboarding"]["Business Rules Engine"] ["Chief Risk Officers"] ["decisioning automation"] ["Identity decisioning"] ["fraud decisioning"] ["credit underwriting"] ["Sentinel"]