The Pattern #134

Did the FinTech rocketship overheat the lending stratosphere?

Mayank Jain

Head - Marketing and Content

·

Mar 15, 2024

Hello everyone,

Welcome to the 101st edition of The Pattern, a weekly newsletter where we dive into the latest from the world of economy, finance and technology. Let’s get started.

Dying stars burn the brightest?

Excess of everything is bad. It’s something we’ve all heard, learned and internalised but it’s the consumer lending FinTechs that are now on the receiving end of this harsh reality.

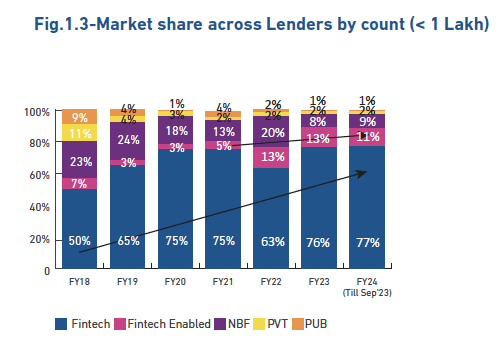

For a while now, FinTechs have progressively eaten into the market share of public and private banks by capturing a majority of the new-to-credit borrowers along with creating a specialized niche for quick, small-ticket lending. For loans below INR 1 lakh, FinTechs have a market share of a whopping 77% by the number of loans and more than 50% by the total value disbursed. This data is from the latest Experian report titled “Charting new horizons for Fintech lending.”

This is a leap unlike few seen before. The total annihilation of legacy lenders from the forefront of digital consumer acquisition for sachet loans is a bragworthy achievement.

But, the arms race it started is now threatening an entire industry’s stability. As FinTechs raced to the front door and grabbed young borrowers – banks and NBFCs decided they didn’t want to sit around and watch. And hence, started a wave of digital origination, partnership-based-lending , third-party origination, banking-as-a-service and what have you.

The idea is simple – if the FinTechs can do quick onboarding and disbursal of personal loans, then legacy players can too. They have more experience, better offline reach and simply more hands on the deck. What they didn’t have was a digital presence and that changed with the arrival of infrastructure companies such as FinBox that enable transformation of entire product, processes and business through risk products and API stacks.

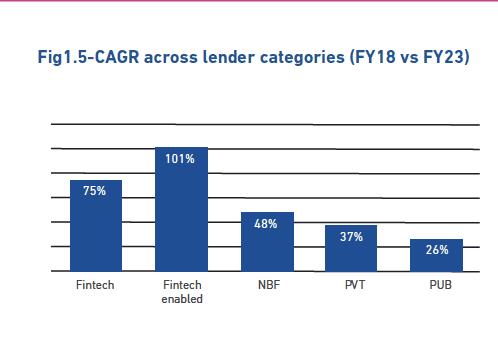

The result? FinTech-enabled lending grew with triple-digit CAGR between FY18 and FY23 – effectively meaning that even NBFCs and banks got a chance to grow their loan books through the magic of partnerships.

And now, everyone’s wondering – did we fly too close to the sun?

To the regulators’ credit, the Reserve Bank of India saw it coming. From emphasizing caution in retail lending to taking prohibitive actions to curb this unfettered growth – the central bank was at the forefront of limiting damage which few saw coming.

The hypothesis was simple – most of the customers being served by FinTechs are either new-to-credit or sub-prime and hence, portfolios must be monitored closely. At the same time, easy access to loans could easily throw someone into an over-leveraged situation thus making EMI payments not only unsustainable but potentially impossible.

A new report by Experian suggests that some of this has already started to play out.

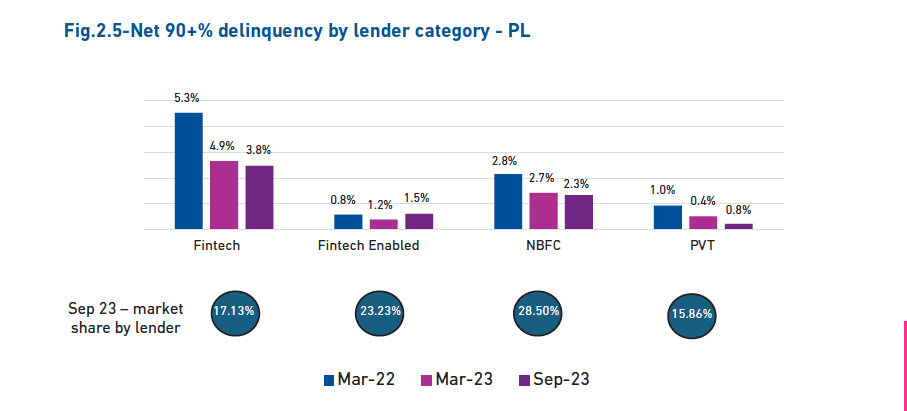

The report underlines how FinTechs have performed the worst on NPAs concerning <1 lakh INR loans.

“While Fintech registered exponential growth there is some stress observed especially in more recent sourcing. There is a need to go for controlled aggression in new sourcing to ensure a sustainable book,” the report states.

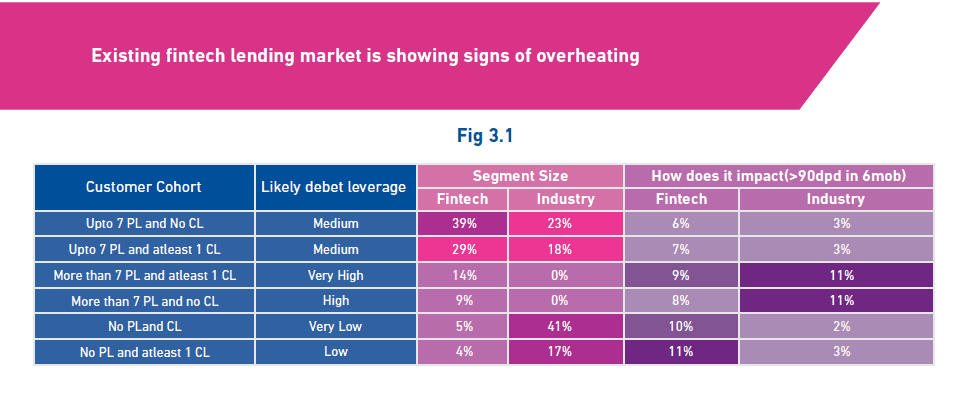

As the above graphic suggests, FinTechs have improved their net 90+ delinquencies but it’s still miles ahead of all other lender cohorts. Another issue with the overheating is over-leverage for which Experian has calculated potential impact on portfolio quality. Again, no surprises as FinTech and FinTech-enabled lenders emerge as the ones most likely to be in harm's way if over-leverage further increases.

This isn’t to say that consumer lending is dead, neither is to pronounce it troublesome. The data just reinforces that the regulators’ worries weren’t unfounded and with the right checks and balances in place – it should be possible to keep the retail lending train on the path without causing it to derail due to excess speed.

This is perhaps what the regulator wanted in the first place, and the first signs are starting to show. The latest bank credit data suggests that the retail lending growth has slowed to 18% in January 24 as compared to 20% y-o-y growth in January’23. This moderation, while new, needs to be sustained even as FinTechs and NBFCs must find a newer oasis for growth now that the unsecured lending well seems to be drying up. Well, for the short term, at least.

That’s all from me this week. I will see you next week.

As always, some data and reading recommendations follow.

Reading list

Slice gets CCI's clearance to merge with North-East Small Finance Bank

Paytm gets third-party app license from NPCI, letting Paytm users access UPI

UPI transaction fee debate resurfaces as PhonePe & Google Pay cash in on Paytm's fall

Between the digits

68% - Customer complaints to the RBI Ombudsman increased by 68% in 2022-2023 compared to the previous year. This is likely on the back of increased awareness and more rampant fraud.

21% - Bad loans in the banking sector fell by more than 21% over the last year to Rs 4.85 lakh crore – a record low.

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources