The Pattern #134

RBI just made these 3 surprising revelations about Indian economy

Mayank Jain

Head - Marketing and Content

·

May 31, 2024

Hello everyone,

Welcome to the 111th edition of The Pattern, a weekly where we dive into the latest from the world of finance, economy and technology. Let’s get started.

This week, the Reserve Bank of India released its magnum opus – a 300+ page dossier of everything that the central bank concerns itself with. And trust me, it’s a lot. A lot.

Let me start with this, if math nerds were to form an organisation – RBI would crush them in its sleep. The regulator loves to keep count. Be it the number of soiled bank notes in the system or even the number of its employees who received emotional intelligence training.

If this isn’t impressive, consider this – the RBI not only knows the currency in circulation (every central bank would know that, duh!) - but it also conducts a dual side survey – consumer and business – to figure out the exact sentiments about the currency situation . It, then, tells us exactly how many consumers want more Rs 5 coins and exactly how many merchants say they’re running short of banknotes in which specific months.

This isn’t a trivialisation of the regulator’s full-time job of keeping the earth spinning on its axis and ensuring that consumers, investors and financial institutions are protected at all times. Rather, this is an expression of one’s shock at seeing just how overachieving a regulator can be if they’ve got the right work ethic.

The 300 pages of the RBI’s annual report aren’t easy to read by any means but dig deep and there’s so much to learn about things you’d generally never stop to consider twice.

Today, let’s look at 5 such revelations and see if these can help us make sense of these crazy, crazy times.

AI (probably) can’t steal Indian jobs

It’s a common theory that more digitalisation leads to more output and hence, obviates the need for commensurate human resources. In other words, technology investments ultimately reduce worker productivity and force organisations to pick computers over people. It’s called Solow’s paradox.

Except, it doesn’t work in India. According to an RBI analysis of various studies, more ICT investment has led to increased worker productivity.

“The contribution of ICT capital services to output growth increased from 5.0 percent during 1981-90 to 13.2 percent during 1992- 2023. The contribution of ICT capital deepening to labour productivity growth increased from 8.4 percent to 15.3 percent over the same period,” the RBI states in its annual report.

Phew. Vanquishing myths and bucking trends – one deep-dive at a time.

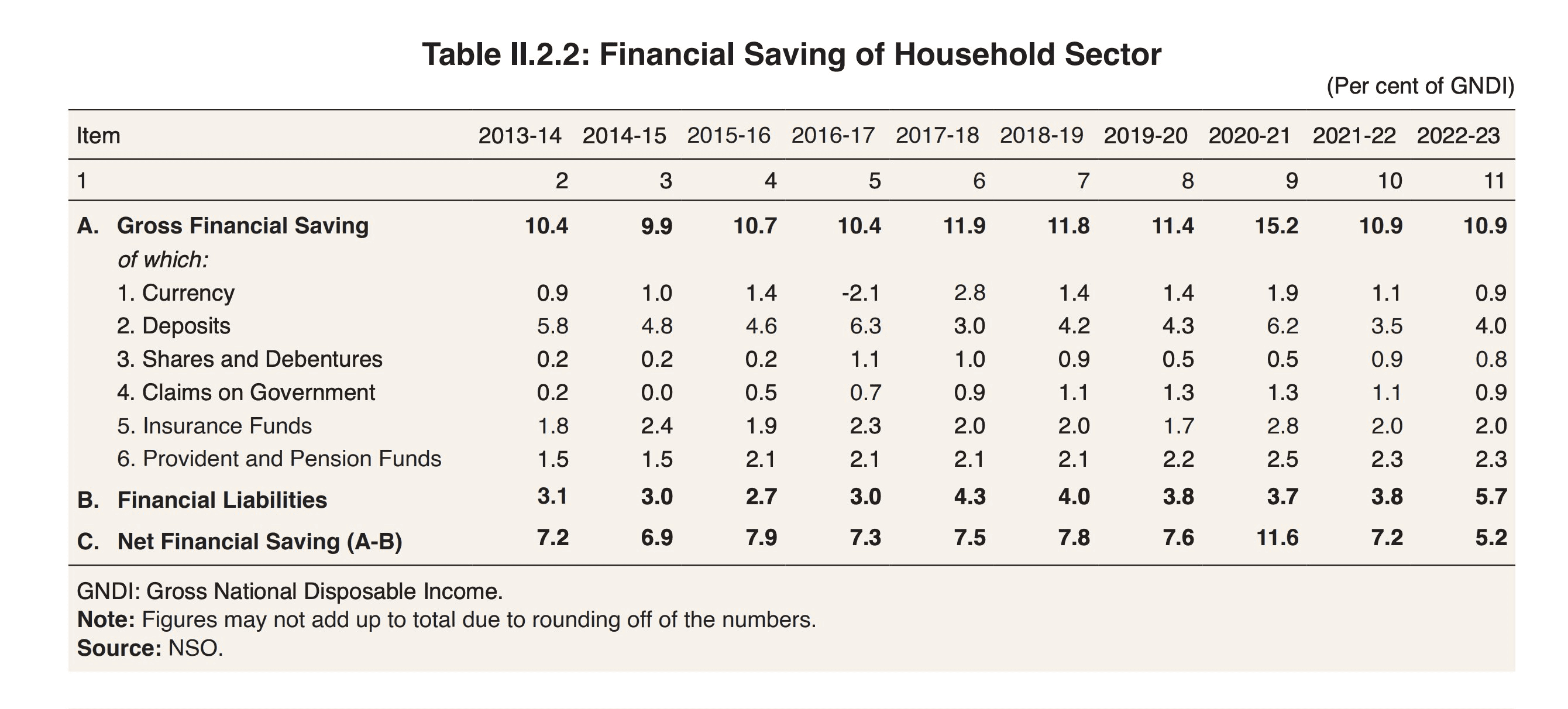

2. Indians are ditching saving and borrowing like there’s no tomorrow

Once commended for their ultra-thrifty financial management, Indian households seem to be embracing the consumerist wave in more ways than one. The latest numbers on household savings show that over the last decade, total financial savings have flattened even as financial liabilities have almost doubled !

This is not a blip on the radar. It’s a gradual shift that has come about due to increased preference for owning cars, homes and other assets among the younger generation. At the same time, increased availability of credit has also made it easier for people to finance these big-ticket purchases – even if it means dipping into their savings pool a bit.

As a result, financial liabilities have jumped from 3.1% in 2014 to 5.7% of the gross national disposable income in 2023. This has led to a decline in net financial savings from 7.2% to 5.2% in the same period.

However, some economists say this isn’t a reason to worry yet. Read here what DK Joshi, Chief Economist at CRISIL told the Economic Times.

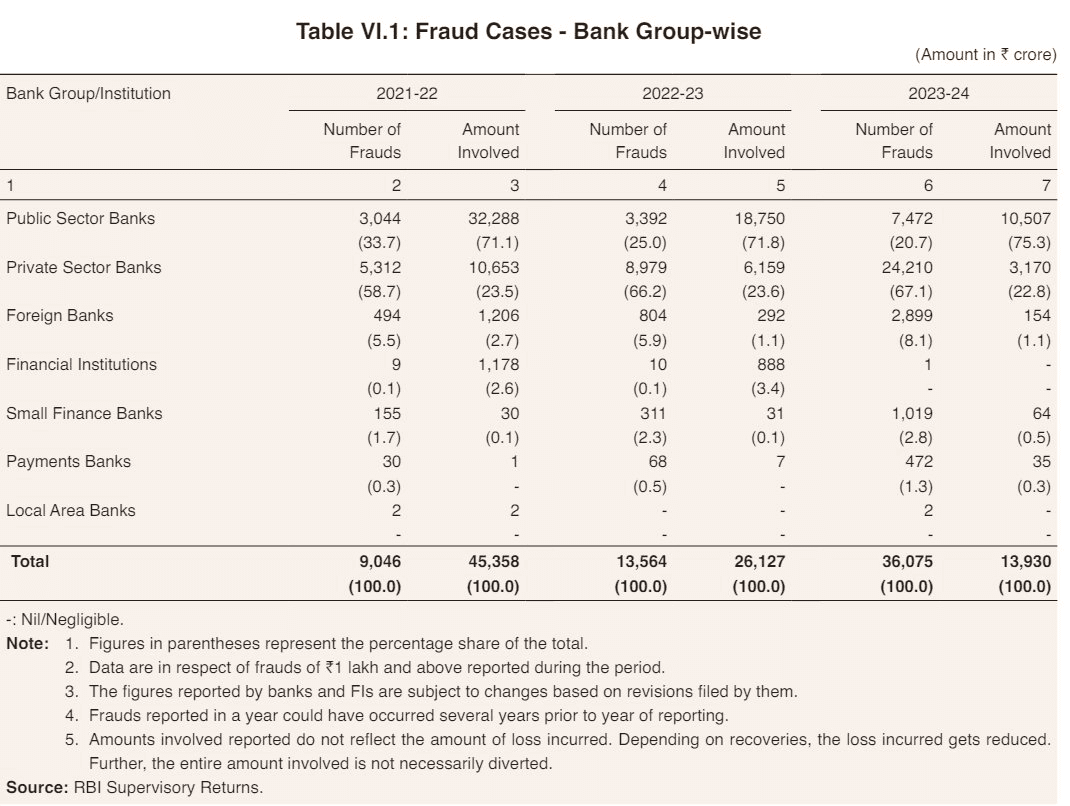

3. Frauds rise, damages fall, reporting lags

Banking fraud has been one of the biggest themes of the season. Though fraud and money go hand-in-hand, the regulator has been working overtime to curb fraud and protect consumers as well as the financial system. The latest data indicates that fraud has risen massively across segments – 36,000 cases were reported last year as compared to 13,000 in the previous year – a 3X rise! However, the money involved almost halved in the same period.

What gives? Observers suggest that it could be due to greater awareness among the public that people smell fishy business and limit their exposures even as fraudsters get more crafty and are seemingly able to cast a net wider with every passing day.

This, however, still overlooks the fact that this is just the reported data and actual quantum of frauds could be even 10x higher than these numbers and it might never make it to formal reports because of the shame, liability and friction associated with this pesky issue.

Interestingly though, people seem to be coming forward to report cases of fraud that happened way back in the past. In fact, more than 90% of fraud cases reported in the last year actually pertain to previous years. This means that only 10% of the reported fraud happened in the same year as it was reported. Crazy.

“An evaluation of bank group-specific fraud cases spanning the past three years reveals that although the private sector reported more frauds, public sector banks consistently accounted for the highest total fraud amount. The majority of fraud cases have occurred within the realm of digital payments (specifically involving cards and internet transactions) both in terms of frequency and monetary value,” wrote Business Standard.

That’s all from me for this week. As always, leaving some reading recommendations below.

Reading list

1. Mukesh Ambani's fintech juggernaut starts rolling: The road ahead

2. Reduce reliance on wholesale deposits to fund loans: RBI to banks

3. RBI Guv Shaktikanta Das launches PRAVAAH, Retail Direct mobile app and FinTech Repository

4. Some Indian ARCs are circumventing rules, says RBI's Swaminathan

5 . Census: Updated demographic data is a must for India

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources