The Pattern #134

The Pattern #129: After sunny heydays, a harsh winter awaits lenders

Mayank Jain

Head - Marketing and Content

·

Oct 18, 2024

Hi everyone,

Welcome to the 129th edition of The Pattern, a weekly where we dive into the latest from the world of finance, economy and technology. Let’s get started.

“The Times They Are-a Changin,” wrote and sung Bob Dylan in 1965. But while his anthem was supposedly to loosely inspire positive change in society, its connotation has tilted axis over the years and now seems to be an aphorism for any profound change in the status quo – be it good or bad.

For India’s financial services sector, however, there’s more bad news than good. Be it the continued difficulties in getting customers to save money in banks or the relentless onslaught of rising credit costs on profitability margins – banks seem to be bracing for a harsh winter which technically coincides with the climate in the country too.

Be it Winterfell or Delhi – winters have always been braved by stocking up on supplies, hibernating till the harsh winds pass and the sun shines again. Banks, unfortunately, don’t have that luxury. They’re going to have to fight battles on many fronts if they’re to see the sunshine on the other side of this cycle.

The wars to come

Let’s start by dissecting the perfect storm brewed by a bunch of difficult conditions that have got lenders worried and their leadership scrambling for answers. First, there’s a situation of excessive liquidity in the system which the RBI is worried about. Excessive liquidity is a problem because too much of it causes inflation. At the same time, time deposits in the form of savings and fixed deposits are nowhere close to desirable levels.

Despite best efforts by banks to raise deposits before the quarter end, the results are marginal and the credit-to-deposit ratio across the system is hovering precipitously near the danger mark.

Axis Bank MD Amitabh Chaudhry said that it’s a tough situation for banks to navigate because on one hand, their costs of funds is rising while interest rates they get for loans aren’t rising in tandem.

"The current conditions present a lot of variables which are tough," he was quoted as saying by The Economic Times. He added:

"While we say we have excess liquidity on the other side the deposit rates are not coming down. There are clear guidelines in place on what credit-to-deposit ratio you can have. We are seeing some worsening of asset quality in some of the unsecured and some other asset classes. The interest rates demanded by good customers are also not increasing. In such an environment to be able to deliver a steady NIM, improve asset quality and take prudent provisions puts us in a different light.”

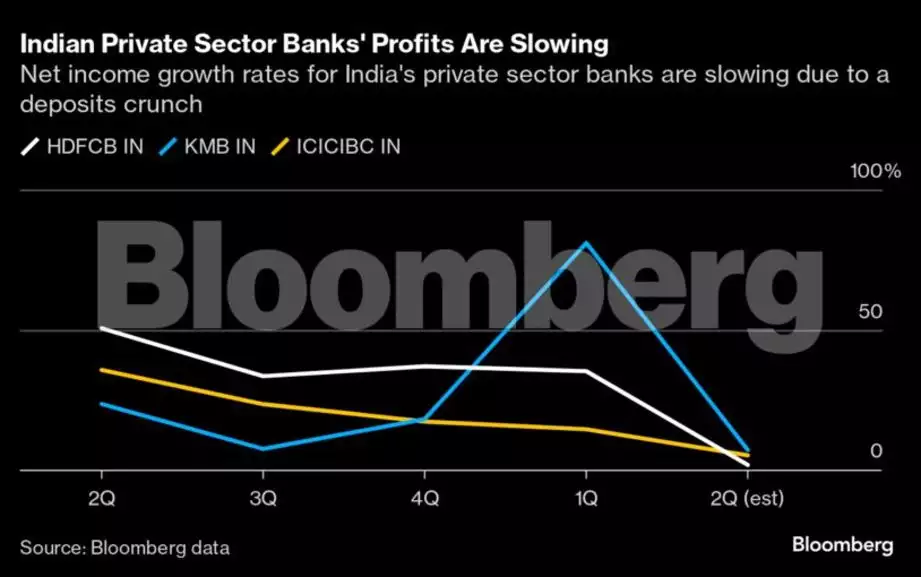

While Axis Bank’s recent results are by no means disappointing – the increase in provisioning for loan write-offs have got analysts and industry watchers worried about the health of the lending portfolios on the retail unsecured side.

“Loan to deposit growth remained muted and credit to deposit ratio continues to remain elevated at 92%,” said Rahul Malani, Equity Research Analyst at Sharekhan by BNP Paribas. “On the asset quality front, although net slippages were lower, write-offs were significantly higher mainly from the unsecured retail segment.”

You win or you die

The perfect storm has been in the making for more than a few quarters now. It all started with the alarm bells raised by the banks and the RBI about the reduced deposits in the banking system which limits the ability of banks to comfortably lend.

This is concerning because credit demand across segments has continued to rise unabated and deposits not keeping pace with it puts lenders in a tough position.

The theory goes that Indians are increasingly choosing mutual funds and equities to park their money rather than coming to the bank branches and depositing money in a savings or a fixed term deposit. This meant that banks have had to slow down loan growth – both considering the lack of deposits and also the RBI’s soft instructions to lower loan-deposit ratios.

As a result, the margins have started to take a hit. Because banks are now financing credit by raising funds from the market at higher rates, their interest margins are squeezed, and the bottom lines of banks are getting affected.

As the system expects a rate-cut in December, things might get worse.

“Markets are also split on a rate cut in December after inflation accelerated at a faster pace than expected last month. With high rates, banks also face high credit costs because of the lag in the repricing of deposits, which will worsen once rate cuts kick in,” a news report said .

Meanwhile, Small Finance Banks aren’t doing much better either. Their profitability measured by Return on Assets (RoA) is expected to reduce a bit this fiscal due to crunched margins and higher costs of capital. It’s expected to reduce to 1.7% from 2.1% last fiscal, according to a report by Crisil.

While large and small banks deal with this thunderstorm, the NBFC sector seems to be caught in a hurricane.

Due to their higher costs of credit, NBFCs usually charge an even higher rate of interest on loans from customers to maintain a healthy profit margin. However, the RBI has come down heavily on offenders when these rates tend to rise above comfortable levels for the borrowers.

In a recent action, the RBI banned four entities – including Navi Finserv, DMI Finance and two others from any fresh lending.

“This action is based on material supervisory concerns observed in the Pricing Policy of these companies in terms of their Weighted Average Lending Rate (WALR) and the Interest Spread charged over their cost of funds, which are found to be excessive and not in adherence with the regulations,” the RBI said in its statement noting that these practices are “usurious”.

While it’s unclear how and when this ban will be lifted, it seems clear that there’s enough and more for lenders across different licenses to be worried about. With a watchful regulator, competitive headwinds and burgeoning stress on portfolios, it’s anybody’s guess when this winter ends. One can only hope that the famed resilience of India’s financial system once again offers protection to its constituents as they brave winds harsher than ever.

"You were born in the long summer. You've never known anything else. But now winter is truly coming. And in the winter, we must protect ourselves, look after one another," Ned teaches his younger daughter in Game of Thrones .

That’s all for this week. As always, leaving some reading recommendations below.

Reading list

Shaktikanta Das asks emerging economies to strengthen risk buffers; warns banks of growing AI use

Indian payments industry likely to grow to $49 trillion in value by 2028: BCG

Can the use of multiple Account Aggregators make customer onboarding smoother?

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources