The Pattern #134

5 trends that will shape the future of credit in 2025

Mayank Jain

Head - Marketing and Content

·

Dec 27, 2024

Hi everyone,

Welcome to the Pattern #137, this year’s last and final edition. We’ve spent more than 2 years now tracking the latest in the world of technology, economy and finance. This is an opportune time to reflect on some of the major tectonic shifts from the year gone by. It’s time to reflect, reassess and realign priorities as credit and FinTech gear for a highly volatile year ahead.

Let’s get started.

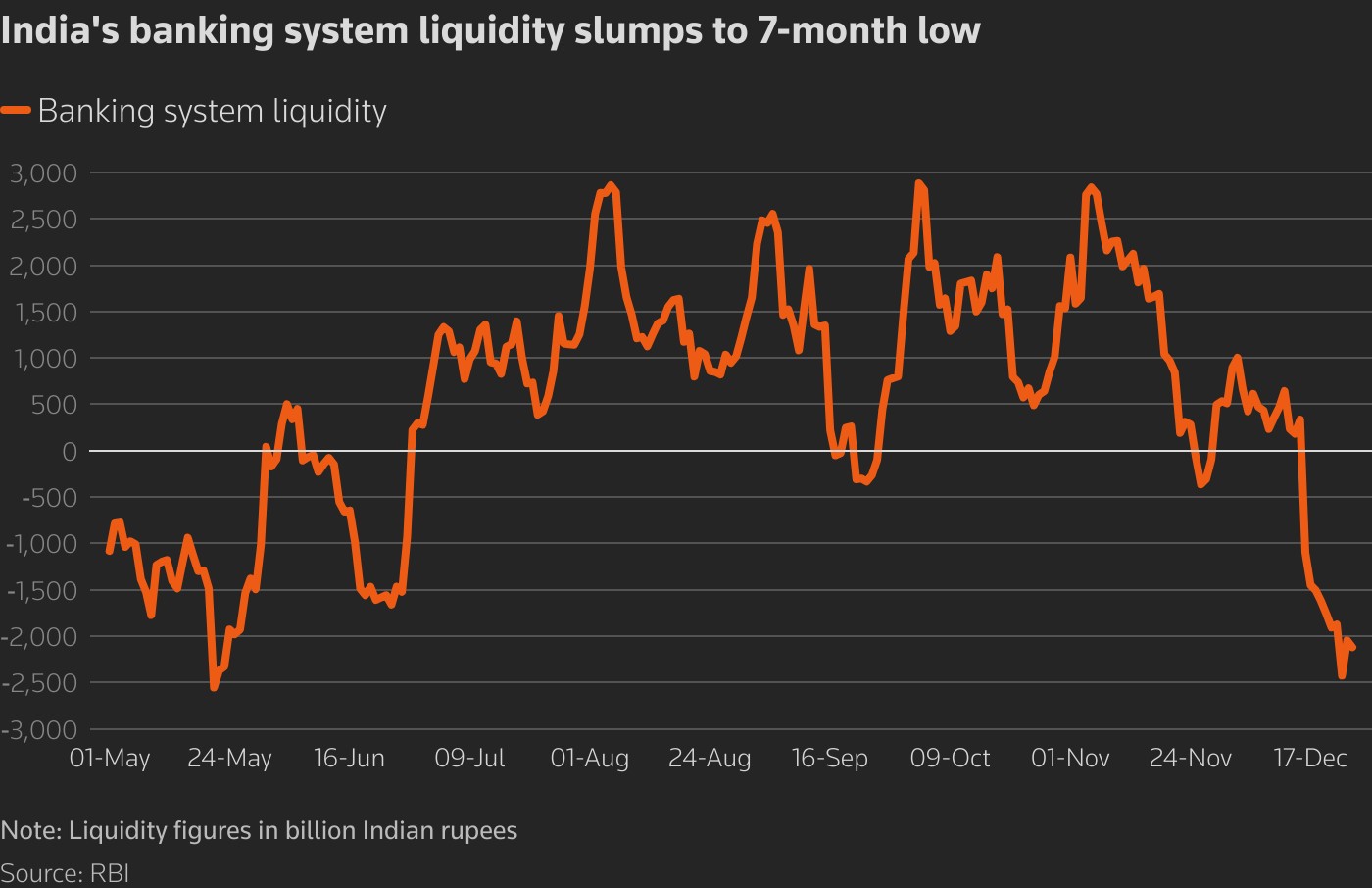

Trend 1: Banks continue to be cash-starved

It’s a rather funny thing to say and write. But Indian banks are running out of cash. Even as the situation makes for good rhetoric, its implications are rather grave. The current liquidity crisis in banks is not borne out of a run on the banks, instead, it’s the manifestation of multiple years of high credit growth while sources of liquidity – including deposits, infusion from the central bank and foreign sources of funds are plateauing – at best.

There are suggestions that the situation might even worsen in the upcoming year . It’s important to note that banks often receive liquidity in the system from three major sources:

Deposits – time and demand deposits

RBI – through lowered reserve cash requirements

Government spending

Now, we’ve chronicled the problem of deposit deficit for a while. It’s something that banks are grappling with and struggling to solve. At the same time, the RBI has done its part by recently lowering the Cash Reserve Ratio (CRR) by 50 basis points. However, government spending has been muted recently.

Add to this, the skyrocketing credit growth and you get a situation where banks can’t do much but twiddle their thumbs and wait for a divine or regulatory intervention to heal. 2025 is set to be less than a cakewalk.

Trend 2: Indian consumers are running low on funds too

While the banking liquidity crunch is somewhat notional and easier to solve with monetary policy interventions, what can one do when most of the consumer class is burdened with debt?

In recent years, unsecured loans such as personal loans and credit cards have seen immense growth. It was once seen as a good sign for the banking system but has now morphed into a bellwether of perhaps stressed budgets and wallets leaving citizens with no resort but to avail expensive credit.

Here’s a data point – credit card outstanding reached 3.3 lakh crore INR in June’24, a 26.5% increase from the previous year. At the same time, late payments are rising across the board! Here, from an Economic Times report capturing the insights from a CRIF study -

“Late payments are rising across all card categories. The percentage of cards with payments overdue between 91 and 180 days increased to 2.3% from 2.2% a year ago. Cards with limits under ₹50,000 showed the highest risk. The percentage of these cards overdue between 31 and 90 days rose from 2.5% in June 2022 to 3.2% in June 2024. For medium-sized card issuers, the percentage of cards overdue by more than 360 days jumped from 1.5% to 3.8% during the same period."

In 2025, banks and FinTechs betting on the lending horses will have to figure out an alternative strategy because the unsecured jock is tired and about to faint mid-race.

Trend 3: Fraud will be as commonplace as there are FinTech apps

There’s no exaggerating this. Banking, credit, and payment fraud has been rampant all of 2024, and the year ahead will likely be no different. If anything, fraud will rise further and will get more complicated to detect as the sophistication of malevolent actors improves.

Data released by the RBI yesterday showed that that fraud cases during April-September period stood at 18,461 cases involving Rs 21,367 crore – this is an eight-fold jump from the comparable period of last financial year.

While internet fraud accounted for 45% of the total amount involved, they constituted 85% of all frauds in numbers reported by the customers. This shows just how scary a place the digital world is becoming for consumers – savvy and naive alike.

In the coming year, we might see a lot more regulatory oversight in this area, but a lot more of the onus will be on banks, FinTechs, and NBFCs to ensure that not only are their systems bullet-proof but that their consumers aren’t interacting with an imposter who’s out for their money and more!

PS: Check out this scary dashboard compiled by a fake-app activist who’s been on a crusade to get fake apps of popular lenders removed from the app stores.

Trend 4: There’s security in secured credit

As lenders look to mitigate the storms of unsecured lending, they’re likely to adopt wholeheartedly the secured lending portfolio. What was once seen as a relatively boring and automatic mode business is now likely to see a lot of action, attention and innovation.

Secured lending is likely to be the theme of the year 2025 and lenders across the board are already gearing up to go full throttle on this segment. Be it loans against property, mutual funds, mortgages or automobile loans – lenders will find it more comforting to lend against an asset rather than just on a consumer’s willingness to consume credit.

This isn’t a deep realization borne out of soul searching but a rather urgent call to action given that unsecured lending is set to be either slowing down or showing stress all year long. Already, banks have seen their retail books rise massively due to increase in home loan disbursements across the country.

As Indian consumers find themselves strapped for cash, lenders might come and offer help – but only when they get to choose what the cash gets spent on!

Trend 5: Compliance will become a success vector

Last but not least, regulatory compliance will become a success vector for financial services firms in the year 2025. This implies that those who keep their books in order, operations in check and function above the rule of law will see asymmetric upside to their business.

This is because the government and the regulator have both come out strongly against any form of non-compliance and the RBI has continuously warned that trying to find loopholes will lead to disciplinary curbs.

In a recently published report, the RBI said that banks must mend ways or be ready to face more curbs. The regulator spoke out against lenders not being mindful of the stress in the unsecured portfolios and said extra vigilance is required.

It said that the regulator expects "boards of regulated entities (RE) to show prudence and avoid exuberance in the interest of their own financial health as also systemic financial stability" and that "delinquency levels and leverage warrant enhanced vigil".

It won’t be surprising then, to see lenders in 2025 investing heavily in fixing their compliance, operations and regulatory issues proactively before they even try to fix anything else.

Spring cleaning time, it is, then.

That’s all for this edition. I will see you next year. Hope you have a very good and prosperous year ahead. Do write back and share your thoughts if you liked this edition or forward it to a friend. No reading recommendations today – watch a holiday movie instead.

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources