The Pattern #134

RBI eases risk weights but can it keep the lending house in order?

Mayank Jain

Head - Marketing and Content

·

Feb 28, 2025

Hi everyone,

Welcome to the 145th edition of The Pattern, a weekly where we dive into the latest from the world of economy, technology and finance. Let’s get started.

There's an ongoing feud within a family, where younger members are at odds, causing tension in the household. The only way to restore harmony is when an elder steps in to take charge of things, ensuring the house runs smoothly. Sounds like the plot of a daily soap opera, right?

Well, this is somewhat the scenario for Indian finance right now. To improve credit flow, increase liquidity, and strengthen growth, the Reserve Bank of India has stepped in like the elder, announcing measures to make it easier for banks to provide micro-loans and lend to non-banking finance companies (NBFCs) and microfinance institutions (MFIs).

The central bank has done this by freeing up capital—essentially lowering the amount of money banks need to set aside against such loans.

Starting April 1, NBFCs will see their loan risk weights return to previous levels while microfinance lenders and borrowers get immediate relief.

This is the second time in a month that the RBI has taken steps to support credit flow. Earlier this February, RBI reduced the repo rate by 25 basis points to 6.25% .

The feud

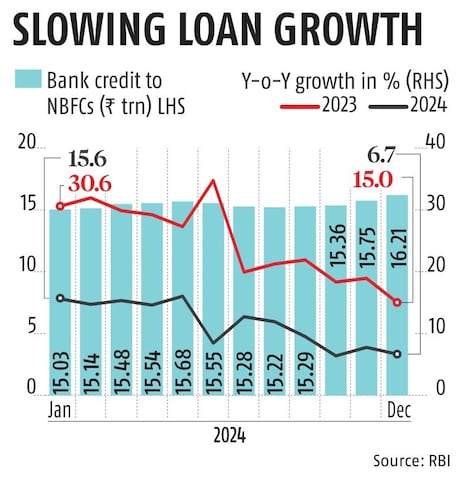

To keep the unsecured lending in check, in November 2023, RBI initially increased the risk weights for banks to NBFCs. The previous increase in risk weights led to a significant decline in bank lending to NBFCs, from 15% to 6.7% year-on-year by December 2024. This slowdown affected the ability of NBFCs to provide credit to retail customers, impacting overall economic growth.

In response, the RBI aimed to improve credit flow to NBFCs and support economic stability by reversing the higher risk weights. RBI had to take this step presumably to bring back the sluggish bank credit growth to NBFCs on track.

“Prior to November 2023, 47% of NBFC borrowing was from banks. That has already declined to 45% over the past year. NBFCs had to explore alternative sources like capital markets and external commercial borrowings (ECBs). At a time when dollar movement has been adverse for ECB hedging costs, alternative funding options for NBFCs were becoming limited,” said Ajit Velonie , senior director of Crisil Ratings.

The solution

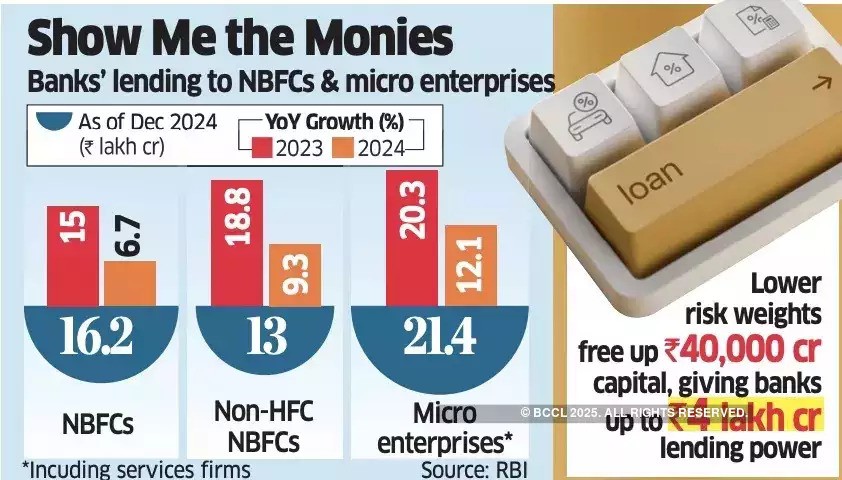

To manage the household or the Indian financial ecosystem, this reduction of risk weights is one of the solutions. It is estimated that about ₹40,000 crore in capital will be freed up due to this move. This roughly translates to banks now being able to lend up to ₹4 lakh crore to higher-credit-worthy, AAA-rated companies.

Not just that, the RBI also reduced the risk weight on bank microloans to 75% , a significant drop from the previous 125% assigned to banks with significant microfinance exposure. However, loans allocated for consumption will remain at 100% risk weight. The RBI also increased the risk weight for consumer credit (excluding housing, education, vehicle loans, and loans secured by gold) to 125%.

Appreciating RBI's decision, YS Chakravarti , managing director at Shriram Finance, said that, "The higher risk weights for over a year hit smaller NBFCs because bank funding became more expensive for them. Larger NBFCs like us had to keep excess liquidity to ensure funding was not a challenge. Now, with lower risk weights, access to funds will improve for the sector."

Sadaf Sayeed , chief executive at Muthoot Microfin, also mentioned that "RBI's temporary measures have worked well, and it is time to focus on prudent growth."

Will this solve the issue?

Even though the head honchos of the microfinance sectors have shown support for RBI's move, it's not hidden that microfinance tends to get over exuberant and that it is also done with razor-thin credit margins throwing caution to the wind. All this to capture mid-sized corporate borrowers. The result? NPAs in the microfinance sector skyrocketed to ₹50,000 crore, reaching a 13% ratio of gross loans at the end of December.

Not just that, the India Meteorological Department issued heatwave warnings for various regions. This is worrisome for lenders, as they will witness a decline in loan collection and an increase in NPA due to a lack of farming income due to a potential drought. These external risks are beyond anyone's control.

While this is undoubtedly a significant step toward financial stability taken by RBI, only time will tell if it brings lasting relief or if the Band-Aid will eventually peel away, exposing deeper cracks.

This is a huge puzzle to solve, and this is just one piece. The RBI has taken several key decisions to support India's financial landscape. To stay updated, I've compiled a reading list for your weekend. Do check out the links to get the full picture.

Reading List:

RBI increases mortgage, loan ceilings for urban co-operative banks

Indian banks to face margin squeeze as RBI may go for more rate cuts

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on X here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources