The Pattern #134

Blunt instrument - Can a ban fix the digital lending industry?

Mayank Jain

Head - Marketing and Content

·

Feb 10, 2023

Hello everyone,

Welcome to the 47th edition of The Pattern, a weekly newsletter where I dissect the rumblings from finance, economy, and technology. Let’s get started.

Bolt from the blue

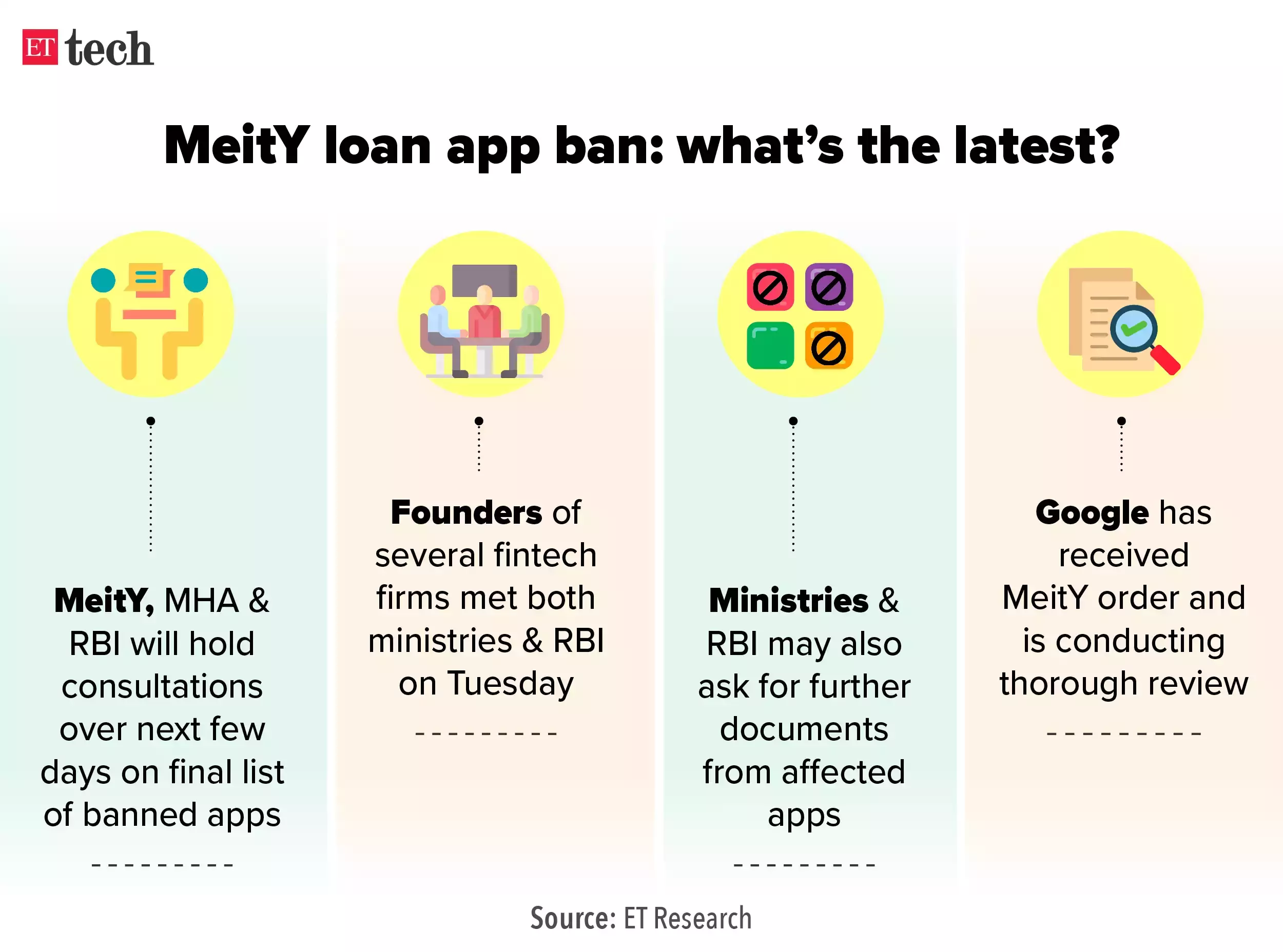

The week’s biggest news story was a sudden ban on several digital lending apps by the orders from the Government of India. On Monday, 138 betting apps and 94 loan apps were banned by the Ministry of Electronics and Information Technology. The banned apps reportedly include certain big names such as LazyPay, Kissht, Indiabulls Home Loans, and Quik Finance, among others.

Here’s the problem - the order isn’t public, nor is the reason behind the ban.

What makes it worse is that even the affected companies haven’t received any order/intimation from the government and the respective app stores.

While many companies have stopped user onboarding, users are complaining online about not being able to access the apps or finish transactions in apps still on the Google Play Store.

As a result, the entire FinTech industry and startups are scrambling to double-check if their names are on the lists or if there’s a likelihood of them getting affected through a future action.

This is oddly reminiscent of the crackdown of 2020 when the government banned certain Chinese companies from Indian markets in one fell swoop. The biggest names included TikTok and PUBG.

This isn’t to say the ban is unfair or unjustified but to point out that many blunt instruments like banning don’t often work the way most policymakers assume they will.

For instance, the continued haze around the reasons for this ban means that lending companies don’t know what they did wrong. A quick scan of various media reports and unnamed quotes from government officials reveals that potential reasons for action could well run into dozens, if not more.

Let’s take a look at some of the possibilities:

Chinese links - either in ownership or funding or routing money

Usurious interest rates - very high-interest rates that lead to debt traps

Collections malpractice - threatening, harassing, and shaming delinquent borrowers

Data security - fears of data being sold, transferred, or leaked to mala fide entities

User complaints - action for apps not servicing users properly or harassing them in any form

RBI whitelist - apps not on the RBI’s whitelist could be banned as they can be deemed illegal

Shell companies - certain lending operations recently were found to be run through shell companies

Authorisation - many apps may operate in a regulatory grey area without RBI’s direct supervision

Licence muling - apps using/renting licences of dormant NBFCs to run lending operations

And more…

Bad weather and hazy skies

Even if one acknowledges the very real problem of illegal lending apps and malpractices in the sector, the current framework of regulation and corrective/coercive measures raises certain questions.

Once a blanket ban order is issued on a bunch of entities, the entire sector is threatened. It may or may not be intended but the result is chaos and deep-rooted fears in the minds of both promoters and investors of even bona fide companies about the long-term stability and future of the industry.

This is echoed by many industry organisations and experts who see the move as a catalyst for more confusion and chaos in an already gloomy business environment.

"Policy decisions like these have a direct impact on the ease of doing business in India," Vivek Iyer, national leader of the financial services risk advisory division at Grant Thornton Bharat, told BQ Prime. "Given that there is a significant amount of investments made in digital lending companies in India, decisions such as these can prove to be big negatives for the investment climate," he added.

Second, the problem of illegal lending and loan-sharking is much larger than just Google and Apple’s marketplaces.

There are dozens of third-party app stores that list hundreds more lending apps that have either been thrown off the Google or Apple ecosystems or have not been listed there. This means that while some users will be saved from ever accessing the apps, the malpractice continues largely unabated as fraudsters find newer avenues to host and distribute these apps.

Third, there’s also an adverse incentives problem. The companies that complied with the government, the RBI, and Google’s policies to list themselves as bona fide businesses (assuming they’re not in contravention of any laws whatsoever) are facing the maximum heat while much of the unregulated loan-shark industry continues to thrive. It’s not a whataboutery argument but one that calls for a more nuanced and measured discourse around any business activity considering that digitalization only increases compliance - rather than decrease it.

Fourth, there’s a larger digital rights issue that other startups and companies in other industries might have to grapple with as well. Actions such as these bans without public consultations etc. become dangerous precedents and can lead to even more disruption in other businesses/industries without little public scrutiny or pressure on the policymakers to clarify their stance.

“But the issue is the opaque manner in which the subject is being addressed,” Prateek Waghre, Policy Director at Internet Freedom Foundation, told The Print. “We are still not 100 percent sure which apps have been banned and why. This is part of a continuing trend. Hence, it is important that the Indian companies also look at the digital rights issues. Even if these don’t impact them now, they may in the future. The way this issue has been dealt with, the Indian fintech companies are facing the brunt of a lack of due-process.”

Final word

As we wait to see which companies/apps get themselves a lease of life by consulting with the government - it’s pretty much a given that more such moves might follow in the near future.

Hence, it’s imperative for not just FinTech founders but all digital businesses to evaluate their overall compliance to the last grain and invest in continually updating their regulatory readings to be a step ahead of the curve.

As for digital lenders - the message is clear - find your way to that whitelist and comply with all the possible regulations - before it’s sprung upon you in a circular somewhere.

Between the digits

3.8 million - Subscribers Disney+ Hotstar lost in the quarter that ended December 31, 2022. This is one of the big declines in the companies’ subscriber base and is reportedly a result of losing the IPL streaming rights to Reliance’s Viacom 18.

INR 18,216 crore - Money owed by various government departments to MSMEs across the country. This is a fraction of the actual amount as most MSMEs don’t log their pending cases online, and the finance minister did announce a budgetary measure to expedite payments. Let’s hope it works.

USD 164 billion - Norway’s sovereign wealth fund lost a record USD 164 billion last year. One of the world’s biggest investors - the fund returned -14% last year. The USD1.3 trillion fund cited a ‘very unusual’ year for its dismal performance. The fund recently announced it had sold all its holdings in Adani companies - worth around USD 200 million at the end of last year.

With that, I will wrap up this edition. As always, leaving some reading recommendations below.

Reading list

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources