The Pattern #134

FinTrifecta - Analogue rollback, digital push & a regulator to watch over

Mayank Jain

Head - Marketing and Content

·

Mar 3, 2023

Hello everyone,

Welcome to The Pattern, a weekly newsletter where I bring you the latest from the worlds of finance, economy, and technology.

I’m celebrating a personal milestone today. For exactly 50 weeks now, writing this newsletter has been a Friday ritual before I can start unwinding over my two-day weekend - a privilege not everyone in the financial services space gets to enjoy. (I’m watching you, bank employees).

5-day work week on the cards?

The Indian Banks Association (IBA) is in conversation with the United Forum of Bank Unions (UFBU) about a five-day work week. The proposal, which advocates for Saturdays and Sundays off for bank employees, also makes the case for longer shifts (10-hour work day) from Monday to Friday.

There is no final word on the development yet, since the IBA is also conferring with the government. Perhaps bank employees still have a long battle ahead – they’ve been demanding this since the 10th Bipartite Settlement signed in 2015.

It has to be a tough decision for banks. Banking operations are already riddled with red tape and have infamously long holiday calendars every year.

If you ask me, the unions will prevail in their demand for a shorter work week. Simply because it’s not an isolated demand - it’s a reflection of the mood of the banking sector. The sleeping giants of traditional banking are waking up to the potential of digitization rolling back the expansion of their physical resources.

Our CEO Rajat has been documenting this trend for a while now. For instance, banks are no longer expanding their bank branches. There is also a skewed ratio of officers and clerks. Here’s how he put it:

“Given the rapid digitisation in the industry, a need to bulk up executive-level positions has arisen. There is an exodus to administrative offices from modest bank branches as customer-facing jobs are slowly replaced with technology solutions.”

Perhaps bank branches and employees will no longer remain a benchmark for financial penetration - as digitisation takes over.

Sachetisation ftw

Personal loans make up 96% of all FinTech lending, and most of these had a ticket size lower than Rs 5,000, a report by Equifax and FinTech industry body Fintech Association for Consumer Empowerment (FACE) showed. It also concluded that the consumer segment that took loans between Rs 10,000 and Rs 50,000 saw the highest growth last year.

Remarking on the findings, Sugandh Saxena, CEO of FACE said, “Data from the report validates the fintech lending role in distributing ‘sachet loans’ to the mass market and bringing them to the formal credit fold, expanding their credit footprint."

Sachetisation of credit has triggered a mini-revolution in microcredit. Microcredit in India has failed, despite being hailed as the harbinger of financial empowerment. The main reason has been an inadequate delivery framework for microcredit in India.

And FinTechs are bridging this gap. Compared to banks which stand the risk of upending their unit economics by offering small-ticket loans, FinTechs are equipped to lend through alternative delivery channels like BNPL and P2P lending, while also scaling and customising them.

“There has to be a governance layer if…

…you’re in financial services,” Dilip Asbe, the CEO of the National Payments Corporation of India (NPCI) has said. Technically, there is no need for FinTechs to operate in grey areas since the establishment of platforms like UPI and OCEN , he explained, and I concur.

We’ve been watching FinTech regulation closely here at FinBox, and we’re hopeful about the shape it’s taking, albeit slowly. Over the past year, we’ve seen the RBI and other authorities make some decisions that may have been tough on players in the space. But in the long run, the clarity brought about by these guardrails will help establish a vivacious and innovative space dedicated to serving its customers securely.

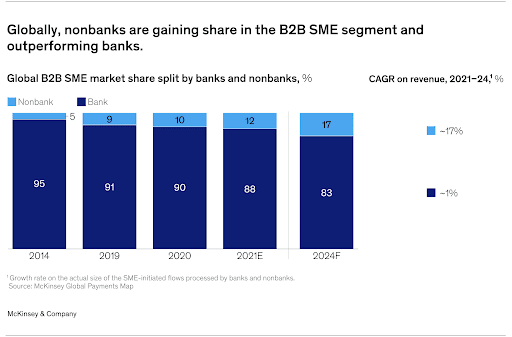

Cross-border payments are becoming FinTech turf

According to a recent McKinsey report , FinTechs have overtaken banks in the race for domination of cross-border payments in Asia. In spite of challenges in fundraising over the past year, players like Payoneer and Wise reported a 30% year-on-year growth in revenue in Q3 2022. Globally, in the B2B and SME segments, nonbanks providing cross-border payment solutions saw a growth of 12% in 2021 compared to only 5% in 2014. They are expected to hold 17% of the total global market by next year.

FinTechs have been able to gain an increased market share through better pricing, greater convenience, faster execution, providing a larger number of products and services as well as third-party integrations. As a result, there is an increased pressure on incumbent banks to recapture market share by leveraging their extensive network of branches and correspondents, expanding the range of products offered, access to forex and liquidity and compliance infrastructure.

Between the digits

$175 billion: What Tesla plans to invest to cement itself as the world’s most valuable car company.

$700 million : The cost of Foxconn’s planned iPhone manufacturing plant in Bengaluru.

Rs 3.06 crore: What the RBI fined Amazon for non-compliance with PPI norms.

Chew on this!

As usual, I’d like to leave you with a few reading recommendations -

What does it take to disburse a Rs 20 crore loan digitally?

How Asian banks can regain the cross-border payments crown

Narayana Murthy is right about start-up valuations

Uncle Sam is disrupting the venture capital world

How Digital technologies and FinTech impact India’s financial landscape

Millennials are on a borrowing binge

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources