The Pattern #134

Will UPI finally get the credit this time around?

Mayank Jain

Head - Marketing and Content

·

Apr 14, 2023

Hello everyone,

Welcome to the 56th edition of The Pattern, a weekly newsletter where we bring you the latest from the worlds of finance, banking, economy, and technology. Let’s dive right into what happened this week!

RBI announces credit lines on UPI

The Reserve Bank of India (RBI) last week announced that customers using UPI for payments can now access credit lines sanctioned by their banks to transact on theplatform.

This isn’t the first time there has been talk of offering credit through UPI. Just last June, it was announced that credit cards could be loaded on UPI, with RuPay integrations leading the charge (UPI and RuPay share the same parent body - theNPCI). Our CEO Rajat Deshpande had written an incisive piece on therepercussions of such a move for several stakeholders in the credit card ecosystem - merchants, credit card companies, and banks. I highly recommend that you read it –

Will linking credit cards break UPI?

The NPCI’s previous experiments have shown that there is some trepidation about the uptake of credit through UPI. For now, RuPay is the only credit card provider offering this functionality on the payments interface. Moreover, as per the RuPay website, only four banks are live with this functionality - Punjab National Bank, Union Bank of India, Indian Bank, and HDFC Bank. Even among UPI apps, only BHIM, Mobikwik, and Paytm are offering credit cards on UPI.

Even as early as 2018, a credit facility akin to overdraft on UPI was announced. However, it failed because merchants were required to pay some charges to use it – an unpopular idea for a platform that typically does not levy any costs.

The question now is – if previous attempts at offering credit through UPI have been slow to gain traction, what can we expect from the new move?

First, this is a little different from UPI’s previous attempts to load credit cards on thepayment rail. Users need not have a credit card to tap into this pre-approved credit line. This could potentially make access to institutional credit more widespread, given UPI’s popularity among Indian users.

Second, the lack of a merchant discount rate (MDR) that is typically levied by credit card companies could prompt merchants to accept credit payments more readily through UPI as opposed to incumbents.

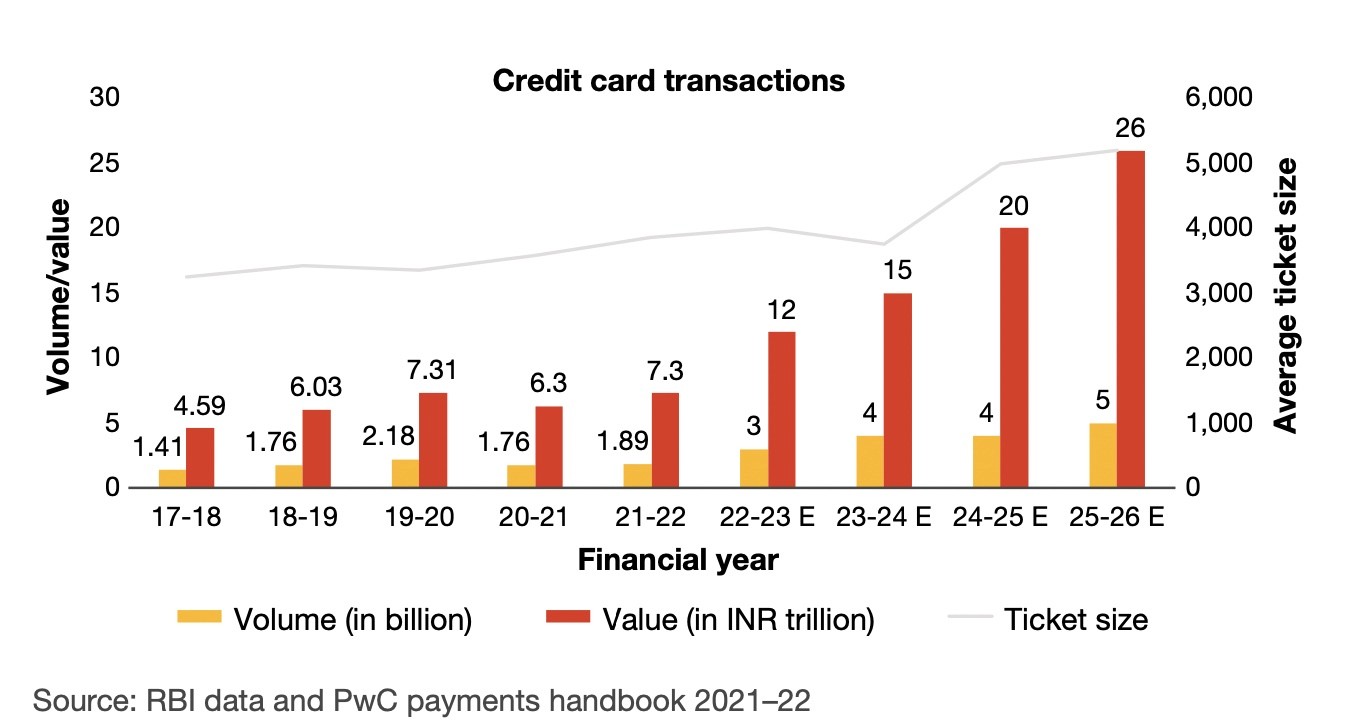

However, if the limit on such credit lines is capped low, it might be hard for UPI to make a dent into credit cards’ market share. Because credit cards are typically used for transactions amounting to ~Rs 4,000, smaller credit limits on UPI may not appeal to users.

Another major reason why customers use credit cards is the rewards and features that they offer - something that will be missing from the UPI credit line functionality.

But these are just my two cents based on the initial announcement. Let’s wait and see what plans the RBI has for credit lines on UPI!

Interest can no longer be used in a punitive way

The RBI issued a draft circular this week barring lenders from using interest as apenal tool to tackle borrower default and non-compliance. It observed that penal interests were being used by lenders to make up for revenue lost in cases of default.

Two things of import stood out in the circular –

Determination of interest rates on credit facilities, including conditions for reset of interest rates, will be strictly governed by the relevant regulatory instructions issued in this regard. REs shall not introduce any additional component to rate of interest.

Penalty, if charged, for default / non-compliance of material terms and conditions of loan contract by the borrower shall be treated as ‘penal charges’ and shall not be levied in the form of ‘penal interest’ that is added to the rate of interest charged on the advances. There shall be no capitalisation of penal charges, i.e, no further interest computed on such charges. However, this will not affect the normal procedures for compounding of interest in the loan account.

It also reminded lenders that the interest component must include a credit risk premium that appropriately reflects the borrower’s risk profile, and can be changed if the risk profile also changes.

Lack of fairness in lending practices such as this remains yet to be addressed, so this is a welcome step in the right direction. While it is critical that lenders protect their loan books - for their own sake, and that of the economy as a whole - there are far better ways to ensure this than resorting to measures like punitive pricing, and worse .

The first step would be to introduce the same level of consideration and personalisation to collections as is afforded to onboarding. If dealt with properly, collections present an opportunity to build quality customer relationships. We wrote a helpful e-book on the subject that you can find here .

The bottomline is this - the entire lending lifecycle, from product development to themanner of debt recovery, needs to be viewed as a business of human relationships. My colleague Shamolie put together an excellent series on humanising FinTech. Here’s Part 1 to get you started:

Humanizing FinTech #1: The case for empathy in FinTech and how to bake it in your products

FinTech funding recovers

There was some other good news this week - the FinTech segment recovered from last year’s funding setback. Tracxn reported that FinTechs drew investments worth $1.2 billion in Q1 of 2023, a 126% rise from the $523 million in Q4 last year.

Funding prospects that cratered last year seem to be bouncing back, thanks to deep internet penetration, and the government incentivising a cashless economy. It’s also imperative to note that FinTech players themselves are building more resilient offerings, partly due to increasing regulatory scrutiny and in part because investors are prioritising profitability over all else. Between the digits

INR 1,000 cr + : Value of overall monthly digital payment transactions each month during the past three months

USD 538 billion: The amount investors have moved into cash funds over the past eight weeks in the fallout of the SVB collapse

10-12% : India Inc’s expected topline growth in Q4FY23

USD 122 billion: India’s overall trade deficit in FY22-23

INR 25,000 crore: Co-lending assets rise 4x in FY23 from INR 5,000 crore in FY22

Reading list

Have FinTechs come down with a case of 'over-specialisation’?

ChatGPT is knock knock knockin' on the music industry's doors

A journey to Dalal Street: the story of one of the oldest private sector banks

In controlled digital lending, the issue of public interest

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues.

Cheers,

Mayank

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources