The Pattern #134

India’s most profitable FinTech operation is hiding in plain sight

Mayank Jain

Head - Marketing and Content

·

May 5, 2023

Hello everyone,

Welcome to the 58th edition of The Pattern, a weekly newsletter where we unpack the rumblings from the worlds of finance, technology and the economy. This week, we’ll uncover the best kept secret in India’s fintech industry and dive deep into just how many ways one can make money (a lot of it) in a sector that’s usually criticised for being a cash-burning machine.

We need to talk about NPCI

The name is familiar. Most people associate the National Payments Corporation of India with UPI. The revolution in digital payments brought about by UPI is often credited to the NPCI and its efforts in building a world-class infrastructure and a real-time settlement product that’s now the envy of the world.

But, NPCI is bigger than UPI. Way bigger.

The organisation is a not-for-profit promoted by the RBI and is owned by a consortium of major banks in the country. It’s actually older than most of the FinTech startups in the country - started in 2008, the payments giant is now maturing towards adulthood at 15 years of age.

The payments system operator was created with the aim of building robust infrastructure for retail payments. And less than 2 decades in, the company has not only turned around magical infrastructural wins but also a hefty sum of cash that could be the envy of just about any FinTech company in the country.

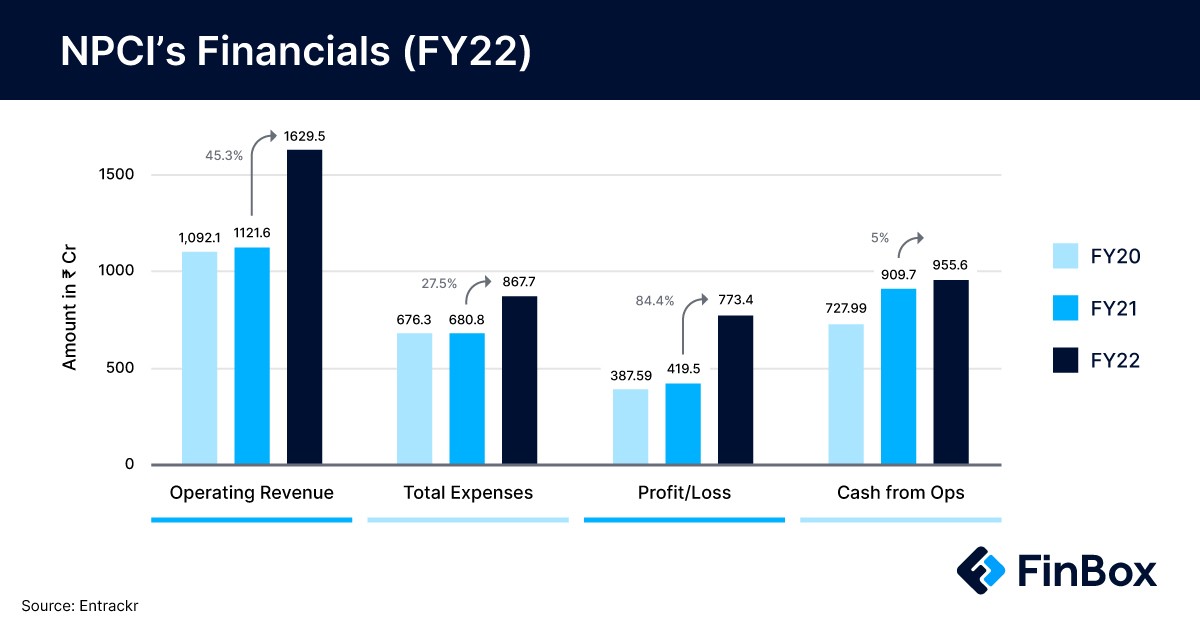

Let’s look at the wad of cash first. According to a very insightful Entrackr analysis , the NPCI made Rs 773 crore in profit in FY22. If you think about it, there aren’t very many FinTech companies in the country that can boast of a profit figure anywhere close to this number (except the notable Zerodha) - forget beating what was once a tiny experiment lab for the RBI and banks to build new cool™ things.

The fun part about the NPCI is that it’s as much behind the scenes about mostly everything else it does as it is front-and-centre about UPI (and now RuPay). This allows this payment systems operator to not just innovate in peace but also continue to build and ship infrastructure that…just works.

We know about UPI. We know about RuPay cards. We know about the marriage of the two in what is called ‘credit on UPI’ - planned, organised and officiated by none other than the NPCI.

But, the NPCI also runs FASTag - a money spinner network as toll plazas in India get digitised and automobiles compulsorily ship with a pre-installed tag that works on the prepaid instrument rails.

This is the fancy stuff. It’s the less shiny places where NPCI is sitting on a gold mine. It runs the Aadhaar-enabled Payments System (AePS). It also runs - National Financial Switch (the ATM network of the country), Cheque Truncation System, NACH, IMPS, and e-RUPI - one could go on.

Practically speaking, NPCI oversees, runs and manages more transactions than perhaps any other entity in the world.

So where’s the money?

The organisation makes a bulk of its revenue from payment services - it forms 96% of its operating revenue and grew 46% in the last year to Rs 1,557 crore in FY22.

This is supplemented by certification income that adds another Rs 10 crore to the top line with network income contributing Rs 17 crore and another Rs 34 crore from other things like compliance and membership fees, hologram charges and international alliances, etc.

All in all, that’s a revenue of Rs 1,629.5 crore with total expenses of about Rs 867 crore and a nice profit of Rs 773.4 crore.

Why is this important?

NPCI’s financials are important for two reasons. One, it’s perhaps a glowing commendation for Indian regulators and policymakers who envisaged this organisation that not only delivered innovation but also is self-sustaining and profitable to boot.

Second - and the more important reason - is that the NPCI is the mother lode of India’s FinTech story. It sits at the centre of the ecosystem and its moves could dictate winners and losers in this hunger game for a long time to come.

Just think of its move to limit market share for UPI apps. Or its recent bid for linking credit cards on UPI - but limited to only RuPay cards. Or the government’s mandate for using FASTag that made certain payment banks a fortune while effectively killing a bunch of startups who were innovating in this space through their own solutions.

The bottom line is that the more NPCI makes, the less it leaves for other intermediaries in the financial sector to eke out. It’s not a zero sum game in the long run but in the long run, as Keynes put it, we’re all dead anyway.

What NPCI has done is commendable and that’s not up for debate. But, what happens when policymakers and regulators not only act as venture capitalists for certain technologies but also birth quasi-regulatory entities that threaten to morph into competitive giants in the same industries that they are tasked with running and managing?

Chaos.

For now, it’s appropriate to congratulate NPCI for making the dream happen. And opportune for the rest of us to learn from the NPCI how to break long standing monopolies, create scalable infrastructure, drive adoption and make money out of public welfare - without ruffling a single feather.

This is all from me today. As always, leaving some interesting data points and reading recommendations below.

Between the digits

Rs 1.24 lakh crore - The difference between loans to industry and retail lending observed in December 2022. This is the lowest gap in recorded history and has sparked concerns on the sustainability of consumption and retail credit when trade credit isn’t increasing.

40%-50% CAGR - Merchant payments are expected to grow by up to 50% CAGR on UPI, according to Bain that expects the total transaction volume for merchants on UPI to touch $1 trillion by 2026 .

5% - Credit card penetration in India as estimated by the World Bank. In comparison, countries like Israel and Canada have more than 80% of their population possessing a credit card.

Reading list

Visa launches CVV-free payments for tokenised credit, debit cards

RBI to step up regulations around FinTechs, Digital products: Governor Das

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources