The Pattern #134

Will Aadhaar’s trembling bring down the FinTech tower?

Mayank Jain

Head - Marketing and Content

·

Jun 2, 2023

The Pattern #62: Will Aadhaar’s trembling bring down the FinTech tower?

Hello everyone,

Welcome to the 62nd edition of The Pattern, a weekly newsletter where I break down the latest from the world of finance, technology, and the economy. Let’s get started.

We need to talk about Aadhaar

Aadhaar is the world’s largest citizen identification project. With more than a billion enrollments and counting, Aadhaar is also the largest database of citizen information including biometrics. These biometric identifiers also help run a payments system which helps millions of people access subsidies, transfers, and social security from the government by showing their Aadhaar cards and verifying their identity through the biometrics.

But, there’s a big problem.

For all its touted benefits in plugging leakage in subsidy transfers, the system is prone to frauds that are getting more innovative by the day.

Lending: In Noida, a gang was held for helping defaulters getting loans from banks by forging new Aadhaar cards and PAN numbers. These defaulters are usually folks whose credit scores dip and they enter a defaulters’ blacklist. But, the gang used people’s toe-prints (as opposed to fingerprints) to help them get brand new Aadhaar cards and secure loans from banks. The amount ran into crores of rupees, apparently.

Payments: It’s not just fake accounts, fraudsters around the country have been using various methods including silicon thumbs to impersonate unsuspecting citizens and siphon money off their accounts using the AePS rails. In fact, it’s gotten so bad that banks have started putting additional guardrails on AePS transactions - such that about 85% of transactions are now failing.

The failure rates are high across various major banks and hence, participants in the ecosystem are worried that it’ll become a continued problem with transfers of subsidy.

“We are talking about poor consumers, some even below the poverty line, many of them do not own a mobile phone let alone getting them seeded with their bank account. They are facing major issues withdrawing funds through customer service points,” said one of the people quoted by the Economic Times, a banker with a private sector bank.

The total damage? Funds up to Rs 2 lakh crore are lying unclaimed and languishing in the banking system across the country.

“In fact, Aadhaar-linked accounts are especially vulnerable to fraud. If your bank account is linked with Aadhaar, and you are not careful, scamsters can easily extract money from it. Even if they lack the simple skill of cloning fingerprints, they can persuade you to put your finger in a biometric ATM under some pretext. This has happened on a large scale in the last few years. Indeed, it is one of the top fraud types listed by the National Payment Corporation of India in its updated ‘Fraud Liability Guidelines’ for Aadhaar-enabled payments,” wrote development economist John Dreze in a recent column in TOI.

Therein lies the rub - if the AePS remains as vulnerable as it is today, it might pose problems for the digitisation story in the financial sector. For starters, Aadhaar is the basis for onboarding new customers across lending, savings, mutual funds and even insurance.

With the rise in failure rates as well as worries about frauds - lenders as well as other FinTechs could be left in the lurch waiting for a solution that can enable as seamless an onboarding as Aadhaar does (or did, once upon a time).

What’s the way out?

Frankly, the story of Aadhaar and India Stack has been one of building the airplane while flying it.

The UIDAI, to its credit, has been quick to issue fixes - however patchy - whenever serious bugs arise in the Aadhaar ecosystem. We’ve seen this many times in the past - the virtual ID, offline verification, QR codes, and biometric locking were all attempts to curb the fatal flaws that showed up in the edifice of digital infrastructure built with the blood, sweat and tears of many a public policy professionals.

One hopes that the serious fraud risks with Aadhaar based solutions are mitigated at the earliest so that FinTech doesn’t have to kill yet another one of its darlings.

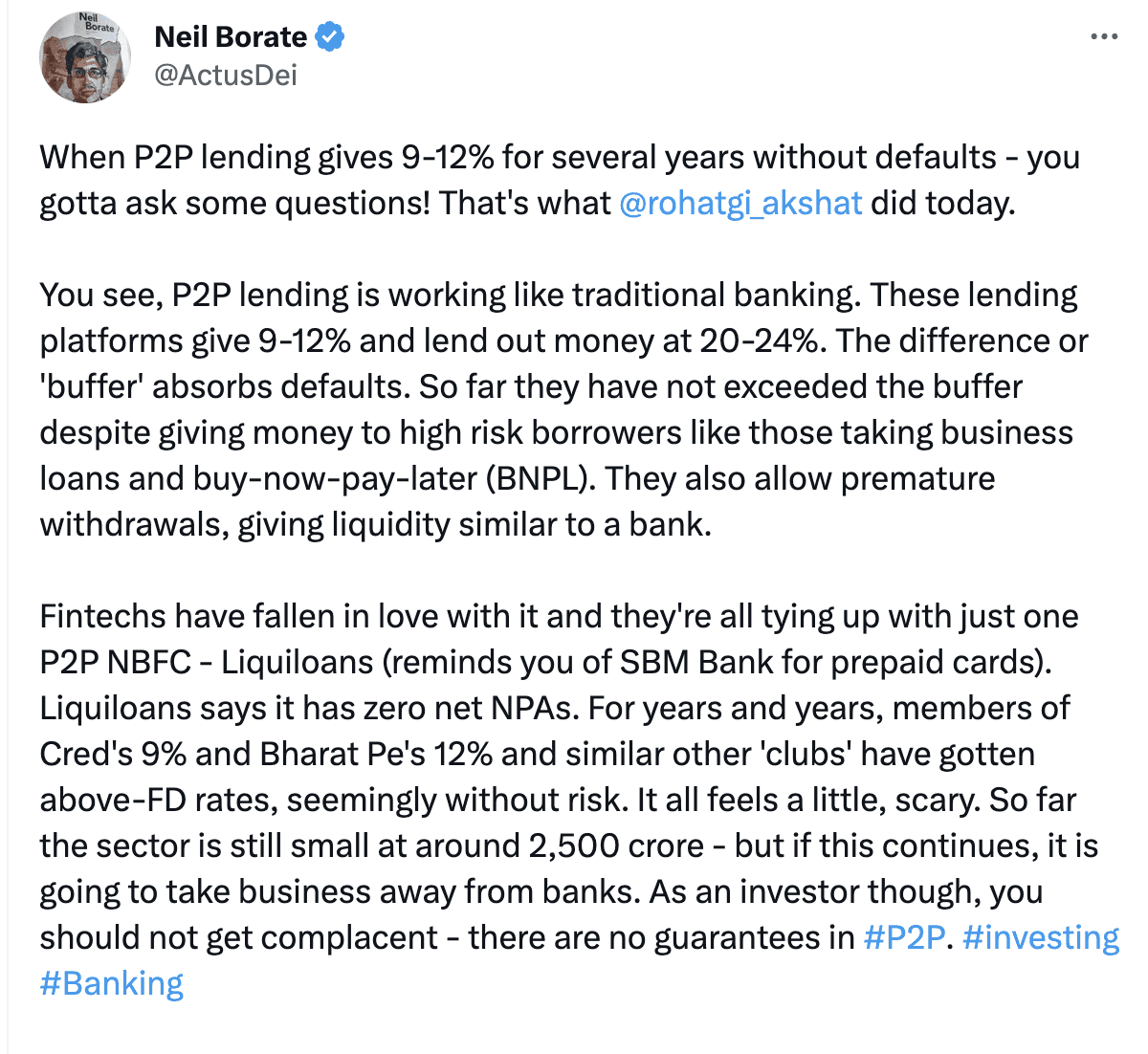

The story of Indian P2P lending - courtesy LiveMint

That’s all from me today. As always, leaving some reading recommendations and interesting data points below.

Between the digits

400- HDFC Bank’s dedicated workforce in its Enterprise Factory division in Bangalore that works solely on digital transformation projects.

9.6%- Reported NPAs for Faircent’s P2P lending operations. The rest of the industry seems to be doing way better, according to self-reported numbers.

10.2% - Credit card and personal loans exposure for scheduled commercial banks against their total loan book.

Reading list

FLDG guidelines expected in second round of digital lending regulations

RBI governor’s speech on ‘innovative accounting practices’ at banks to hide bad loans

Watch out for rising risk appetites among Indian banks, says Fitch

Account aggregator transactions soar as lenders disburse Rs 6K cr

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources