The Pattern #134

Boom goes the lending dynamite!

Mayank Jain

Head - Marketing and Content

·

Nov 17, 2023

Hello everyone,

Welcome to the 86th edition of The Pattern, a weekly newsletter where we delve into the latest from finance, economy, and technology. Let’s get started.

Hitting the panic button

Few things go well in excess. And the banking regulator thinks unsecured credit isn’t one of them.

The Reserve Bank of India has been vocally concerned about how unsecured credit has blown through the roof. Now, it is taking action.

With a circular that sent shockwaves across the industry, the RBI on Thursday mandated that unsecured credit products will now attract higher risk weights - effectively putting the regulatory speed bumps on the road for booming consumer credit. Who will trip up, and how much will we slow down? Let’s find out.

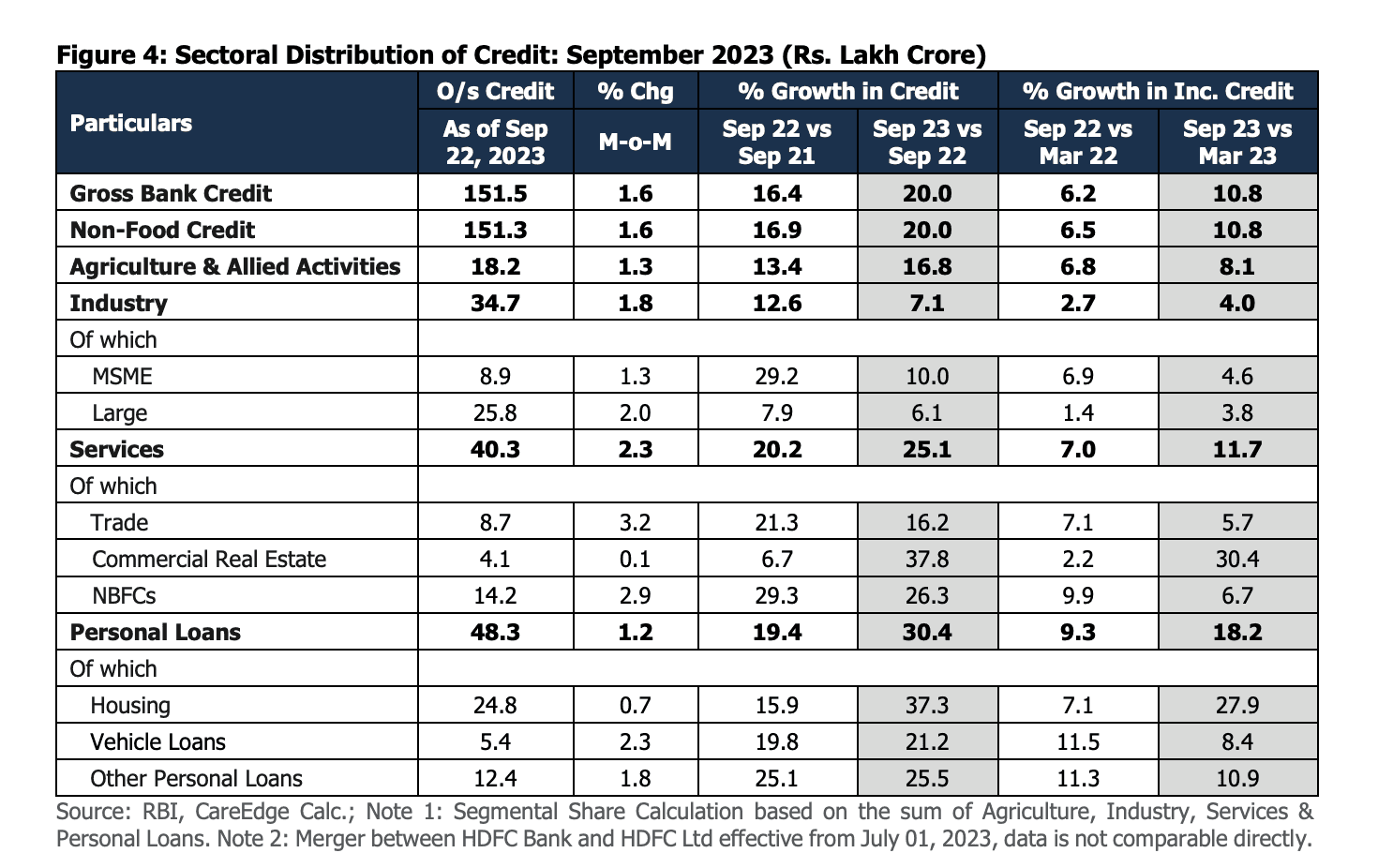

First, let’s establish just how big this blow-up has been. NBFCs saw their AUM rise by 25% in FY23; unsecured consumer credit rose the highest by about 45%. At the same time, banks also got a share of this unsecured pie, as personal loans have grown by 25% -30 % in recent quarters.

This steady growth of unsecured loans is fueled by three big factors - digital lending-induced unforeseen credit acceleration, economic growth, and rising consumer spending across all baskets.

Even though growing credit is a sign of the economy’s health, the regulator is worried that we’re heading into an overheating phase. The problem with too much unsecured lending is that there are few guardrails if a section of the borrowers are overleveraged and defaults. At the same time, adverse economic conditions such as job losses could also lead to unforeseen defaults that might blow up in lenders’ faces.

RBI writes the prescription

Now, the RBI wants lenders to pay for all this lending. Literally. The central bank has readjusted its risk weights and has upped the ante for personal loans except vehicle, education, housing, and gold loans. The new risk weight is 125% - up from 100% earlier.

Risk weights are assigned by the regulators based on the perceived riskiness of asset classes. A higher risk weight implies that the bank/NBFC would now have to set aside more capital to cover potential losses on their corresponding exposures.

This move by the RBI also includes a rise in the already high risk weight of credit card outstanding from 125% earlier to 150% now.

The move will do the following:

Deter lenders from playing fast and loose with unsecured credit - additional capital requirements will mean that lenders might go slow on disbursements and take stock of existing portfolios’ health.

Increase costs: The RBI has increased risk weights for banks lending to NBFCs by 25%. This means that NBFCs cost of capital will increase and thus eventually get passed on to the borrowers as well.

Trade-offs: An interesting impact of this move will be on the FinTechs and lenders with exposures to various segments apart from just personal credit. With the bolts tightening here, and cost-arbitrage in play - will the money move away from personal loans to something else?

“Unlike banks, the impact on NBFCs is on both sides of the balance sheet (assets and liabilities), and our calculations suggest that the increase in risk weights on bank loans to NBFCs could push up the cost of bank borrowings for NBFCs by ~10- 30 basis points (bps) and dampen capital ratios by ~30-450 bps,” a note from Nomura said.

We’ll see how it plays out in the field but for now, the referee has blown the whistle.

This is all for this week. As always, leaving some reading recommendations below.

Reading list

Decoding RBI credit risk weight impact across banks, NBFCs; how each lender will lose, gain

NBFC assets to grow 25-30 pc in FY24 and FY25; unsecured loans need monitoring: Icra

Why an advanced rules engine should be the core of lenders’ ONDC strategy

Transforming Credit Underwriting: The Power of Alternative Data in Income Estimation

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources