The Pattern #134

These 3 RBI charts show what lending will look like in 2024

Mayank Jain

Head - Marketing and Content

·

Jan 5, 2024

Hello everyone,

Welcome to 2024 and the 92nd edition of The Pattern, a weekly newsletter with the latest banking, finance, and technology insights.

It’s the start of a fresh year; making predictions is the season's flavor. Be it the financial services industry or the ozone layer depletion, crystal ball gazing is aplenty on the internet this time of the year.

However, I decided to steer clear of empty predictions regarding the lending rocketship in India and, instead, add some data and facts to improve the pixel count of the picture. And what better source than the regulator itself?

In the last week of December, the Reserve Bank of India published its annual report on trends and progress of banking in India. It also presented some interesting nuggets that point towards the overall banking trends - but let’s focus on the future of lending.

Let’s take a look and see if something surprises you.

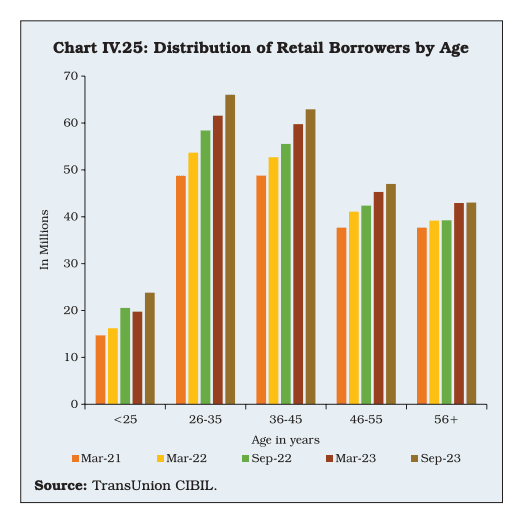

Borrowers get younger

In a poetic ode to the instant gratification age of Reels and TikTok - lending is also getting Gen-Z-fied. We’ve written aplenty on the rise of digital lending, but the latest data also shows that young adults are increasingly becoming beneficiaries of formal credit.

The data suggests that 53.1% of retail borrowers were between 25 and 45 years old as of September 2023. This is more than half of total retail lending. An additional 40 million borrowers knocked on lenders’ doors between March ’21 and September ’23.

In 2024, this trend is expected to continue as lending becomes an integral part of newer platforms and apps and becomes more accessible to even younger consumers who interact more with Cred and Zerodha than their primary bank.

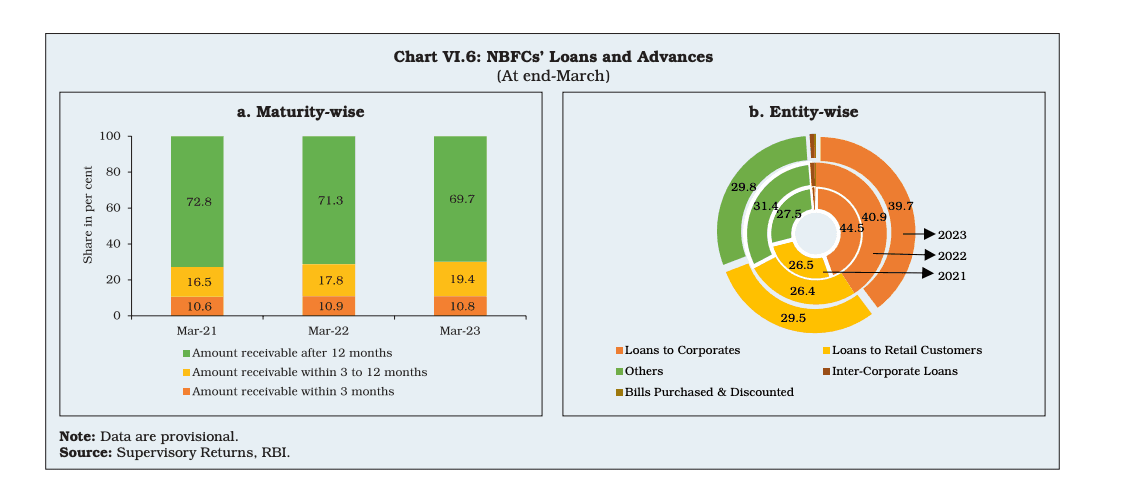

2 . Loan tenures are getting shorter

It’s not just the borrowers; even the credit products themselves are evolving and seem to be embracing the mantra of ‘instant gratification’.

Amidst liquidity tightening and competition from banks in segments such as vehicle loans, NBFCs leaned further towards unsecured lending. As a result, unsecured loans witnessed twice as much growth as secured credit in 2023. An extension of this is the resultant reduction in average tenures.

Loans receivable within 3-12 months are gradually increasing in share in the overall NBFC lending even as long-term loans are still over two-thirds of the total portfolio. However, the prevalence of shorter tenured-small ticket loans is likely to increase even further as digital products mature.

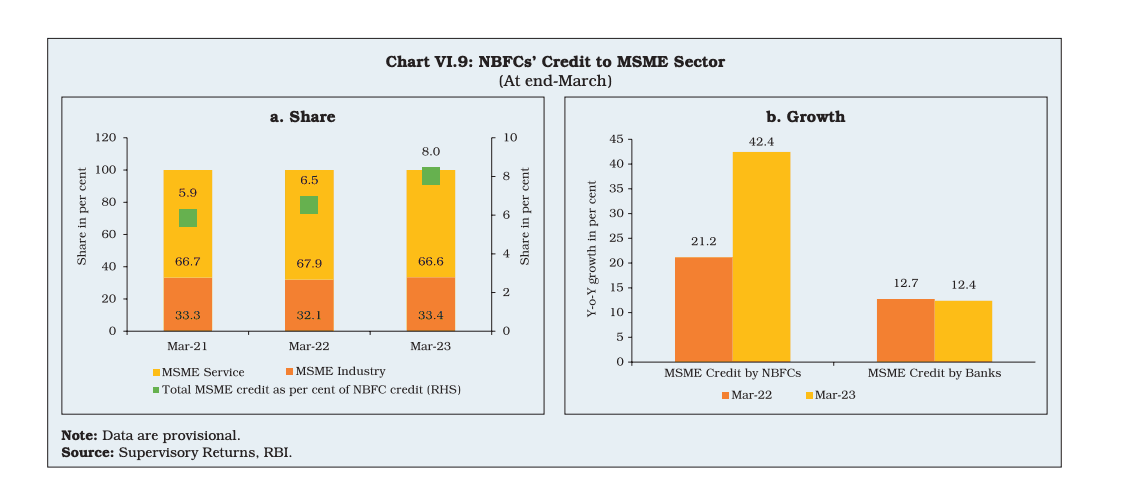

3. NBFCs are stealing MSME borrowers from banks

The hottest thing after retail personal loans in the industry currently is MSME credit. The large population of small businesses that are growing and yet, credit starved, makes them a lucrative borrower pool for all lenders. However, it’s the NBFCs that are shining here and leaving the legacy banks behind when it comes to providing them credit.

The latest data suggests that NBFCs’ credit to the MSME sector grew a humongous 42% in the last year, compared to a 12.7% growth in credit from banks. NBFCs, in fact, outdid their own previous year’s performance where their MSME credit jumped 20% year-on-year.

The regulator believes that custom financing solutions and co-lending frameworks are the secret ingredients to this recipe of success.

“Credit growth by NBFCs to the MSME sector was more than three times that of banks, benefitting from their ability to offer customised financing solutions,” the RBI report states.

Final word

The above charts show where we’re headed - in a more digital world where lenders will find ways to capture new borrowers, build custom products to please them, and overall ensure that the credit growth bandwagon doesn’t come to a halt. And we’re here for it!

That’s all for this week. As always, leaving some interesting data points and reading recommendations below.

Between the digits

6x AI: The RBI constructed an AI adoption index analyzing annual reports of Indian banks between 2016 to 2022. It found that private banks’ use of AI increased six times while public sector banks also embraced AI-related terms in their communications 2.5 times more over this period.

14,483 frauds: In the first half of 2023, close to 15,000 frauds were reported by banks - almost thrice the amount reported in the corresponding period in the previous year. However, the amount involved was less than one-fifth of the previous year’s tally.

60%: The market for gold loans is glittering and NBFCs are holding their own. Latest analysis suggests that the market share of NBFCs is at a strong 60% despite heavy competition from banks. Will it hold up is anybody’s guess.

Reading list

Govt may mandate video recording by insurance agents to curb mis-selling

Transforming Customer Qualification and Cost Efficiency with FinBox BureauConnect

Customers' complaints against credit information companies increasing: RBI

Transforming Credit Underwriting: The Power of Alternative Data in Income Estimation Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources