The Pattern #134

Credit growth has a dark underbelly that few noticed

Mayank Jain

Head - Marketing and Content

·

Feb 23, 2024

Hello everyone,

Welcome to the 98th edition of The Pattern, a weekly newsletter where we dive into the world of technology, economy, and finance. Let’s get started.

Save the deposit

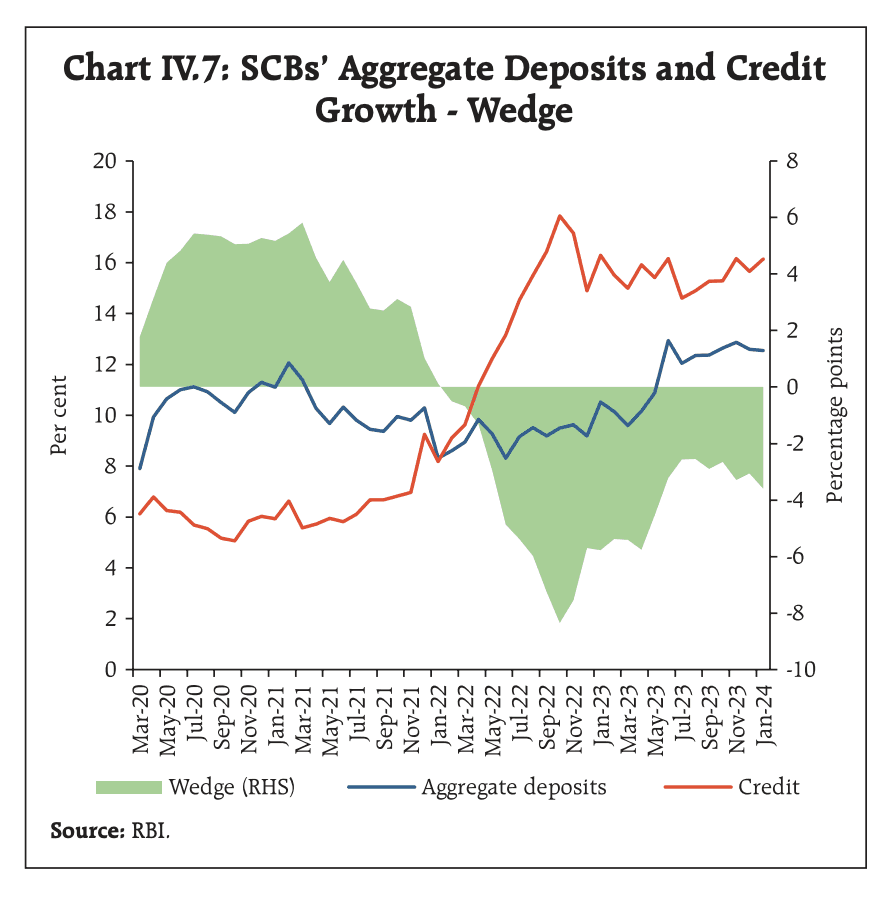

Last year, bank credit grew in high double-digits year-on-year. This is a good thing. However, even with 15%-16% overall growth, retail credit including unsecured personal loans and credit cards etc. grew much faster with more than 25% y-o-y growth. This is also a good thing (to an extent).

In the same period, deposits made by Indian citizens in banks grew by only 10% year-on-year. By itself, this is a good thing. But seen in juxtaposition with consistently higher credit growth, it can be a bit disturbing.

The relationship between credit and deposits in banking is one of mutual harmony. Both must work in tandem to keep the economy from overheating or collapsing. This is so because credit is given out by banks on the funds it receives as deposits. Thus, more deposits can mean more room to boost credit. And vice versa. However, when credit growth outstrips deposit growth, problems can start to mount.

Take the case of HDFC Bank, one of the largest lenders in the country, which is currently taking a beating in the public markets even after announcing better-than-expected earnings in the last quarter. This is because the bank’s credit-deposit ratio – a measure of its dependence on deposits for lending – reached an alarming 110%. The number was similar at YES Bank in December 2019, a quarter before its collapse.

“Now, for the quarter ended 31 December 2023, HDFC Bank recorded advances of Rs 24.6 lakh crore and deposits of Rs 22.1 lakh crore. This means that it lent Rs 2.5 lakh crore more than it garnered in the form of deposits—this is the money it borrowed from the markets, and it costs more than deposits. The strain of these market borrowings is visible in the bank’s net interest margin,” wrote The Morning Context.

But this is not about just HDFC Bank. Almost all banks are currently on this spectrum, from wanting more deposits for comfort to being dangerously deposit-starved.

The situation has worsened due to Indian consumers finding equity, mutual funds, and other investment instruments more attractive than bank deposits to generate extra returns on their idle funds.

“All of this is leading to a deterioration in the loan to deposit ratio (LDR) levels,” said S&P Global Ratings in a recent report.

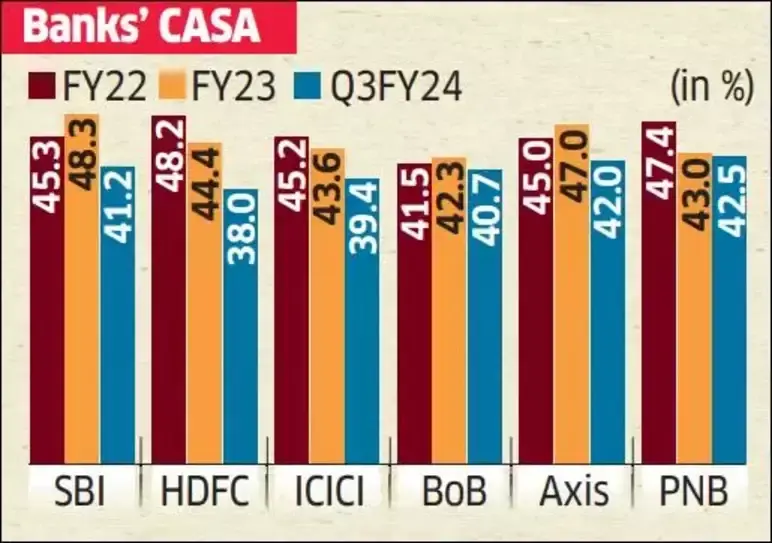

Further, the CASA ratio - which measures the current and savings account deposits in banks – has declined by almost 5 percentage points in the last 18 months to land at 40.5% in September 2023, compared to 45% in March 2022.

"There has been a shift in the savings pattern, especially in the metros, where banks used to get most of their large deposits from,” P R Rajagopal, executive director, Bank of India, was quoted as saying by ET. “Thanks to digitisation, these savers have access to other savings products, such as mutual funds, denting banks' ability to garner deposits.”

So, banks are finding it hard to drum up deposits due to the popularity of SIPs. Elections are approaching – that makes cash a favourite. Plus, the credit demand refuses to go down. For banks, it’s going to be an uphill battle to simultaneously cap credit growth while boosting deposit growth. We’ll see what happens. What RBI thinks of this, we might find out sooner than later.

This is all for this week. As always, leaving some interesting data and reading recommendations below.

Between the digits

Rs 21,781 crore: Inflows into equity mutual funds increased to Rs 22k cr in the month of January to hit a 22-month high .

55% Third-Party Fraud : A new report on fraud in Indian banking suggests that more than half of all fraud is third-party takeover fraud which essentially involves someone else getting access to a bank account and then initiating transactions.

Reading list

Paytm bank RBI Ban: Indian fintech is fast, furious — and fraudulent?

India set to standardise 'know your customer' banking checks

Google Pay takes its QR soundbox to small merchants in India after trial run

How Account Aggregator improves information sharing through journey design

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to always get all updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources