The Pattern #134

The joy of rising unsecured lending might turn to ashes

Mayank Jain

Head - Marketing and Content

·

Jun 23, 2023

Hi everyone,

Welcome to the 65th edition of The Pattern, a weekly newsletter where we unpack the latest from the worlds of finance, technology, and the economy.

I’d like to start this edition with a little blast from the past – this epic line delivered by Tyrion Lannister on Game of Thrones (early seasons, obviously):

“A day will come when you think yourself safe and happy, and suddenly your joy will turn to ashes in your mouth, and you'll know the debt is paid.”

- George RR Martin

What does this have to do with this newsletter? Let me break it down.

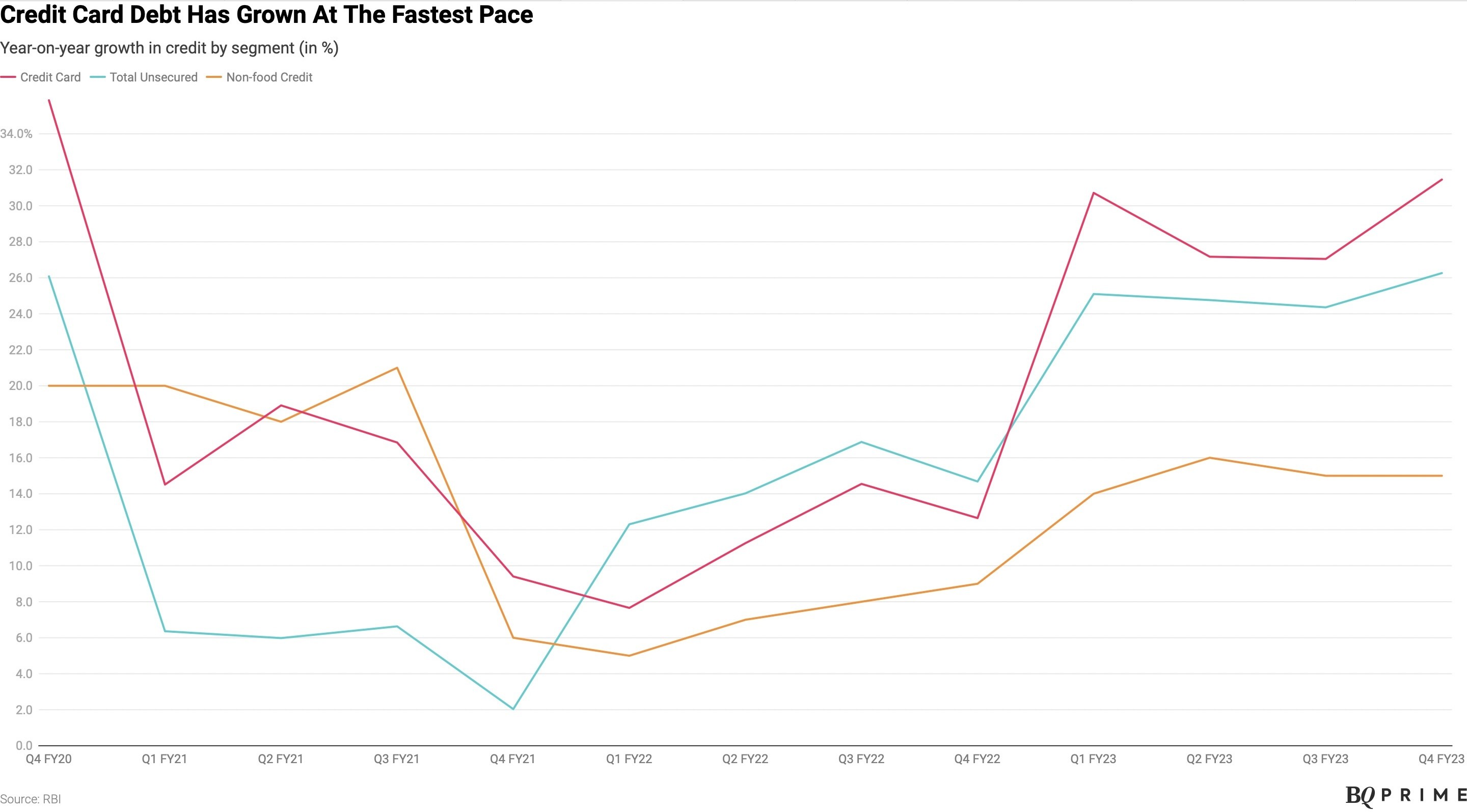

Here’s what’s joyous – there seems to be an uptick in economic activity since the growth in lending, lukewarm during the pandemic, has soared Q1 FY23. Unsecured credit grew 26% year-on-year at the end of the previous year. The corresponding numbers for credit cards and non-food debt stood at 31.5% and 15% respectively.

Here’s why it might turn to ashes – the rapid pace of growth across all these ‘consumer’, unsecured loan categories has alarmed the Reserve Bank of India (RBI). And now, it’s quietly intervening to prevent this spike from snowballing into a crisis.

Why such growth is concerning

The speed at which unsecured lending has grown over the past year, especially in the credit card segment, signals that consumers are increasingly relying on credit to make purchases. In fact, credit cards toppled debit cards to become the second largest source of transactions after UPI in April this year.

Credit card spends during this period were largely driven by discretionary spending on travel and entertainment. However, industry experts have also been quoted as saying that the high volumes could be attributed to transactional spending instead of large-ticket purchases or EMIs.

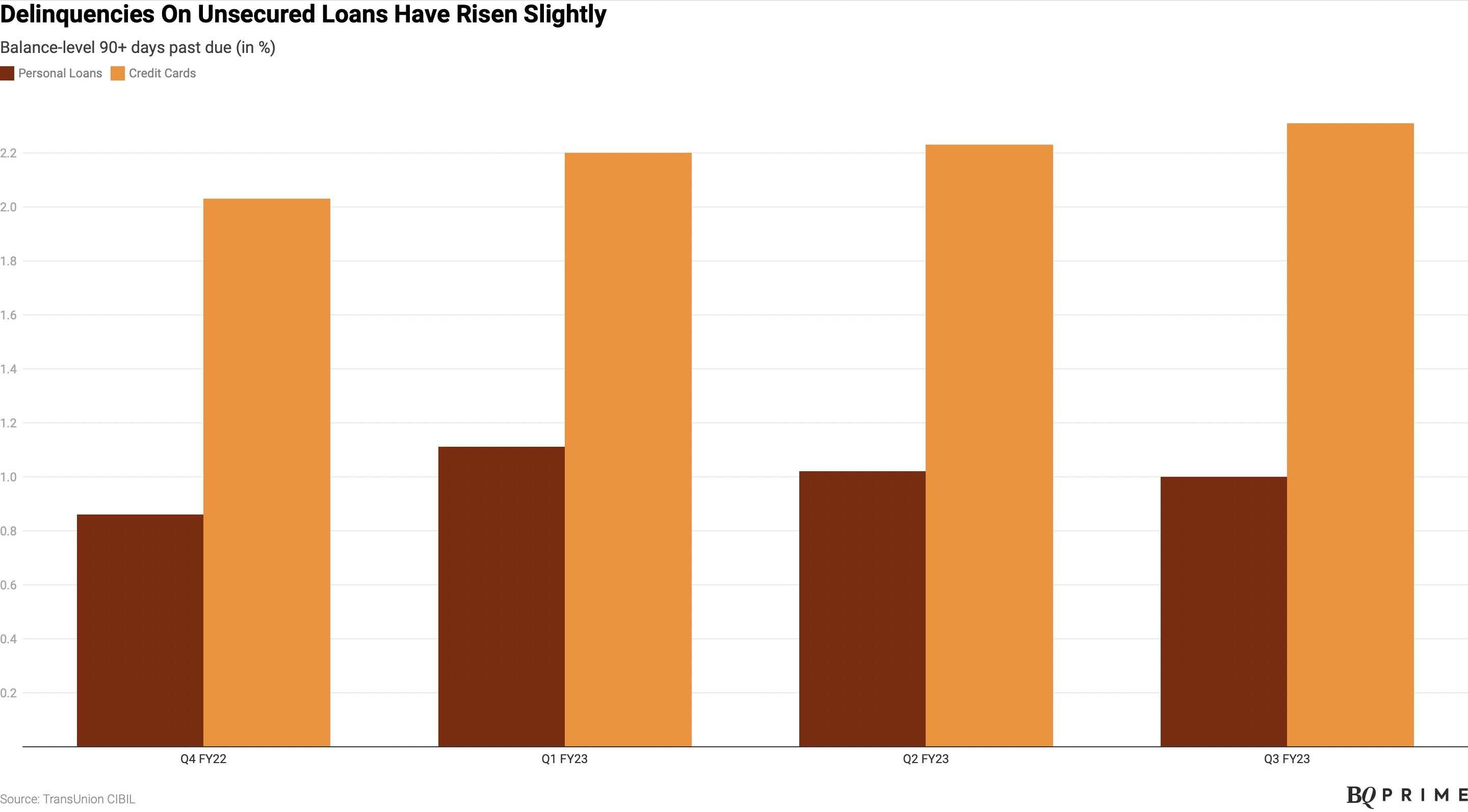

Moreover, banks’ credit card NPAs rose by 24.5% in April to December 2022, the RBI responded to a right to information (RTI) query earlier this week.

TransUnion CIBIL data showed that in December 2022, the delinquencies rose across personal loan and credit card categories. Overdue balances for more than 90 days on credit card accounts rose 25 basis points year-on-year.

Lastly, even though the gross credit offtake grew 16.3% year-on-year in January 2023, unsecured personal loans and NBFC lending were responsible for the bulk of it. Contrast this with findings from the Indian Retail Loans Overview April 2023 report – home loans grew 16% from December 2021 to December 2022, while personal loans saw an astronomical rise of 57% during the same period.

What’s being done to tackle it?

The RBI is mulling risk weights on unsecured lending to rein in the growth of lending to these segments. The objective is to curb non-performing assets across these categories from arising in the future.

At present, the risk weights on personal loans and credit cards is 100% and 125% respectively. Increasing the risk weights further will force lenders to rein in unsecured lending as it requires that banks consume more capital to disburse these loans.

Another attempt to curb the allocation of unsecured loans is afoot. NBFCs, which CIBIL reported to have witnessed the sharpest rise in personal loans, are now reducing their exposure to new-to-credit customers. Loan approval rates to this segment declined from 35% in December 2020 to 24% in December 2022.

Is unproductive lending dangerous?

It’s clear that the increase in such unsecured lending is considered dangerous in the long run. Such debt is used for little more than sustenance, contributing next to nothing in terms of asset creation or productivity. For lenders, the absence of collateral guarantees 100% losses in the event of a default.

What’s the alternative, then? Should lenders readjust their portfolios to favour secured lending?

Our CEO Rajat Deshpande put it like this in his newsletter last year –

“Collateral isn’t as secure as it seems. Secured lending can actually sometimes be a misnomer.”

During uncertain economic conditions, lenders can become more inclined towards secured lending, assessing credit risk based largely on the value of the collateral. While this seems like the sensible thing to do, lending based on collateral minus robust underwriting might still result in defaults.

Moreover, lenders may be compelled to lend more to allow borrowers to pay off the interests on their existing loans. At the same time, it becomes critical to make low-risk investments in the economy to offset the ill-effects of compounding interest.

Portfolio reallocation is not the solution

Here’s how I feel about the proposed solutions to this problem –

1. Collateral doesn’t guarantee risk-free investments.

2. The RBI’s initiative to add risk weights is a welcome institutional intervention.

3. NBFCs’ staying clear of lending to new-to-credit customers isn’t a sustainable option.

One solution sustainable in the long run is to build robust underwriting capabilities. New-to-credit customers, especially, are considered difficult to underwrite given their lack of credit history and unavailability of reliable data.

That’s all from me this week - as always, leaving you with my favourite reads and interesting numbers from this week:

Between the digits

9.6%: The rise in the Bank Nifty over the last three months

73%: The share of non-cash retail payments made through UPI in the year to March

4.25%: Inflation rate fell down in India for May 2023, since April 2021

Rs 2,313 crore: Amount disbursed in merchant loans in the March quarter

Reading list

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources