The Pattern #134

RBI's Financial Stability Report and the danger of premature celebrations

Mayank Jain

Head - Marketing and Content

·

Jun 30, 2023

Hi everyone,

Welcome to the 66th edition of The Pattern, a weekly newsletter where we unpack the latest from the worlds of finance, technology, and the economy.

Let’s jump right in with some good news! According to the Reserve Bank of India’s (RBI) latest Financial Stability Report (FSR) , Indian banks’ gross bad loans are set to fall to a ten-year low of just 3.9%. Net non-performing assets (NPAs) have also fallen to 1% of total loans - the lowest since 2011.

These developments are in line with an Assocham-Crisil study from March this year, which predicted that bad loans would decline to less than 5% in FY 23, hitting a decadal low of below 4% by March 2024.

This was attributed to several causes, including a clean-up of books by banks in the last few years, strengthened underwriting practices, and post-COVID recovery.

Several publications have gone on to claim that this report paints a picture of resilience and a “robust economy”. But I’d suggest that any celebrations be tempered with a little bit of caution.

All's not well in the retail lending space, with the FSR adding that nearly 10% of borrowers in this segment are missing their monthly payments. According to the data in the report, the total of SMA-0, SMA-1 and SMA-2 in the retail advances in the public sector banks (PSBs) was 9.4 per cent as of March 31.

These borrowers are keeping their accounts from being classified as NPAs by making some payments before the 90 day mark. Talk about living on the edge.

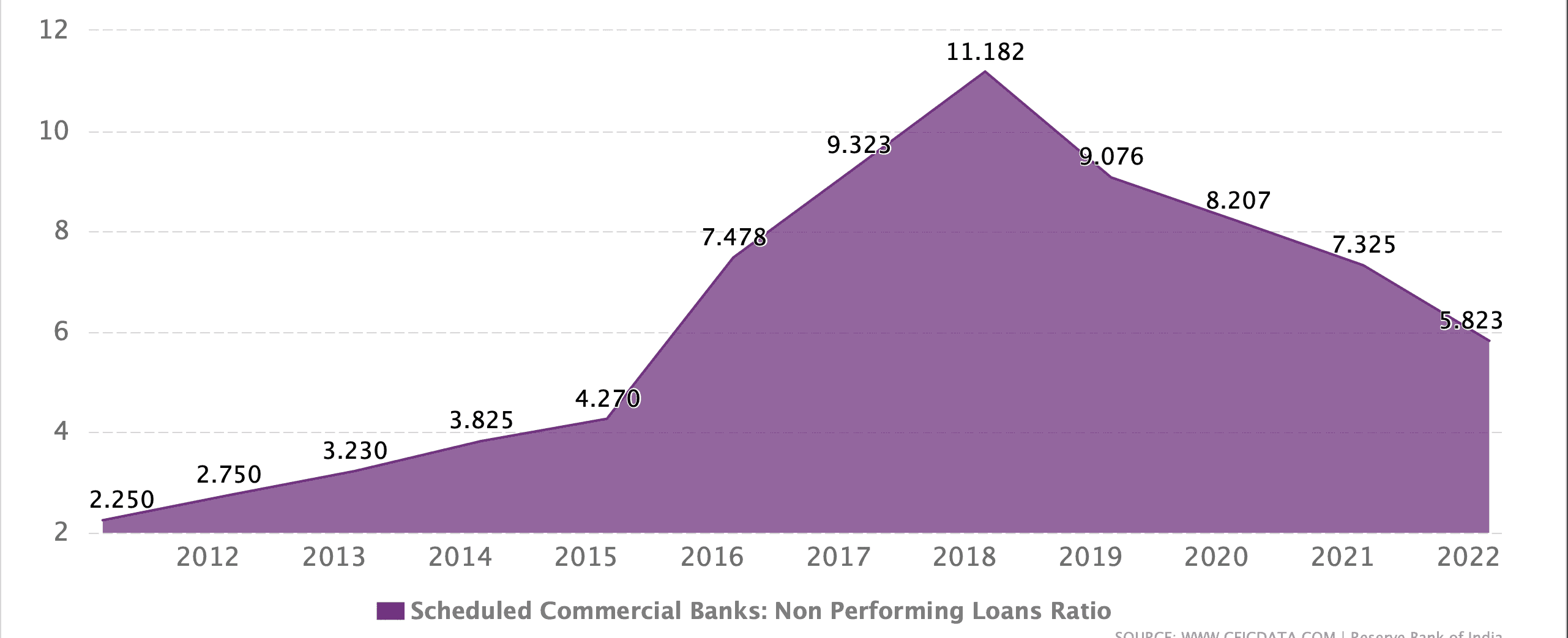

What’s more, the report itself shows that bad loans tend to rise and fall periodically. According to this piece, gross NPAs as a proportion of total assets stood at 11% in 2002, fell to 2.5% by 2010, climbed back up to 4.1% by 2014, soared to 11.5% by 2018, and fell back down to 3.9% by 2023.

So the real question is, what are the underlying causes for the periodic rise in bad loans, and what can be done to address them? Or what about the fact that scheduled commercial banks (SCBs) wrote off a total of Rs 11,17,883 crore in the last six fiscal years?

Taken from: https://www.ceicdata.com/en/indicator/india/non-performing-loans-ratio

It’s tempting to focus on the good news and gloss over what makes us uncomfortable. But that’s not sustainable - especially when India’s economic growth was described as “ very fragile ” in just February this year.

That’s all from me this week - as always, leaving you with my favourite reads and some interesting numbers from the week: Between the digits:

1,500: Number of Bandhan Bank branches across India, in just 8 years

USD 10 Bn: The amount Google has pledged for India's digitisation fund

INR13.25 trillion: The amount GST revenues have grown to in 2022-23

Reading list:

Bank Giant Bigger Than Morgan Stanley Arises From India Merger

Why RBI penalised credit info companies and what borrowers should do now

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources