The Pattern #134

Booming digital credit still struggles to reach where it’s needed

Mayank Jain

Head - Marketing and Content

·

Aug 25, 2023

Hello everyone,

Welcome to the 74th edition of The Pattern, a weekly newsletter where I dissect and unpack the latest rumblings from the world of finance, technology, and industry. Let’s get started.

The Sisyphean challenge

This week, like many others, saw various research reports come out on the state of digital credit in the country. One of these, released by Equifax and FACE - a FinTech association - stated that digital credit had grown leaps and bounds in the first half of the financial year.

The report, now widely being reported in the media as yet another bellwether of FinTech’s rapid inroads into the Indian ecosystem, claims that the digital lending sector disbursed more than 76k crore in loans, an increase of 61% year-on-year.

Other highlights from the report include a deeper penetration of digital credit in the interiors of the country with tier 3 cities accounting for 40% of all disbursements and tier 2 cities accounting for another 35% of disbursements.

At the same time, almost 80% of digital loans are availed by people under 40 - speaking to the age and accessibility bias that persists in the digital lending space.

The report also highlights how it’s mostly personal loans and short-term credit that are fuelling the volume expansion in the digital lending industry. Most loans were less than six months long in duration - about 88% of them - and were closed much earlier than their stipulated term. While reports like these provide new insights, talking points, and reasons to believe - there’s a big problem of unknowns.

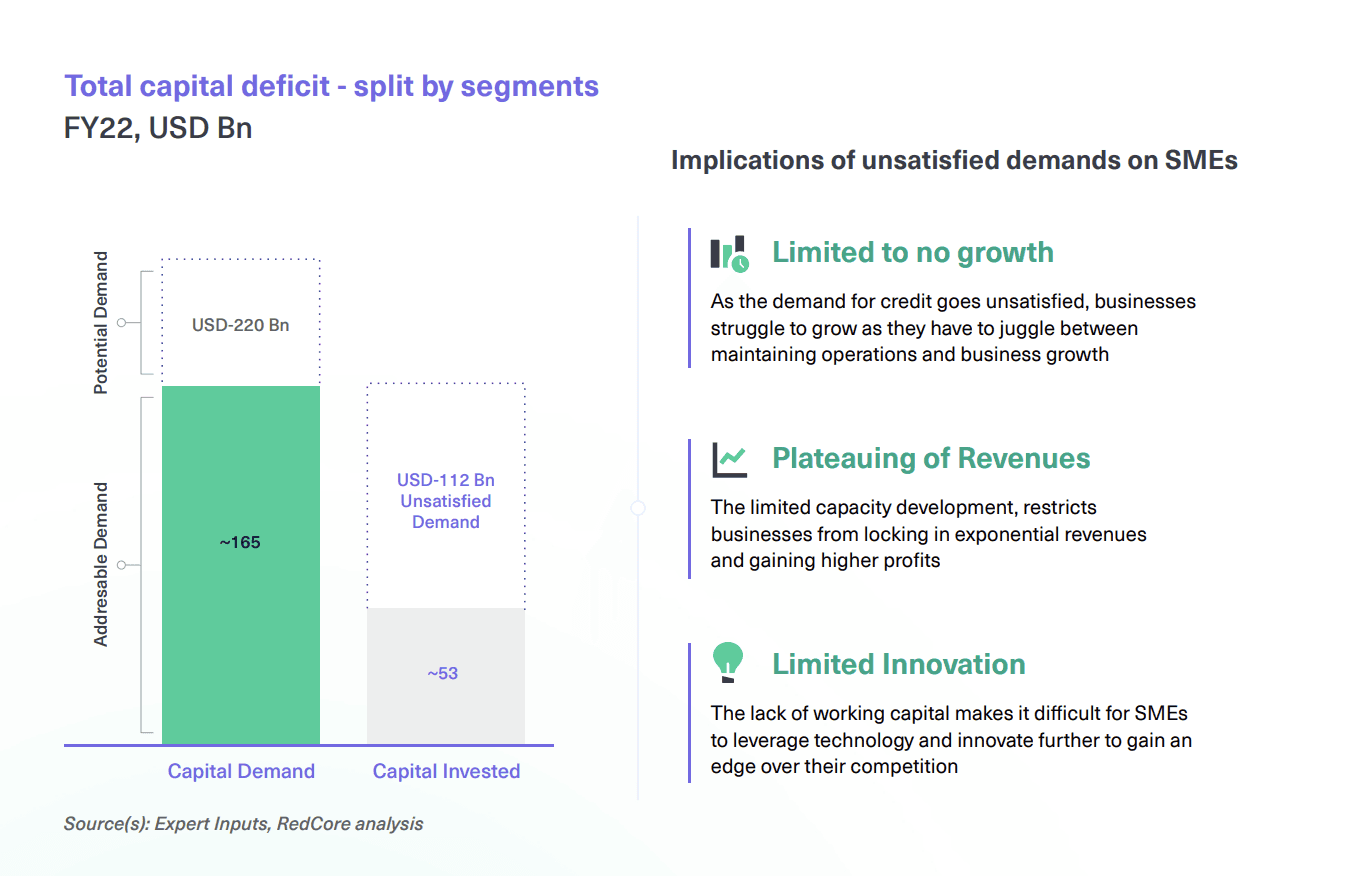

For instance, another report released this week by research firm RedSeer and commissioned by alternative financing platform GetVantage revealed that the SME credit gap is already $220 billion and it’s set to widen to as much as $569 billion by FY27. The report posits that this credit demand will mostly increase in tandem with the increased digitization of SMBs.

“Over the next few years, the demand for working capital is expected to rise steadily at a CAGR ~20% and is projected to reach ~USD 570 Bn. As the number of digitized SMEs is likely to double over the next 5 years, the consequent demand for working capital is also likely to follow a similar trend,” the report states.

This credit gap is worrying. It’s not only a cause of concern for the small businesses facing a working capital crunch but also for the overall ecosystem as the report states that traditional modes of financing aren’t able to address or reach these setups in many cases.

Seen in the light of the explosive top-line growth of digital credit, it makes one wonder whether the task at hand - of deepening credit access - is more Sisyphean in nature than thought earlier.

“The total demand for capital across digitized SMEs exceeds the available supply of credit offered through formal channels including banks, NBFCs, and other new age lending platforms. In other words, ~33% of the overall demand is serviced and about 67% remains unaddressed creating a massive divergence in the potential economic output of India. This gap has only widened over the last 5 years, where it used to be ~29% during FY17. This growing gap over the years indicates that the supply of credit is outpaced by the demand for credit, which is likely to widen in the future. Sisyphus used to drag a boulder over the mountain over and over only for it to roll down again. One can argue here that progress is being made - albeit slowly - and that the boulder isn’t rolling down the mountain. But, it makes sense to ask whether the mountain is simply too big to scale and perhaps more core strength is needed than just what technological levers are able to provide.

We’ll keep watching this space. For now, this is all from me today. Have a good weekend. As always, leaving some interesting data and reading recommendations below.

Between the digits

4% - Average delinquency in FinTech credit as measured by DPD90 according to the FACE-Equifax report Rs 14,485 crore - Digital credit disbursement from Paytm in Q1 FY24, up 160% y-o-y. The company is reinventing itself by becoming a major digital lending player and targeting micro-credit to fuel its growth 24.3% growth - According to finance ministry data, the government capital expenditure rose 24.3% year-on-year in FY23 - much higher than the 7% average recorded during the pandemic years

Reading list

India Can Expect 500 Mn Payment Customers Soon: Vijay Shekhar Sharma

Fintech Unicorn Mobikwik To Enter B2B Merchant Lending To Serve MSMEs

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources