The Pattern #134

The pull of unsecured credit - and the push for securing it

Mayank Jain

Head - Marketing and Content

·

Sep 1, 2023

Hello everyone,

Welcome to the 75th edition of The Pattern, a weekly where we dissect and report on the rumblings from the world of technology, finance, and economy.

We’ve had a relatively quiet week compared to the tumultuous last few months in the FinTech space. But, there’s still a never-ending stream of exciting goings-on that one must pay attention to. Let’s get started.

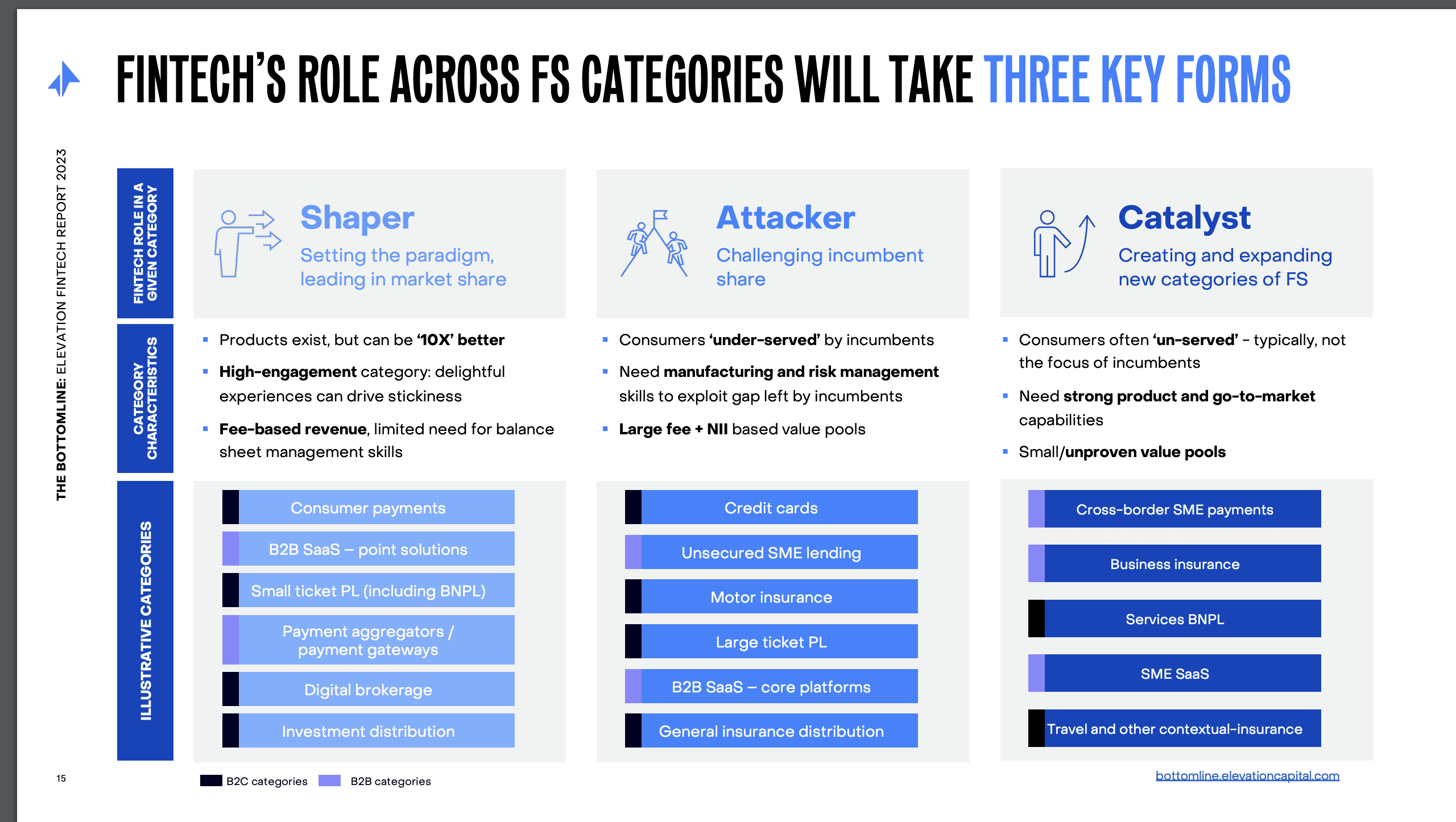

First off, we’ve got a brand new report on the FinTech space in India released by Elevation Capital in partnership with McKinsey. The report suggests that the Indian FinTech space is likely to see a value creation of $400 billion by the year 2030. This is 4x the current levels and it’s on account of funding to Indian fintechs doubling since the year 2018.

The report added that FinTechs have increased their share of digital payments to 70% of all transactions, an increase of 2.3x in FY22. Moreover, the report claims that FinTechs are sourcing 1.5x-2x more new-to-customer credits in the retail lending segment as compared to private lenders.

The study surveyed industry participants too and 50% of them believe that navigating regulations will be one of the major challenges for the FinTech sector going forward. Another 40% said that FinTechs might find it challenging to find durable business models.

This is just part 1 of a series of 10 in-depth reports lined up by the VC firm and the consulting giant. We’ll keep our eye on updates even as the sector basks in its glory and FinTechs continue to navigate the rapid digital transformation of financial services.

Securing unsecured loans

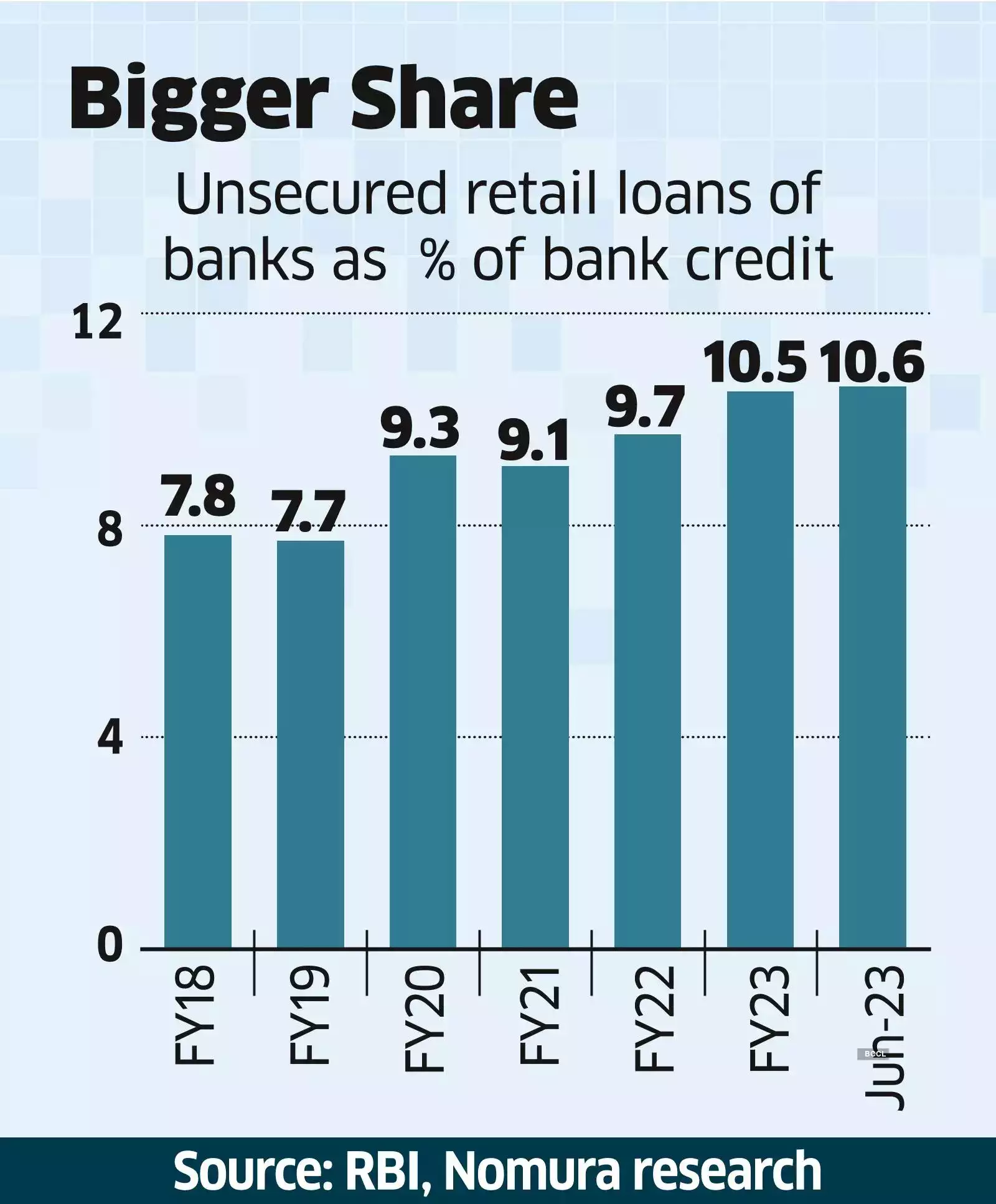

We’ve written a bunch about the rise in unsecured credit , why it worries banks and regulators as well as the possible implications of unchecked growth in unsecured lending for the broader economy. Now, a new report predicts that credit costs of unsecured loans could become the major contributor to large private sector banks’ provisioning by the year 2025.

Credit costs are the provisions banks make on the potential of making losses on their lending portfolio. The report by Nomura suggests that this could be about 250-300 basis points in personal loans and about 600 basis points for credit cards.

Even as the analysts warned of the rising provisioning needs, they predicted that unsecured credit growth might not necessarily lead to rising losses for banks or deteriorating income statements.

"While most lead indicators do not flag imminent risk for banks, the regulator’s repeated warnings on unabated growth in the segment, as well as concerns on rising consumer leverage have sparked investor concerns," the analysts said .

This comes in the light of unsecured credit steadily gaining a larger share of the banks’ total loan books. Even as revenge spending and consumerization lead to higher disbursements, banks are leaving no stone unturned to capture this demand across products.

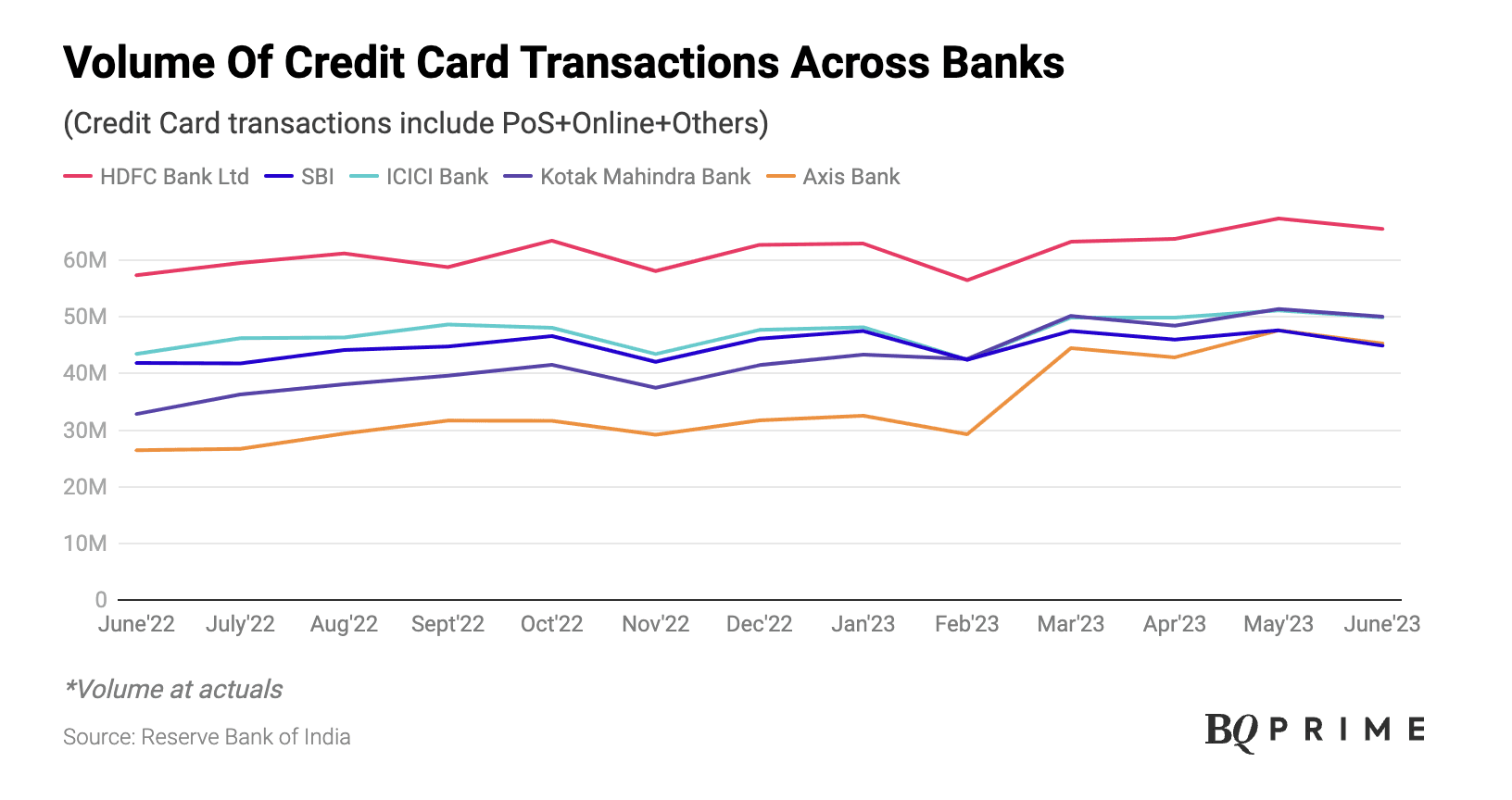

An example of this is HDFC Bank’s renewed push to gain market share in the credit card segment. The bank was barred from onboarding new customers by the RBI in December 2020. This saw its market share drop from 26% to 20% but the bank is now making up for lost time.

It’s launching a slew of new products in partnership with the likes of Swiggy and IRCTC with a rumoured Apple partnership card about to come next. The bank is aiming to boost its overall credit card user base as well as the volume of transactions by actively acquiring new users and capturing more user wallet share.

“At the same time, we will continue to identify relevant categories where customers are spending and focus on getting wonderful partnerships where we get significant value and thereby get the full customer wallet,” HDFC Bank Cards Chief Parag Rao said recently.

The bank is betting on credit cards to bounce back even harder now that BNPL as a product has seen a loss of traction and favor due to large players failing and fears of recession. The bank believes that credit cards and UPI’s linkage with RuPay credit cards might prove to be “excellent” BNPL surrogates.

We’ll see how that pans out. But for now, banks must focus on ensuring that quality of underwriting remains paramount even as they try to capture a growth spurt. Digital credit is a double-edged sword and a slight slip in portfolio quality can start a rather nefarious downward spiral - nothing that the regulator doesn’t keep warning about all the time.

This is all from me this week. As always, leaving some interesting data and reading recommendations below.

Between the digits

80-90% margins - NBFCs lending to risky borrowers at very high rates can sometimes expect to make 80% or more on the portfolio if borrowers repay loans on time.

12x - Digital loan disbursements in India have grown 12x in just 3 years between 2017-2020, according to the Elevation Capital report .

10 billion - UPI transactions crossed a massive 10 billion transactions a month milestone for the first time in August with a total value crossing Rs 15.14 lakh crore.

Reading list

India’s digital public goods networks can’t get enough of e-pharmacies

Moody's raises India GDP growth forecast for 2023, slashes outlook for 2024

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources