The Pattern #134

Credit lines rev up the UPI rocket ship

Mayank Jain

Head - Marketing and Content

·

Sep 8, 2023

Hello everyone, welcome to the 67th edition of The Pattern, a weekly where we dissect the latest rumblings in the world of FinTech, the economy, and the business of money. Let’s get started.

Credit where it’s due

This week was all about the buzz from the Global FinTech Festival in Mumbai and it seemed that the entirety of Indian FinTech had descended at Jio World Centre to celebrate and showcase innovation. It seemed almost impossible for anything else to survive in the din of that glitter but yet again, UPI managed to do that.

India’s banking regulator - the RBI - managed to steal the thunder by timing the announcement of credit lines on UPI just right. The central bank issued the notice to this effect on the eve of GFF’s opening and set the stage for exuberant speculation far and wide through the GFF venue.

Let’s unpack this.

UPI is arguably the most popular mode of digital payment. The RBI estimates that it contributes more than 75% to the total volume of retail digital payments in India. Thus, UPI, with its almost ubiquitous presence is the perfect vehicle to deliver credit in a credit-hungry nation.

The current proposal allows banks (and only banks!) to pre-approve credit lines for their customers and the customers, in turn, can utilize the lines to pay for goods and services through UPI. This is massive. It effectively turns a payment rail into a credit ecosystem and does so without adding friction - hopefully.

Usually, friction is the enemy of credit penetration. Friction is what kills the best-intentioned products. Be it during onboarding, assessment, or credit usage - any amount of a hiccup can all but guarantee that the customer isn’t returning to the lender.

And UPI is the ultimate friction killer. The payment medium succeeded largely due to its silky smooth operation. The payments are instant, real-time, directly reach the bank account and require only a four or six-digit code to be completed. Couple this with a live credit line and you’ve got a winner.

So what happens next?

Even though the announcement came this Monday, there’s been swift action and a flood of announcements everywhere. At least 4 different RuPay credit cards were announced during the GFF event by various FinTechs. Even though linking RuPay credit cards to UPI for credit transactions now feels like old news, it’s still only a couple of months old development and companies continue to launch cards to cash in on the gold rush.

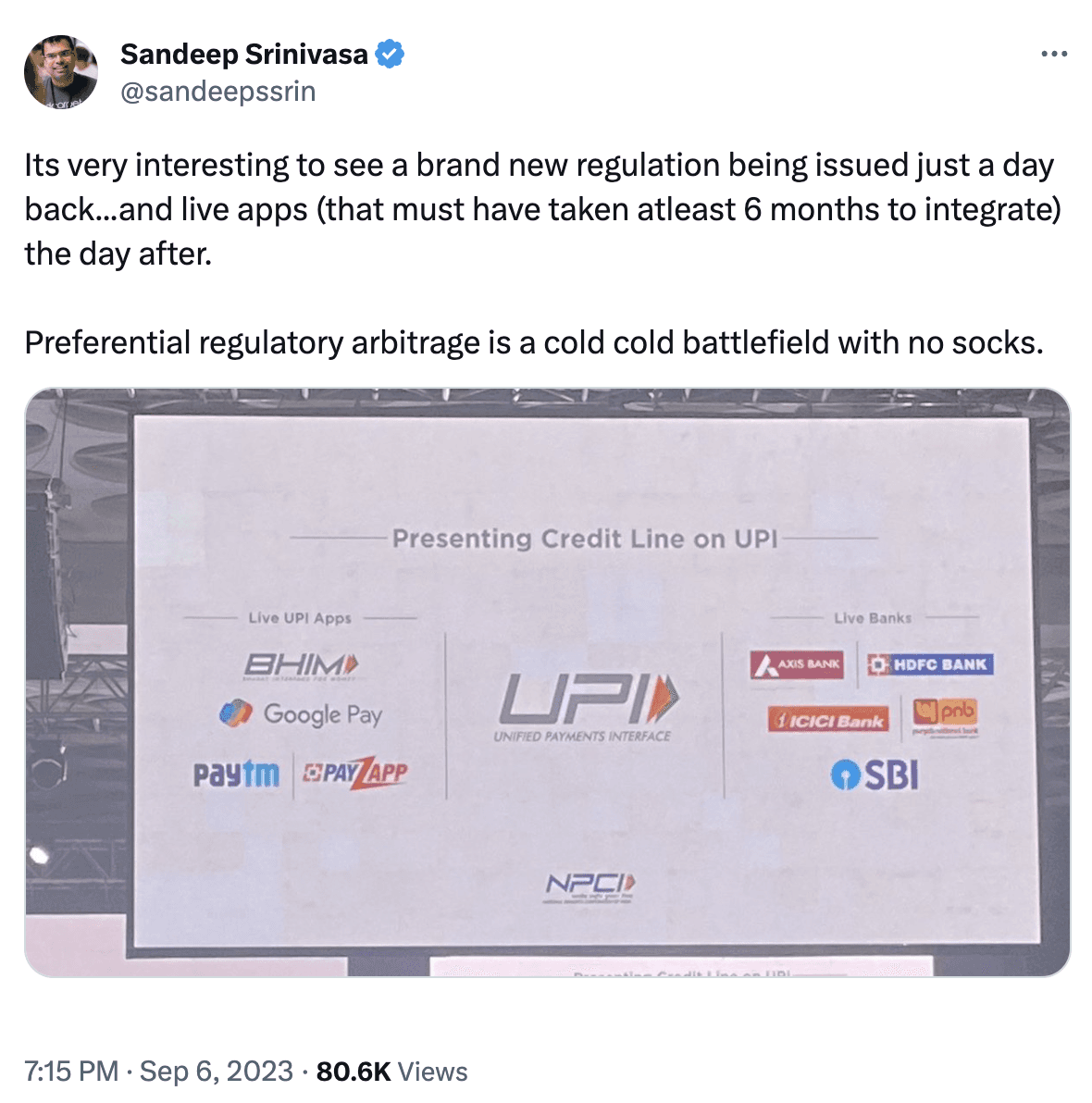

Even on the cardless credit lines front that was announced only this week, we’ve spotted NPCI claiming that apps like Google Pay, BHIM, Paytm, HDFC PayZapp, and banks including SBI, HDFC Bank, ICICI Bank, Axis Bank are already ‘live’ with this feature.

What being ‘live’ means is yet to be ascertained as there is little noise about actual products on this framework so far. But it’s pretty exciting that we’ve got major banks and apps already gearing up to launch new credit products.

Why is this a game-changer?

Now, let’s talk about the substance behind the hype. One must wonder why this is such a big thing and if it’s any different from credit cards (that can be linked to UPI now, by the way) or BNPL and overdrafts.

Here’s what Bernstein research has to say:

"This has laid the foundation for a surge in credit penetration. And the provision of credit, unlike deposits and payments, could lead to a sizable expansion of the banking profit pools,” the brokerage wrote in a September 5 note.

It added that the combination of UPI with credit will create superior products that will easily rival the existing options in the market such as credit cards. This is because:

UPI has wide adoption and it’s been primarily a payment use case

Ubiquitous adoption of QR codes and acceptance infrastructure

Viability of small ticket sizes in credit and progressive tenures

Personalized product construct and pricing for both merchants and consumers

This, all in all, will lead to one of the biggest credit profit pools in India, according to the firm.

“The large population of the country and the healthy profit per customer from lending businesses create the potential for the Indian banking sector to enjoy one of the largest retail banking profit pools in the world,” it said.

Even as perhaps a big shake-up in the retail credit space is underway, it remains to be seen how thorny issues like MDR, product construct, incentives, and merchant onboarding will work. Exciting times ahead.

For those wondering if it’ll kill credit cards, some experts seem to think both products are different and can simultaneously co-exist . We’ll have to wait and watch.

This is all from me today. As always, adding some interesting numbers and reading recommendations below.

Between the digits

12.33% decrease - Indian insurers reported a 12.3% decrease in new business premium income in the life insurance segment on the back of LIC doing lesser business in the April - August’23 quarter.

$361 billion - A document by the World Bank claims that more than $361 billion has been directly transferred to beneficiaries in India through the digital public infrastructure rails. This amount includes subsidies, social security benefits, and other payments from the government to the citizens.

Rs 1,000 - The government of India is planning to credit Rs 1,000 in the wallets of all G20 delegates in a bid to show off India’s impressive digital infrastructure at the summit.

Reading list

Without loss-making companies, Indian fintech would not have seen such growth: CRED’s Kunal Shah

World Bank lauds India's Digital Public Infrastructure in G20 document

Chief executives of shadow banks urge RBI to allow public deposits

How Account Aggregator leverages ‘informed’ consent to enable multiple use cases in digital lending

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources