The Pattern #134

4 charts on India’s save or spend confusion

Mayank Jain

Head - Marketing and Content

·

Sep 22, 2023

Hello everyone, welcome to the 78th edition of The Pattern, a weekly where we dissect and delve into the latest in the world of economy, finance, and technology. Let’s get started.

It’s been a relatively quiet week in the FinTech world but there’s been a bombshell of a data release from the Reserve Bank of India. The banking regulator released fresh data on household savings in the country and this data has become the talking point across the industry.

How does India save and invest?

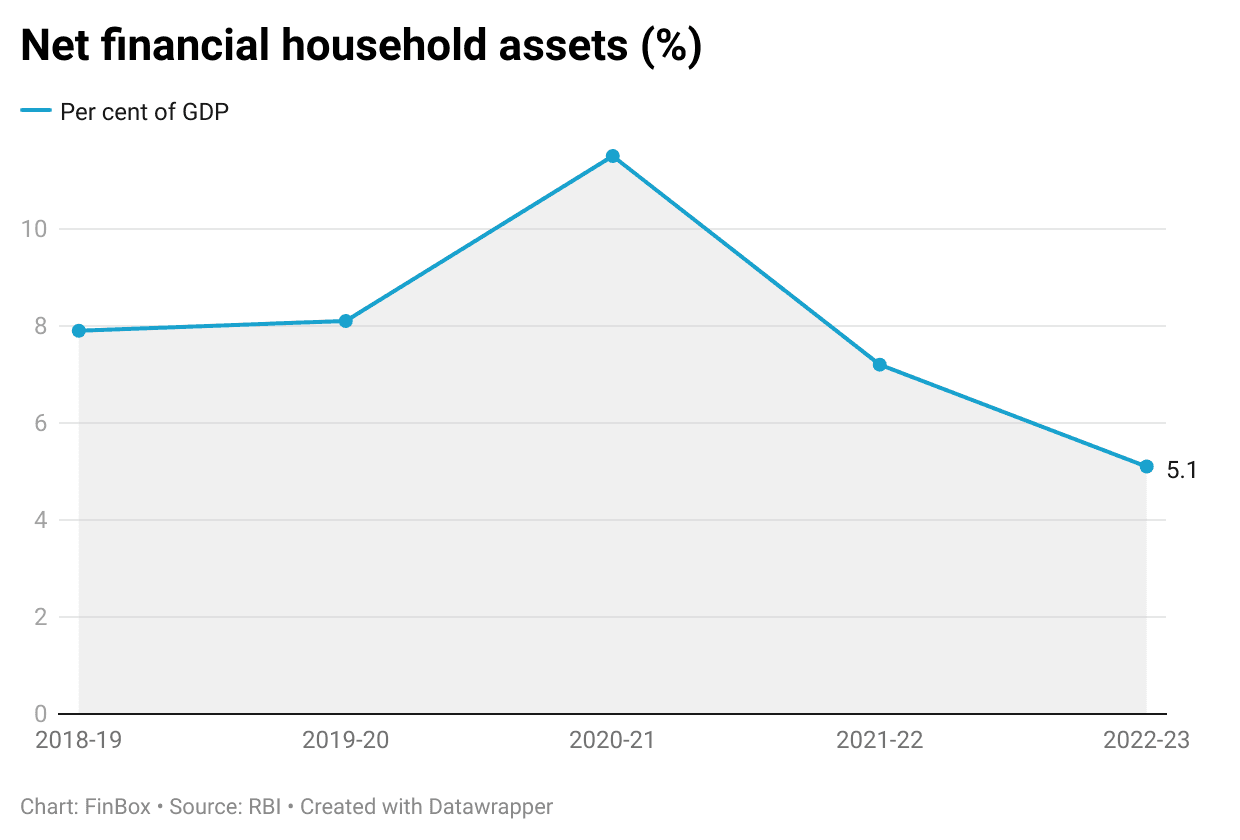

The report highlights a worrying trend - savings have dipped for Indian households to a multi-decadal low as a percentage of the GDP. This has caused much furor in the media as net household assets reached 5% of the GDP in FY23 as compared to 11% in FY21.

This is worrying policymakers and experts because a sustained dip in net assets either implies too much consumption expenditure or an increase in liabilities. The problem is, most guess, that in this situation it’s a combination of both.

“Lower gross savings means that people are saving less and consuming more. Higher consumption can be attributed to pent-up demand after the pandemic’s repression. ‘Revenge spending’ was in evidence as people went shopping and on holidays to make up for COVID deprivation,” wrote Madan Sabnavis, Chief Economist at Bank of Baroda in a piece for Mint.

Sabnavis added that one should worry about the sustainability of such high spending at a time when inflation has peaked and real income hasn’t really taken off.

We didn’t start the fire

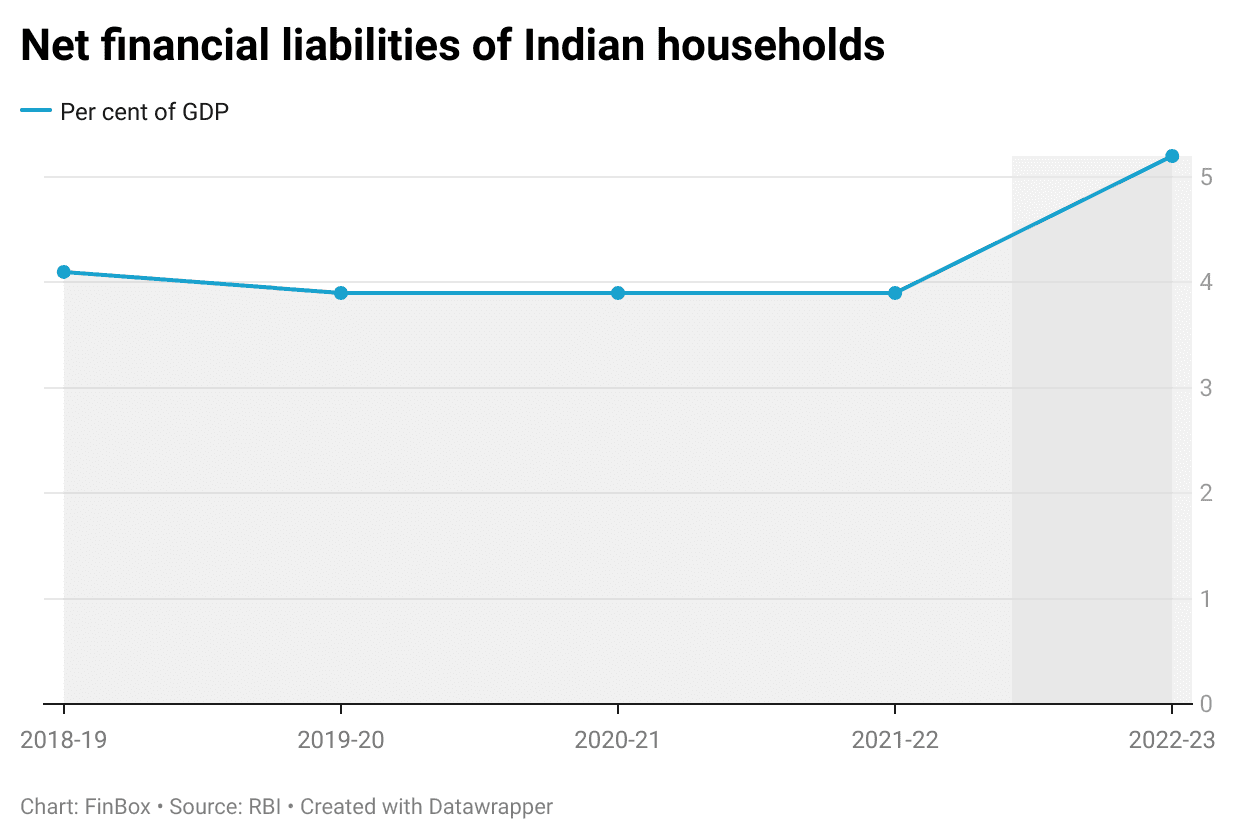

Secondly, a dip in the net financial assets has been coupled with a rise in the cumulative financial liabilities of Indian households. The data suggests that there has been an increase in total financial liabilities as it reached 5.8% of the GDP in FY23 as compared to 3.9% in FY21.

This comes at the heels of global agencies revising their growth outlooks for the country in the upcoming fiscal and a largely worldwide correction in income and output.

“The fall in net financial savings of households means that liabilities have increased faster than gross savings. This again can be a problem for an economy like ours,” Sabnavis wrote.

He, however, added that there’s a chance that increased liabilities could mean a rising consumption expenditure which can provide an impetus for growth and demand to the economy. It’s not clear yet which part of the thesis will play out in the long-medium term.

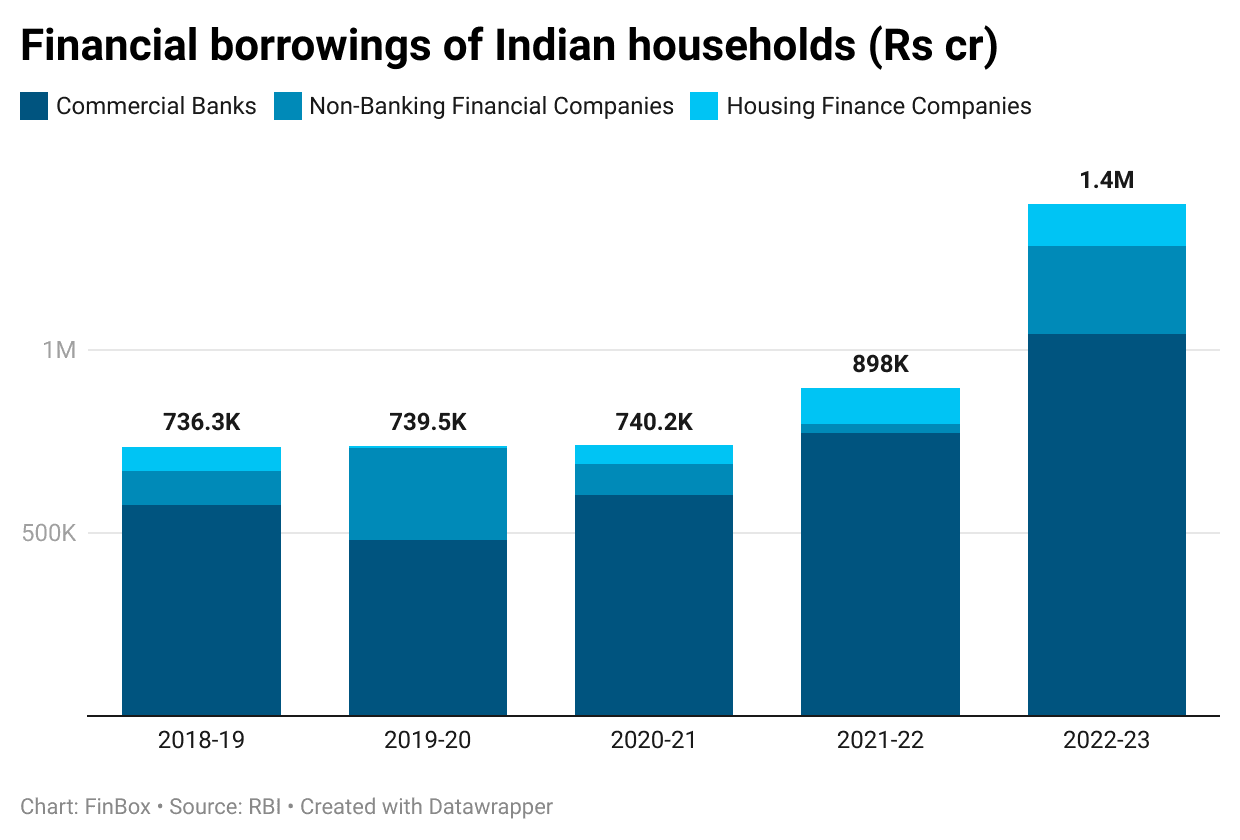

Meanwhile, Indian households’ formal credit exposure continues to rise. Loans from NBFCs registered a steep rise in FY23 even as overall banking sector borrowings rose from 3.3% of GDP in FY22 to 4.4% in FY23.

Economists suggest that this growth has largely come on the back of growth in housing loans, automobile loans, and personal unsecured credit. The first two create assets and add to the economic growth while the third, could be a worrying sign of over-leverage in certain income segments and one which the regulator has been consistently worried about.

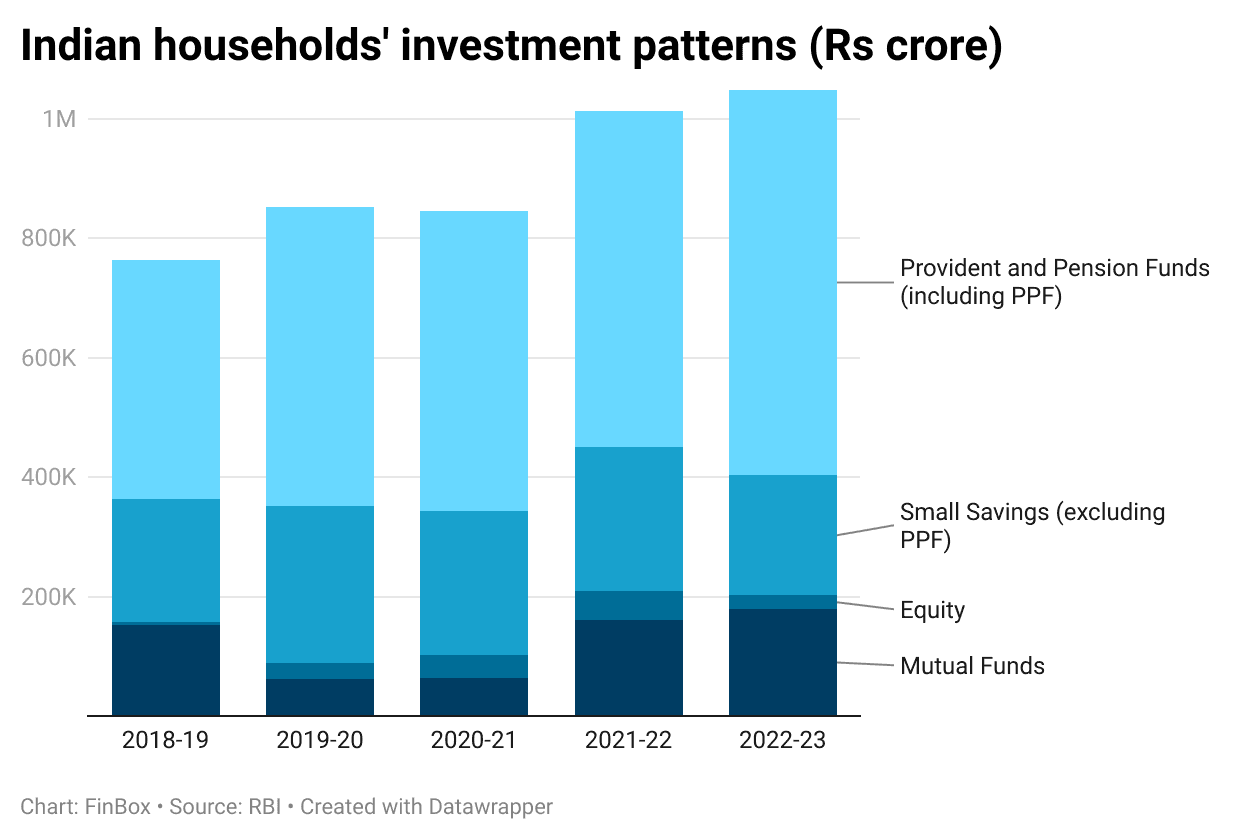

Even as Indians are taking on more liabilities, they are also becoming risk-friendly. The data on investment patterns shows a considerable increase in mutual funds, equities, and pension fund investments while people seemed to have cut back on safer avenues such as bank deposits and small savings.

This is a good sign for the overall deepening of the financial markets in India. It’s certainly going to lead to more maturity in the markets and bodes well for the country, especially as the benchmark JP Morgan EM bond index announced the inclusion of Indian bonds.

Today, the Finance Ministry allayed fears over this data by suggesting that people are saving less overall because now they’re taking loans to buy homes and vehicles.

“They added financial assets by a lesser magnitude than in the previous years because they have now started taking loans to buy real assets such as homes,” the ministry said in its statement .

Clearly, huge tectonic shifts are underway in the economy and one hopes that the RBI and policymakers continue to focus on improving oversight and ensuring sustained growth.

This is all from me today. As always, leaving some interesting numbers and reading recommendations below.

Between the digits

Rs 13.8 lakh crore: Banks’ lending to NBFCs surged by as much as 23% in July, according to an analysis NBFCs have been borrowing a lot more from the banks since the pandemic abated.

$12Bn NBFC: Indian government’s financing agency for universities seems to be in doldrums as the budget allocation dropped to zero and it could only achieve a third of its disbursement target.

$30bn boost: According to experts, India’s inclusion in the JPM bond index could lead to almost $30bn of passive fund inflows into Indian markets

Reading list

Why Jio Financial Services doesn’t have a clear path to world domination yet

UPI driving digital shift in India, but is not a money maker: Mastercard CFO

RBI directs credit information companies to prepare index for commercial, microfinance segments

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers, Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources