The Pattern #134

Can credit ratings help the credit starved startups?

Mayank Jain

Head - Marketing and Content

·

Sep 29, 2023

Hello everyone,

Welcome to the 79th edition of The Pattern, a weekly newsletter where we bring you the latest from the worlds of finance, economy, and technology. Let’s dive right in!

Credit rating for startups

Let’s get back to the basics.

Companies are entities in their own right – just like an individual borrower, they seek credit. For investors, therefore, it is critical to gauge their creditworthiness before being granted funding.

However, in a vibrant and dynamic entrepreneurial environment like India’s, startup funding can be tricky business. After all, the country has recognised 92,000 startups since the launch of the Startup India initiative in 2016, averaging at 80 startups per day.

While credit information companies already assign credit scores to companies, banks in India are reportedly planning a separate rating framework for startups in particular. They are in conversation with stakeholders like the RBI, rating agencies, and the government.

This is interesting because so far, banks have been assessing startups as MSMEs with little thought to the innovation and commercial viability of the product or service they offer. A common rating framework will help lenders with faster disbursals and shorter turnaround times.

Amid lean investor funding prospects, such a framework would give a boost to business borrowing and solve the cash flow woes of smaller startups – the loan amount and terms being commensurate with the merit of the product and business model, and preserving the ownership of the company with the founders themselves.

Are DBUs contributing to progress in financial inclusion?

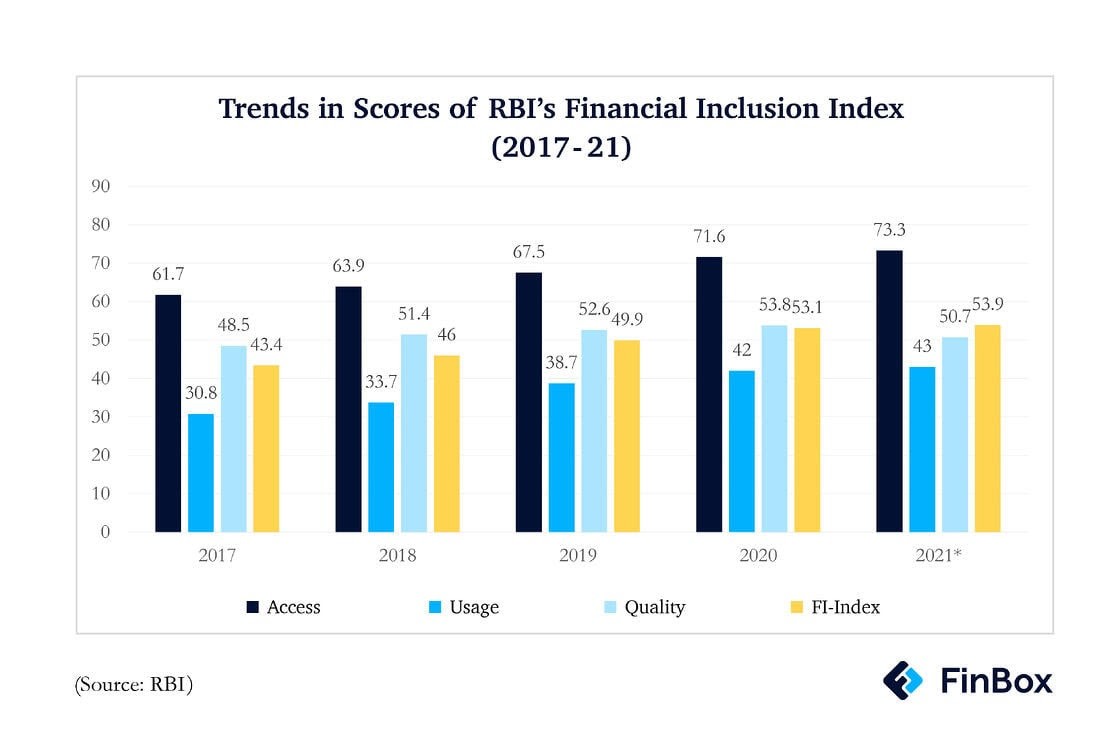

A few months ago our CEO Rajat wrote in his newsletter that the internet won’t fix financial inclusion – poking holes in the theory that digitisation alone is the messiah for those at the fringes of formal financial access. In truth, digitisation has many benefits, but the offtake of digital financial inclusion is stunted by a cold start problem. Digital inclusion is a prerequisite for financial inclusion. But despite deep smartphone penetration, the digital financial infrastructure is not being used optimally. The following graph from the RBI shows that while the supply of financial infra is high, it remains severely underused.

Why do I mention this? Because to overcome the financial gap, we need to first overcome the digital gap. And that can only be bridged through a phygital approach.

This is where digital banking units are instrumental. These bank-run outlets in small towns and villages offer banking services assisted, self-serve modes. These units offered fundamental banking services like opening of accounts, loan application, cash deposits and withdrawals and more. Now, the government has asked public sector banks to review their performance based on which it will push its schemes like the PM Vishwakarma, and leverage the growth of deposits in Jan Dhan accounts to offer additional services.

Improving DBU performance will have a deep impact on the ongoing digital reformation of legacy banks and their market share in digital financial services vis-a-vis NBFCs and their existing FinTech partnerships.

Scale-based regulation for NBFCs

Earlier this month, the RBI released a list of NBFCs that will comprise the ‘upper layer’ of players for scale-based regulation of the sector. Put simply, these NBFCs are so large that they could potentially have ripple effects on the entire financial sector.

After a long line of knee-jerk, piecemeal diktats doled out by the RBI over the past year, such a scale-based approach could signal the ushering of a more stable and long-term regulatory regime. However, what bears examination is whether imposing stricter regulations on the upper and middle layers will have a detrimental effect on overall growth in a critical sector that fills the gaps left behind by banks.

We wrote at length on the subject earlier this week. You can read it here .

Between the digits

17.5% : The decrease in the number of frontline workers in the present financial year from the previous.

€1 trillion : The amount raised by fossil fuel companies from the global bond market through European banks.

₹1300 crore : The amount paid by the RBI to procure 720 crore ₹2000 notes.

12.1% : Rise in growth of India’s eight core sectors.

$2.34 billion : Decrease in India’s foreign exchange reserves.

Reading list

State-owned banks face dilemma amidst govt and RBI directives on wilful defaults

India’s balance of payments has a current solution for a future problem

Scale-based rules, unscalable growth

Thank you for reading. If you liked this edition, forward it to your friends, peers, and colleagues. You can also connect with me on Twitter here and follow FinBox on LinkedIn to never miss any updates.

Cheers,

Mayank

All opinions expressed are my own and do not necessarily reflect the views of FinBox or its promoters.

Powering Credit Infrastructure at Scale

© 2025 Moshpit Technologies, Inc. All rights reserved.

Risk Management

Identity Verification

Solutions

Products

Resources